In 2026, Malaysia’s property market is entering a new phase. Budget 2026 proposals, a stronger focus on affordable housing, and changes to how foreign buyers are taxed are reshaping both demand and access to financing. At the same time, the supply of new homes is tightening, which may put gentle upward pressure on prices in the coming years.

For homebuyers and investors, understanding the Malaysia Property Financing Policy 2026 is no longer optional. It sits at the intersection of three significant forces: government housing reform, bank lending behaviour, and an evolving market where supply, prices, and transaction volumes are shifting simultaneously.

This guide walks through the key policy and financing changes for 2026, how they affect different types of buyers, and what you can do now to prepare.

Find Your Next Home Now

Check out available properties on the market today.

What the Malaysia Property Financing Policy 2026 Really Covers

When we talk about Malaysia’s property financing policy 2026, we are essentially referring to a cluster of changes that interact with one another:

- Budget 2026 housing measures, including support for affordable housing, rent-to-own (RTO) models, and a gradual emphasis on build-then-sell to reduce abandoned projects.

- Stamp duty and tax adjustments, especially for foreign buyers, and extended exemptions or reliefs for first-time Malaysian homebuyers.

- Bank and lender practices, such as how Debt Service Ratio (DSR) is interpreted, who qualifies for special guarantee schemes, and how the Overnight Policy Rate (OPR) environment shapes borrowing costs.

- Market performance data, including transaction volumes, house price movements, and overhang trends from the National Property Information Centre (NAPIC) and other market research.

Malaysia Property Financing Policy 2026 is not about one single law or scheme. It is about how Government policy, lending rules, and market realities combine to influence your ability to buy, upgrade, or invest.

Key Housing And Property Policy Changes In 2026

Malaysia’s property landscape in 2026 will be shaped by several important policy updates aimed at improving affordability, regulating demand, and strengthening buyer protection.

These changes affect both local and foreign purchasers, influencing transaction costs, eligibility, and overall market behaviour. Understanding these shifts is essential for buyers planning their next move in 2026.

- Stamp Duty And Taxation Changes

Budget 2026 introduces notable changes to stamp duty, especially for foreign purchasers. Several analyses summarising the proposals indicate that:

- Foreign individuals and foreign-owned companies buying Malaysian residential property will face a higher stamp duty band of roughly 4-8% on the instrument of transfer from 1 January 2026, replacing the previous flat 4% rate.

- Permanent residents are generally exempted from this higher foreign-buyer band and will follow the standard residential stamp duty scale instead.

The stated aim is to ensure the market remains accessible for Malaysians, while moderating speculative or high-end foreign demand that could drive prices up in key urban centres.

For Malaysian citizens, Budget commentaries suggest that stamp duty exemptions or discounts for first-time homebuyers on properties within a certain price threshold are being extended into 2026, in line with the Government’s housing reform agenda.

On Real Property Gains Tax (RPGT), no radical overhaul has been announced at the time of writing. Still, any changes would likely be calibrated to balance revenue needs with encouraging long-term ownership rather than short-term speculation.

- Housing Reform And Affordable Access

The Ministry of Finance has made it clear that Budget 2026 is intended to strengthen housing reform and expand access to affordable housing, especially for lower and middle-income households.

Key directions flagged include:

- Further support for affordable housing projects, particularly in high-demand urban and suburban areas.

- Development of new models, such as rent-to-own schemes and a gradual shift towards build-then-sell to reduce abandoned projects and better protect buyers.

- Closer examination of support mechanisms for households with less stable income, such as gig workers or self-employed individuals, through guarantee or assistance schemes.

While the exact structures of every scheme will be detailed only when the implementing guidelines are published, the policy direction is clear: more emphasis on affordability, protection, and inclusivity in 2026.

- State-Level Differences To Watch

State Governments retain some control over:

- Minimum price thresholds for foreign buyers.

- Approval processes for certain types of projects.

- Additional levies or incentives on selected segments.

Analyses of market conditions in Johor, Selangor, Kuala Lumpur, and Penang show that transaction trends and unsold stock levels differ across states, suggesting that each state may calibrate its policies slightly to match local realities better.

For buyers, this means you should always check:

- The latest minimum foreign-purchaser price in your target state, if you are a non-citizen.

- Any state-level incentives for first-time homebuyers or specific categories (for example, affordable schemes).

