By Dr. Daniele Gambero

Housing the nation has become a strong tagline for politicians and developers in the last 12 months. Being honest we all should praise most of the Malaysian developers for the fast action showed in shifting their offers from medium –high end residential properties towards more affordable values and sizes. Recently I’ve underlined that still too many developers are actually offering affordable values in terms of RM/psf but at the end, due to “oversized lay-out” in terms of built-up, the value of the house raise again far above the affordable ones.

Recently another threat to the “housing the Nation mission” has been once again averting the possibilities for middle class families to realize their dream to own a home: financing has become more and more difficult and getting your loan approved is tougher and tougher by the day. BNM (Bank Negara Malaysia) has introduced during the last few years a number of restrictions and curbing measures deemed to cool the speculative actions of irresponsible investors, the infamous “Flippers” (buy today sell in few months and make fast cash out of it). The enforced measures have been surely achieving the target of reducing unscrupulous actions but at the same time have been making more and more difficult for genuine buyers to get their hands over a long desired home.

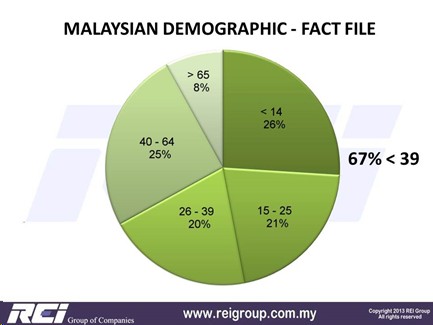

Authorities, banks and BNM should really start looking into the profile of genuine buyers to understand their weaknesses and strength, demographic information are nowadays crucial and strategic to determine the “loan or home-purchasing packages” to be offered. 67% of the Malaysian population is currently aged 39 years and below, the most spoken about GenY and upcoming GenZ or Millennials. This group, representing the future of Malaysia, is for the greatest part having a net monthly income between RM2,000.00 and RM8,500.00 which should allow them to buy homes priced below RM600,000.00. Authorities and developers should do a more in depth analysis of the actual wealth-sharing to better understand the meaning of affordable values and, at the same time, banks should be start looking into possible measures to tailor the mortgage offer to the actual “pockets or valet size” of these home buyers.

The two tables below show an in-depth study done for one of our client in the southern region and is quite precise in terms of quantities and values to be offered to reply in a pro-active way to the demand of affordable homes in Iskandar Malaysia.

Wealth distribution in terms percentage of house-holds sharing the available wealth above and, based on the outcome define the quantities and values of homes to offer.

Beside this first analysis, we all should consider the fact that saving is not one of the strengths of the young Malaysians and consequently we need to find ways to help them during the purchasing process. As per the table below is easy to understand how affordable homes are actually un-purchasable due to the high amount of cash required upon signing the Sale and Purchase Agreement. On top banks are very conservative in their risk calculation and very often the applicant gets a margin of financing slashed down to 85% for the lucky ones and 75-80% for the less fortunate.

Are there any solutions to all these issues? Many are the possible replies to this challenging situation but we all need to be more flexible and a bit creative.

Several might be the actions which, if implemented, will surely help to spur the purchase of affordable homes by genuine first time buyers. Of course there must be a kind of unconditional support from all the parties involved and a fair behavior by the purchasers.

Bank Negara first; our central bank authority should release some of the introduced curbing measures by allowing, only for first time home buyers, easing the high “cash-out” that purchasers have to get ready for when deciding to purchase an affordable home. See the table above again for better understanding.

In case our purchaser is buying a strata property the cash-out amount might be limited to RM38,596.00 as Stamp & Duty on MOT will only be charged later on. But still the amount is impressive if we consider that a RM320,000.00 home will possibly be purchased by a household with a monthly income of RM5,000 to RM7,000.00. How long might take to a family to save enough to proceed with the long sigh for dwelling purchase? A research conducted in 2013 by Sime Darby and the University of Malaya has been determining that the average Household in Klang Valley has a mix of out-goings as per the iconographic above.

