Becoming a first-time homebuyer in Malaysia can feel overwhelming, especially in 2026 when the market is packed with new launches, attractive mid-market projects, and shifting loan requirements. But with the right guidance, your first home doesn’t need to be confusing or stressful. This guide breaks down everything you need to know in simple, practical steps.

Whether you are preparing financially, exploring loan options, or evaluating suitable properties, understanding each step of the homebuying journey helps ensure a smoother experience.

This comprehensive guide is designed to support first-time homebuyers from start to finish, covering budgeting and financial preparation, selecting the right property, securing financing, completing the purchase, and managing responsibilities after moving in.

Ready To Start Your 2026 Homebuying Journey?

Explore affordable homes, compare locations, and find properties that fit your budget and lifestyle.

Why Buying Your First Home Matters in Malaysia

Owning a home provides long-term stability, financial security, and a sense of personal achievement. With rental rates rising in key urban areas such as Kuala Lumpur, Petaling Jaya, Johor Bahru, and Penang Island, many Malaysians are motivated to pursue homeownership earlier.

Overview of the Malaysia Property Market for 2026

The property market continues to stabilise post-pandemic, with increased supply of affordable homes, improving bank lending sentiment, and continued Government focus on homeownership support.

Market analysts highlight that buyer interest remains strong for homes priced between RM300,000 and RM700,000, especially in urban and transit-linked areas.

What’s New for First-Time Buyers under Budget 2026

Budget 2026 introduces several measures to ease the path to homeownership for first-time buyers. The Government continues to prioritise affordability and accessibility, with enhanced financing support and targeted incentives for lower- and middle-income households.

Stamp duty concessions for first-time buyers remain in place for homes up to a set threshold. At the same time, lending conditions are expected to ease through collaborative efforts between banks and policymakers.

The Budget also reinforces support for affordable housing programmes, including allocations for Malaysia Civil Servants Housing (PPAM) and People’s Housing Projects (PPR).

These measures are designed to expand supply in key urban and transit-linked locations, helping more first-time buyers enter the market as affordability remains a core national priority.

Understanding Your Budget and Financial Preparation

Before viewing any property, it is crucial to know what you can truly afford. This section helps you calculate your budget, identify hidden costs, and understand how your financial health affects your loan approval. It empowers you to plan realistically and avoid unexpected financial stress later.

- Calculating Affordability and Total Upfront Costs

Your property budget depends on income, existing commitments, credit score, and long-term financial plans. Banks typically allow a debt service ratio (DSR) of 30–70% depending on income category and lender policies. Online mortgage calculators can help estimate loan eligibility.

Upfront costs include:

Upfront costs include:

- Down payment (usually 10%)

- Legal fees

- Stamp duties

- Valuation fees

- Insurance and moving expenses

Buyers should prepare a financial buffer for unexpected expenses during the purchase process.

- Considering Hidden Costs: Legal Fees, Maintenance, and Taxes

Beyond the down payment, buyers must account for recurring obligations, including maintenance fees (for strata properties), sinking fund contributions, quit rent, and assessment tax. Strata fees vary by property type and facilities offered.

- Importance of a Good Credit Score and Financial Health

Banks assess a borrower’s repayment history, credit utilisation, and financial conduct before approving a home loan. A good credit score increases the likelihood of securing favourable loan terms. Checking your CCRIS and CTOS reports regularly is recommended.

Planning To Buy Your First Home in Malaysia 2026?

Estimate your monthly repayments and understand your affordability with our home loan calculator before you begin your property search.

Government Incentives and Support in 2026

Buying your first home can be expensive, but various national and state programmes can significantly reduce your costs. This section helps you learn which incentives you qualify for, how they work, and how to use them to lower your upfront expenses.