The 2026 Home Financing Landscape: What Buyers Need To Know

Malaysia’s home financing environment is set to shift in 2026 as banks adapt to stabilising interest rates and new Government measures aimed at improving affordability. Lending assessments may evolve, especially for first-time buyers and those with non-traditional income.

Because financing determines real purchasing power, understanding Debt Service Ratio requirements, loan guarantees, and bank expectations will be crucial. For anyone planning to buy in 2026, knowing how these changes affect eligibility can help you prepare and strengthen your chances of approval.

- Lending Conditions And Bank Behaviour

Bank Negara Malaysia’s Overnight Policy Rate (OPR) remains the key reference for mortgage rates. Although future OPR moves cannot be predicted with certainty, recent data points to a stabilising property market, with moderate house price growth and declining overhang, rather than a speculative bubble.

Banks are expected to continue focusing on:

- Debt Service Ratio (DSR): your total monthly commitments relative to income.

- Type and stability of income: salaried, self-employed, gig, or commission-based.

- Existing leverage: whether you already own one, two, or more properties.

With Budget 2026 spotlighting lower and middle-income households, lenders may be more willing to participate in Government-supported guarantee schemes that reduce their risk for specific categories of borrowers, such as first-time buyers or those without conventional proof of income.

- Loan Schemes, Guarantees, And Support

Several commentaries on Budget 2026 and related housing measures highlight the following themes:

- Use of cash assistance programmes and social support schemes to indirectly support housing affordability, allowing families to allocate more of their income to home purchases.

- Exploration of rent-to-own structures that allow households to gradually transition from tenants to owners, which can be helpful for those who struggle to meet initial down payment requirements.

- Potential expansion or refinement of guarantee schemes that back loans for buyers with otherwise sound repayment ability but non-traditional income profiles.

In practice, this means that in 2026, you may see:

- Slightly more pathways into ownership for first-time buyers and those in the lower mid-market segment.

- Tighter scrutiny on multiple-property borrowers, investors, and higher-risk segments, particularly if banks perceive greater exposure in those categories.

- Who May Find Financing Easier Or Harder In 2026

Based on the policy direction and market analysis so far:

- First-time Malaysian homebuyers

- Likely beneficiaries of extended stamp duty reliefs, targeted Budget 2026 measures, and any guarantee or RTO schemes.

- Still need to meet DSR and credit score requirements, but may experience slightly better approval odds if they fall within the targeted income bands.

- Upgraders and multi-property owners

- More sensitive to OPR and interest rate movements, since they often carry larger combined mortgage commitments.

- May face stricter DSR assessments if they already have one or two existing loans.

- More sensitive to OPR and interest rate movements, since they often carry larger combined mortgage commitments.

- Local investors

- Benefit from stabilising prices and potentially rising rents in selected areas, but must navigate stricter credit assessments and higher upfront costs if purchasing higher-value assets.

- Benefit from stabilising prices and potentially rising rents in selected areas, but must navigate stricter credit assessments and higher upfront costs if purchasing higher-value assets.

- Foreign buyers

- Will likely face a significantly higher stamp duty on property transfers from 1 January 2026, which will directly increase acquisition costs and may reduce leverage for some investors.

- Some may shift to higher-yielding or more premium segments to justify the higher entry cost, while others may reduce exposure or pursue sub-sale opportunities.

- Will likely face a significantly higher stamp duty on property transfers from 1 January 2026, which will directly increase acquisition costs and may reduce leverage for some investors.

Understanding these financing changes helps buyers prepare more confidently and choose the right approach when entering the market in 2026.

Supply Demand And Price Trends Shaping 2026

Malaysia’s property market is entering 2026 with shifting fundamentals. New launches are slowing, unsold stock is gradually easing, and demand in key urban areas is recovering.

These factors, combined with improving buyer sentiment, are expected to influence pricing and market activity throughout the year. Understanding how supply and demand interact will help buyers anticipate where opportunities or pressure points may emerge in 2026.

- Slower New Launches, Cautious Developers

Recent reports indicate that new residential launches have already been moderating, with new project numbers falling compared to previous years. For example, reports based on NAPIC and market data show:

- New residential launches in some quarters of 2025 fell sharply year on year, reflecting more cautious developer behaviour.

- Earlier overhang levels have started to decline, suggesting the market is gradually absorbing existing unsold stock.

Press releases and research from Juwai IQI and other market observers point to fewer new homes and more cautious planning into 2026, which may reduce future supply, especially in popular urban locations.