By looking at an average house-hold income as per what mentioned above, RM5,000.00 to RM7,000.00, and using the percentages showed in the iconographic above we can estimate the following minimum time-frame, as per currently imposed “terms & conditions” (BNM), to enable a young family to buy their first home with values as per our previous table’s value.

Nowadays people are getting married not at very young age, say somewhere between 28 and 34 years; which means that young families, as per current situation, will be able to look into their first home from the age of 40 and above. What if any unforeseen extra expenses will suddenly come in? What, even more important, will happen to house values within the next 5 to 6 years? Isn’t it there is a very high chance that property values will move upward averting to a farer date the sigh for home purchase?

It is an extremely unfair situation and not a viable option to finally housing the nation.

Further difficulties are coming in if the future owner/s have accessed a PTPTN loan for further studies and possibly forgotten that what is borrowed first must be repaid later. I’ve already written about this hidden gigantic issue which might be placing totally out of reach whichever property for the unlucky ones.

Not to mention the unreasonable standing of some banks which are slashing to a mere 80% or 85% the margin of financing for those affordable properties (priced below RM500,000.00) but located so to say “out of hand” such as South of Bangi or Semenyih.

Last but not least most developers are keeping on building unaffordable homes not because of the RM psf but due to the huge size (abundantly above 2,000 sq.ft.) of the dwelling’s design.

Where is the logic of all the above? It is a total nonsense and by keep on talking and not acting this problem will keep on growing instead of being finally solved.

A bit of common sense for everybody

Developers: please built normal homes sized between 1,000 and max 2,000 square feet. Above all, please, do not fit the homes with M&E and cabinets but leave the purchaser the right to choose what they like. In this way there will be much higher chances to obtain more affordable values.

Purchasers: the ones of you with outstanding PTPTN balance please go and discuss a repayment plan which will avoid your blacklisting as since April 1st 2015 Bank Negara has started uploading the delay in repayment and many “bad PTPTN paymasters” have already been blacklisted! For them, unfortunately, purchasing their first home will remain a dream for a very long time.

Bank Negara: the wish list for BNM is quite long; hopefully it will be read and at least partially taken into possible consideration.

- Allow developers to reinstate the 10% deposit rebate for first time home buyers only as it is still the fastest and most practical way to obtain 100% financing. If not full rebate at least allow a 3% deposit only.

- Another good help for first time home buyers will be the possibility to avoid the payment of any interest during construction. Only for first time home buyers please re-introduce the DIBS.

- For those PTPTN bad paymasters why it is not possible to find a solution contextual to the home purchase? A minimum agreed upon and affordable amount per month will be transferred from the financing bank directly to PTPTN till balancing the outstanding study loan. There might be a committing document to be signed upon completing the Loan Agreement for the sigh for home.

Government: developing affordable homes is becoming more and more difficult for the private industry players as the reduced profitability leaves a zero margin to mistakes and unforeseen events. Is there any chance to introduce some sort of subsidies to reduce the burden on the first time home buyers? Defining an affordable-home values table which will grant, providing the maximum values in the table will be respected, reduced premium/authority contributions/utilities contributions and so on will surely spur the supply of more affordable homes in the near future and possibly see the nation being final housed.

It is always easy to talk, I’m fully aware of this, but we really need to start from somewhere and the above are few opening discussion points that, if properly carried on might be having good outcome in a relatively short time. *My 5 cents with no intention of hurting or offending anybody*

******************************************************************************************************************

Dr. Daniele Gambero is the CEO and co-founder of a strategic marketing consultancy firm, REI Group of Companies. He provides strategic marketing consultancies, investment studies, researches, property market reports and business valuation all around the world.

Dr. Daniele Gambero has been engaged as a speaker in REHDA KL, REHDA Johor, The Star Property Fair, iProperty, Wealth Mastery Academy, Comfori, ASLI, PIHex and Mastery Asia. Through his ability in structuring local and global macro / micro economic indicators to look into the Malaysian Property Market, he centers his speeches on the rightness of property investment based on current and future market values, location, future infrastructures and their impact on the market trend.

Keep Track of New Launches

Visit our new launches page to find the new launch project of your dreams and submit an enquiry today.

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.