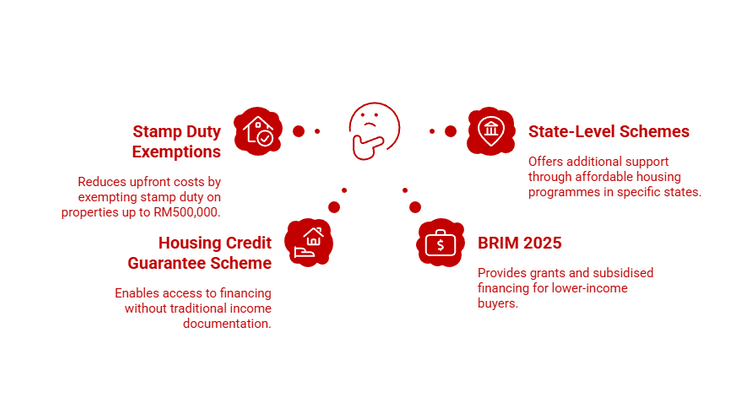

- Stamp Duty Exemptions for Properties Up to RM500,000

First-time homebuyers purchasing homes priced up to RM500,000 may qualify for stamp duty exemptions on transfer documents and loan agreements.

- Housing Credit Guarantee Scheme with Increased Allocation

The Housing Credit Guarantee Scheme (HCGS) enables buyers without fixed income documentation. Such as gig workers or small business owners, to secure home financing without traditional salary slips. The 2025 allocation has expanded to support wider access.

- Overview of BRIM 2025 (Bantuan Rumah Impian Malaysia)

BRIM 2025 is designed to support lower-income first-time homebuyers with grants, subsidised financing, and deposit assistance to encourage homeownership.

- State-Level Affordable Housing Schemes

Several states offer additional support:

- Selangor: Rumah Selangorku scheme

- Penang: Affordable Housing Programme

- Johor: RMMJ – Rumah Mampu Milik Johor

- Sarawak & Sabah: State-level affordable housing initiatives

These programmes offer eligible buyers lower pricing tiers or financial assistance.

Mortgage and Financing Options for First-Time Buyers

Buying your first home can be expensive, but various national and state programmes can significantly reduce your costs. This section helps you learn which incentives you qualify for, how they work, and how to use them to lower your upfront expenses.

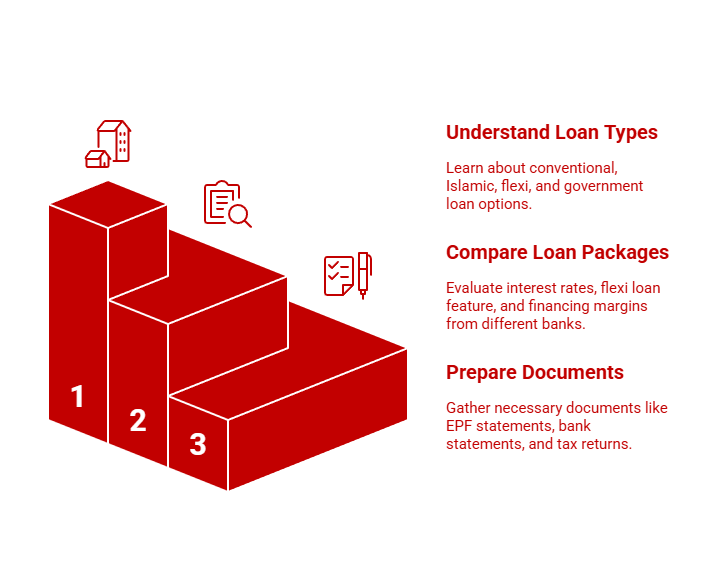

- Types of Home Loans Available and Eligibility Criteria

Common loan types include:

- Conventional housing loans

- Islamic financing (Shariah-compliant)

- Flexi and semi-flexi loans which allow prepayments.

- Government housing loans for eligible public servants

Eligibility is assessed based on income stability, employment history, CCRIS/CTOS reports, and DSR.

- Comparing Loan Packages from Different Banks

Different banks offer varying interest rates, lock-in periods, flexi-loan features, and financing margins (up to 90% for first homes). Comparing loan packages can save thousands in interest over the loan duration.