- House Price Movement

NAPIC data shows that Malaysian house prices have been growing moderately, with average prices rising but at a slower pace than in earlier cycles. One recent update notes:

- Malaysian House Price Index growth of about 3.3% in 2024, with an average price per unit of around RM486,678.

- Q3 2025 data shows annual price growth of around 0.1%, with an average price of roughly RM494,384, suggesting a phase of stabilisation after several years of gains.

At the same time, some forecasts suggest that 2026 could see moderately higher prices, supported by improved sentiment, fewer new launches, and Budget 2026 measures that may lift transaction volumes by about 3-5% compared to 2025.

For buyers, this combination points to a market that is neither in a steep downturn nor overheating, but gradually firming up.

- Transaction Volume And Market Confidence

Bernama, Free Malaysia Today, and industry press releases quoting Juwai IQI analysts suggest that Budget 2026 could:

- Boost residential transaction volumes by roughly 3-5% in 2026.

- See first-time buyers and the lower mid-market price bands leading this growth, supported by cash assistance, targeted incentives, and more careful supply management.

This implies that demand in the affordable and mid-market segments, especially in established urban and suburban locations, may remain relatively strong in 2026.

How Different Buyer Segments Will Feel The Changes

The impact of Malaysia’s 2026 property policies and financing shifts will not be the same for every buyer. First-time purchasers, upgraders, investors, and foreign buyers will each face distinct opportunities and challenges. Understanding how these groups are affected can help you identify where you fit and what adjustments you may need to make before entering the market.

- First-Time Homebuyers

For first-time Malaysians buying in 2026, the environment is mixed, but broadly positive:

- Extended or renewed stamp duty exemptions or discounts on eligible price ranges improve upfront affordability.

- Budget 2026’s focus on affordable housing, rent-to-own, and housing reform is clearly aligned with helping this group get onto the property ladder.

- However, you still need to meet bank DSR thresholds, maintain clean credit behaviour, and handle living costs, which remain a key part of the affordability equation.

If you are a first-time buyer, 2026 may be a sensible year to act, especially if you find a reasonably priced unit in an area with strong fundamentals such as established infrastructure, access to employment centres, and long-term demand.

- Upgraders And Growing Families

Upgraders, such as households moving from a smaller apartment to a larger landed home or a bigger stratified unit, need to consider:

- Total exposure across multiple loans, since DSR will be calculated on all commitments.

- The possibility that prices in certain popular landed and family-oriented areas may edge up due to limited new supply and stable demand.

- Transaction costs, especially high if the property value crosses higher stamp duty tiers.

The decision to upgrade in 2026 should be driven by genuine need, clear affordability, and a realistic view of long-term repayment capability rather than speculation.

- Local Property Investors

For local investors, 2026 is likely to be a year of careful selection rather than aggressive expansion:

- Moderately rising prices and gradually improving rental markets in selected corridors may support yields, especially in areas linked to employment, infrastructure, or lifestyle clusters.

- However, bank scrutiny of investor profiles and leverage is unlikely to loosen dramatically, particularly for buyers already holding several properties.

Investors may focus more on:

- Properties with realistic, sustainable rental demand.

- Units in segments where supply is tightening, but end-user demand is stable.

- Foreign Buyers

Foreign buyers will feel 2026 more sharply on the cost side:

- The proposed increase in stamp duty to a higher 4%-8% band on transfers from 1st January 2026 significantly raises purchase costs at the entry level.

- Combined with existing minimum price thresholds in many states, this will likely push foreign investors towards higher-value or specialised products, rather than competing directly in the mass-market or affordable segments.

Some foreign investors may respond by:

- Prioritising units with stronger capital appreciation prospects or unique attributes.

- Considering partial diversification into commercial, industrial, or alternative asset classes, where the rules and yields differ.

Practical Steps Buyers Can Take For 2026

Regardless of which segment you fall into, there are several practical actions you can start taking now:

- Check Your Affordability Using A Home Loan Calculator

- Use a mortgage calculator to estimate monthly instalments at different interest rates and tenures, and to see how far your current income goes under typical DSR assumptions.

Check Your 2026 Affordability Instantly

Quickly estimate your monthly instalments under the latest financing policy.

- Tidy Up Your Financial Profile

- Pay down high-interest debts where possible.

- Avoid taking on new short-term commitments right before a mortgage application.

- Check your credit score and correct any errors if needed.

- Pay down high-interest debts where possible.

- Prepare Documentation Early

- For salaried workers: ensure your payslips, EPF statements, and tax filings are up to date.

- For gig workers or self-employed buyers: gather bank statements, invoices, contracts, and any supporting documents that demonstrate consistent income. This becomes even more important if you intend to benefit from any guarantee schemes.

- For salaried workers: ensure your payslips, EPF statements, and tax filings are up to date.

- Monitor Policy Announcements Closely

- Look out for detailed Budget 2026 implementation guidelines and any revisions to stamp duty, exemption thresholds, or specific schemes.

- Check both national and state-level sources, as states may fine-tune minimum price thresholds or local incentives.

- Look out for detailed Budget 2026 implementation guidelines and any revisions to stamp duty, exemption thresholds, or specific schemes.

- Compare Loans, Not Just Properties

- Different banks may interpret DSR and risk differently, especially for buyers with non-traditional income.

- Compare interest rates, lock-in periods, and flexibility for extra repayments across several lenders before committing.

- Different banks may interpret DSR and risk differently, especially for buyers with non-traditional income.

By taking these steps early, buyers can stay financially prepared, meet lending expectations, and make confident decisions in 2026. A well-planned approach will make it easier to secure the right home and navigate Malaysia’s evolving financing landscape.

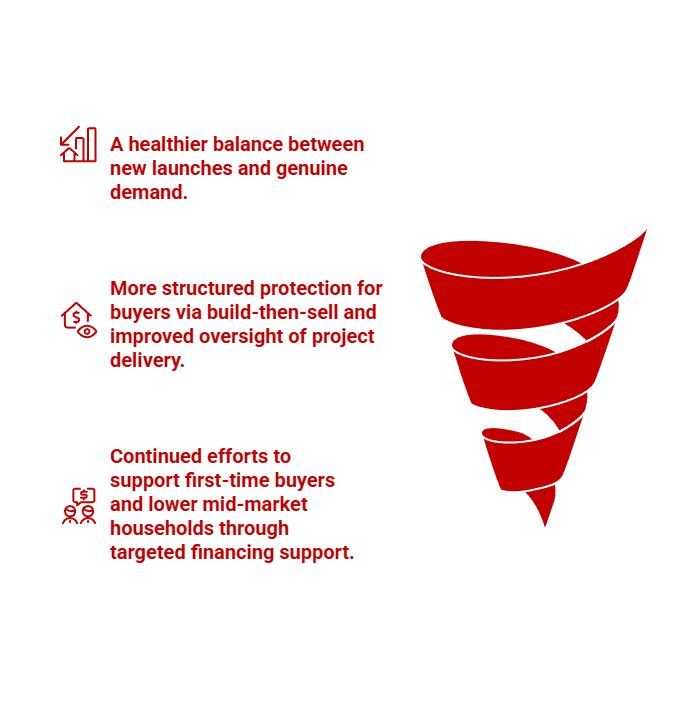

What Buyers Can Expect Beyond 2026

Budget 2026 sits within a broader reform framework under the 13th Malaysia Plan, which aims to improve housing affordability, reduce overhang, and encourage more sustainable development and financing practices.

If reforms are implemented consistently, the medium-term outlook could include:

- A healthier balance between new launches and genuine demand.

- More structured protection for buyers via build-then-sell and improved oversight of project delivery.

- Continued efforts to support first-time buyers and lower mid-market households through targeted financing support.

However, buyers should remember that interest rates, economic conditions, and personal circumstances can change. A property decision in 2026 should still be evaluated on a long-term basis, not solely on short-term incentives.

What 2026 Really Means For Property Buyers

Overall, 2026 marks a year of adjustment rather than disruption for Malaysia’s property market. Policy changes, tighter financing expectations, and a more measured supply pipeline will shape buying conditions, but the underlying environment remains stable.

First-time buyers may benefit from targeted support and clearer pathways to ownership, while investors and foreign purchasers will need to navigate higher costs and stricter credit assessments.

With thoughtful planning, realistic budgeting, and a good understanding of how these policies influence affordability, buyers can approach 2026 with confidence and make decisions that align with their long-term goals.

For more guidance on how the Malaysia property financing policy 2026 influences affordability, loan eligibility, and buyer strategies, browse the PropertyGuru Guides section.

Ready to plan your next step? Explore Malaysia’s latest homes for sale and find a property that aligns with your financing goals for 2026.

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.