- How to Prepare Required Documents for a Loan Application

Most lenders request:

- NRIC

- The latest three to six months’ latest payslips

- EPF statements

- Bank statements

- Employment confirmation letter

- Income tax returns (Form BE)

- For self-employed: business documents, financial statements

Having these documents ready speeds up the loan process.

Choosing the Right Property

Selecting the right home goes beyond price. This section helps you evaluate property types, locations, nearby amenities, developer reliability, and overall suitability based on your lifestyle and long-term goals. It ensures you choose a property that fits your needs, not just your budget.

- Types of Properties Suitable for First-Time Buyers

First-time buyers often consider:

- Condominiums (strata living with shared facilities)

- Landed homes (terraces, semi-Ds)

- Apartments and affordable housing units

- Transit-linked homes near MRT, LRT, KTM, or BRT stations

Each property type has different maintenance costs, lifestyle appeal, and capital appreciation potential.

- Importance of Location: Proximity to Amenities and Transport

Proximity to:

- MRT/LRT stations

- Educational institutions

- Supermarkets and healthcare facilities

- Expressways such as NKVE, LDP, or MEX

Enhances convenience and increases long-term demand.

- Evaluating Developer Reputation and Property Condition

Check for:

- Developer track record

- Completion history

- Past construction quality

- Maintenance standards

For completed units, buyers should inspect plumbing, electrical fittings, structural quality, and potential leakage issues.

Step-by-Step Home Buying Process

The buying process can feel complicated, especially for first-time buyers. This section simplifies every step from searching for homes and attending viewings to signing the agreement, applying for a loan, and getting your keys. It helps you stay organised and avoid missing necessary steps.

- Searching and Shortlisting Properties Using Trusted Portals

Trusted Malaysian property portals help compare pricing trends, neighbourhood profiles, and nearby amenities.

- Viewing Properties and Assessing Their Suitability

When viewing homes, assess:

- Natural lighting and ventilation

- Noise levels

- Parking availability

- Neighbourhood condition

- Future nearby developments

Inspect both the unit and communal areas (for strata homes).

- Understanding and Negotiating the Sales & Purchase Agreement

The Sales & Purchase Agreement (SPA) outlines:

- Payment schedule

- Delivery timelines

- Defect liability period

- The rights and responsibilities of both parties

Engage a registered solicitor to ensure you understand contractual clauses and negotiate terms where applicable.

- Loan Application and Approval Process

Once the SPA is signed, buyers submit all financial documents to the lender. Loan approval typically takes between one and three weeks, depending on the bank and the completeness of the documentation.

- Finalising the Purchase and Property Handover

The final stage includes:

- Legal registration

- Transfer of ownership

- Final payment

- Handover of keys

- Starting the defect liability period

For new properties, buyers must thoroughly inspect the unit and list any defects for rectification.

Key Steps To Take After Buying A Property

Your responsibilities do not end once you get the keys. This section prepares you for ongoing costs, legal tasks, and future planning. Knowing what to expect helps you manage your home efficiently and maintain its long-term value.

- Managing Maintenance and Ongoing Costs

Homeowners must budget for:

- Utilities

- Strata maintenance and sinking fund fees

- Repairs and upgrades

- Property taxes (assessment and quit rent)

- Registering Your Property and Ensuring Legal Compliance

Ensure proper registration with the Land Office and settle all legal requirements. Keep copies of the SPA, loan documents, and receipts for reference.

- Planning for Future Upgrades or Resale

Understanding market cycles, neighbourhood growth, and upcoming infrastructure projects helps homeowners plan future renovations or potential resale strategies.

- Understanding Your Home Loan Obligations

Homeowners should familiarise themselves with their loan repayment schedule, interest structure, and any penalties for late payment or early settlement. Keeping track of instalments and reviewing refinancing options periodically can help improve long-term affordability.

- Protecting Your Home With Insurance

A suitable home insurance policy protects your property against unforeseen events such as fire, floods, and theft. First-time homeowners should review available coverage options and ensure their policy aligns with the property type, location and long-term needs.

By understanding these responsibilities early, first-time buyers can manage their homes confidently and protect the long-term value of their investment.

Best Areas First-Time Buyers Can Consider in 2026 and Beyond

For new homeowners entering the Malaysian property market, these locations strike the sweet spot between affordability, growth potential, and strong connectivity.

1. Shah Alam (Selangor) – LRT3 Growth Corridor

- Ideal for family-friendly landed and strata homes

- New LRT3 stations are increasing accessibility

- Strong rental and resale demand

2. Seri Kembangan (Selangor) – MRT2 Connectivity

- Great for younger buyers seeking condos under mid-range budgets

- Direct MRT2 access to KL City & Putrajaya

- New mixed-use developments boosting long-term value

3. Puncak Alam (Selangor) – Rapid Township Development

- One of Klang Valley’s fastest-growing affordable townships

- New highways + future rail links improving demand

- Plenty of new projects are ideal for first-timers.

4. Tebrau (Johor Bahru) – RTS Link Spillover Zone

- Huge uplift expected from the JB–Singapore RTS Link opening

- Attractive condo prices compared to the Klang Valley

- Popular among first-time buyers working in Johor or Singapore

5. Batu Kawan (Penang Mainland) – Penang’s New Growth Hub

- Tech-driven employment growth is attracting young buyers

- More affordable than Penang Island

- New townships, malls, and industrial parks are strengthening demand

6. Kuching Outskirts (Sarawak) – Expanding Suburban Market

- Good for landed-home seekers

- Infrastructure upgrades are improving connectivity.

- Strong community living and lower cost of entry

7. Kota Kinabalu Fringe Areas (Sabah) – Affordable Urban Alternatives

- Growing supply of modern apartments

- Tourism-led economy supporting future rental income

- Better price appreciation than the city core over time

These areas offer good prices, strong growth, and better connectivity, making them great choices for first-time buyers.

Tips for First-Time Homebuyers in 2026

This section shares practical, experience-based advice to help you avoid common mistakes. It encourages patience, wise decision-making, and proper guidance, giving you the confidence to move forward with clarity.

- Avoid Common Mistakes and Pitfalls

Many first-time buyers face challenges such as:

- Underestimating hidden costs

- Choosing a property without researching the area

- Overstretching budgets

- Rushing purchases without comparisons

Avoid these by conducting thorough due diligence.

- Importance of Patience and Due Diligence

Taking a careful, step-by-step approach ensures that buyers make informed choices and avoid costly mistakes.

- Take time to compare properties, review documents and understand financial commitments.

- A well-researched decision helps buyers avoid long-term financial strain.

- Reaching Out to Professionals for Guidance

Getting expert help makes the buying process easier and more transparent.

- Real estate agents

- Solicitors

- Bank officers

- Financial planners

Professionals can offer insights that help streamline the entire buying process. With the right preparation and guidance, first-time buyers can move forward confidently and make decisions that support long-term homeownership success.

What This Means for Your 2026 Homebuying Journey

Becoming a homeowner in Malaysia is a significant milestone, and with the proper preparation, the journey can be smooth and rewarding. Understanding your budget, identifying suitable properties, securing the right financing, and navigating legal processes are all essential steps for first-time buyers.

With ongoing Government support, improved housing schemes, and a diverse property market, 2026 offers promising opportunities for Malaysians planning to purchase their first home.

Careful planning, thorough research, and awareness of market trends help first-time homebuyers make confident, informed decisions and ultimately secure a home that aligns with their financial goals and lifestyle needs.

For more insights on home loans, budgeting, and first-time buyer strategies, visit the PropertyGuru Guides section.

Ready to start your search? Explore Malaysia’s exclusive homes for sale and find a property that fits your needs.

Keep Track of New Launches

Visit our new launches page to find the new launch project of your dreams and submit an enquiry today.

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.