When planning to sell property in Malaysia, understanding the Real Property Gains Tax Act 1976 (RPGT) and, in particular, the available exemptions can make a significant difference to your final profit. Whether you’re preparing to dispose of an investment or exploring how new RPGT rules might affect your next sale, let’s begin by understanding the fundamentals, what RPGT really is, and why it continues to shape Malaysia’s property market in 2025 and beyond.

RPGT remains one of the most closely watched areas of Malaysian property taxation, not just for investors but also for everyday homeowners aiming to maximise returns.

In this guide, we break down the latest RPGT exemptions, unpack recent regulatory shifts, and guide you through calculating, filing, and optimising your property sale with clarity.

What is RPGT and Why Does It matter?

In Malaysia, the Real Property Gains Tax (RPGT) is levied on the profit, known as the "chargeable gain", arising from the disposal of real property or shares in an honest property company. It applies to both individuals and corporate entities, meaning that any gain made from a sale can directly reduce the net proceeds you ultimately receive.

The tax is therefore a crucial consideration for anyone planning to sell, transfer, or restructure property holdings, as it influences not only profit margins but also timing and financial planning.

Understanding how RPGT operates enables you to make more strategic and informed decisions, from selecting the most advantageous time to sell to effectively managing acquisition and improvement costs and ensuring that all available reliefs are properly claimed.

By anticipating how RPGT will apply to your particular circumstances, you can avoid unnecessary liabilities and align your sale with broader financial goals.

According to the official rate tables issued by Lembaga Hasil Dalam Negeri Malaysia (LHDN), the applicable RPGT rate depends on your taxpayer category, whether you are a Malaysian citizen, a company, or a foreign owner, and on the duration of your asset ownership before disposal. This tiered approach means that ownership duration plays a crucial role in determining the amount of tax you ultimately pay.

Key Real Property Gains Tax (RPGT) Updates for 2025

Malaysia’s Real Property Gains Tax (RPGT) framework has undergone several vital refinements for the 2025 assessment period, aimed at improving transparency, compliance, and efficiency in property transactions. Whether you are selling an investment property or disposing of a long-held asset, these updates are crucial to understand.

Here’s what has changed:

As part of Malaysia’s updated tax framework, several significant changes to RPGT have now been implemented. Here’s what has changed:

- Transition to Self-Assessment (Effective 1 January 2025):

RPGT has officially shifted to a self-assessment system, placing full responsibility on the disposer to calculate their own tax liability and submit the relevant returns. The CKHT-1A and CKHT-2A forms remain mandatory, but computations are now self-declared rather than determined by LHDN. - Revised Filing and Payment Requirements:

While the exemption provisions remain in effect, filing deadlines and administrative procedures have been tightened. RPGT payments must now be made within 90 days from the date of disposal, reinforcing timely compliance and accurate reporting. - Updated Tax Treatment by Ownership Category:

For individual Malaysian citizens and permanent residents, disposals of properties held for six years or more remain exempt from RPGT. However, foreign owners and companies remain subject to tax at existing rates, depending on their holding period and transaction details. - Clearer Exemption Guidelines:

The exemption criteria have been clarified for several scenarios, including disposals of private residences, family transfers, and low-cost homes. Taxpayers should carefully review these definitions to ensure continued eligibility.

As Malaysia transitions into the 2025 assessment landscape, it’s essential to verify that your tax references, guides, or financial records reflect these most recent changes. (Any information citing only Budget 2019 or Budget 2022 without acknowledging the self-assessment system and updated compliance deadlines should be revised or removed to avoid confusion.)

RPGT Exemptions: Eligibility and How They Work

When it comes to managing your Real Property Gains Tax (RPGT) obligations, exemptions can make a substantial difference to how much tax you ultimately pay.

Below are the key reliefs available for 2025, along with the essential conditions attached to each:

A. Basic Individual Exemption (RM 10,000 or 10 %)

Every property seller should first understand the standard exemption available to individuals. It acts as a baseline reduction that can lessen your overall tax exposure.

- An individual may claim an exemption equal to RM 10,000 or 10% of the chargeable gain, whichever is greater.

- Applies to real property disposal by an individual (citizen or permanent resident).

- Important: This must be claimed, and your documentation (including purchase price, legal fees, and improvement costs) must be accurately recorded.

This exemption may appear modest at first glance, but for many individual sellers, it serves as a crucial buffer against smaller capital gains.

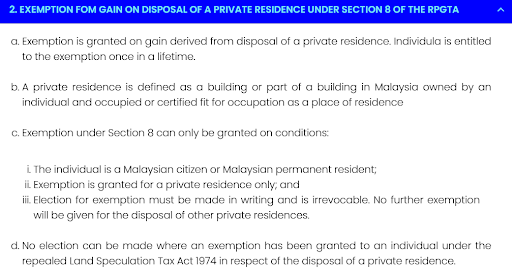

B. Once-in-a-Lifetime Exemption on Private Residence

This relief is one of the most valuable for homeowners, as it allows individuals to be entirely exempt from the gain on their primary home once in their lifetime.

- A Malaysian citizen or permanent resident may claim relief for the disposal of one private residence in their lifetime.

- Conditions: The property must be a building or part of a building owned and used as the taxpayer’s residence; the election for relief is irrevocable.

- If you qualify, this relief can significantly reduce your tax burden.

If you qualify, this relief can substantially reduce your tax burden, particularly for high-value residential properties.

C. Family Transfers Exemption

Family-based exemptions reflect the government’s intent to encourage intergenerational property transfers without undue tax pressure.

- Transfers between spouses, parents and children, or grandparents and grandchildren may qualify for a full exemption (i.e., the gain is treated as zero) provided the donor is a Malaysian citizen.

- Note: Transfers between siblings or other relatives do not generally qualify for this relief.

This exemption is beneficial for estate planning and family restructuring, as it helps ensure that assets can be passed on without triggering additional tax liabilities.

D. Low-Cost Residential Homes Disposal Exemption

This exemption was initially introduced to support affordability and mobility within the lower-income housing segment. While no longer active, it remains a valuable point of reference for potential future policy adjustments.

- The exemption introduced under Budget 2019 allowed Malaysian citizens to disregard gains from disposing of low-cost residential homes valued at RM200,000 or less, provided the property was held for at least five years and sold between January 1 and December 31, 2019. This was a one-off measure that expired after that period.

- As of 2025, there is no active exemption of this kind. Any future reinstatement or new version would require formal inclusion in subsequent budget announcements or amendments to the RPGT Act.

Any future reinstatement or variation of the rule would need to be formally announced through upcoming Budgets or RPGT amendments, so property owners should stay alert to fiscal updates.

E. Other Exempt Transactions

Finally, certain types of property disposals are specifically exempt from RPGT altogether, typically those considered involuntary or for public benefit.

- Certain specific transactions are deemed not to generate gains or are exempt, for example, disposals arising from compulsory acquisition, gifts of property to the government, local authorities, or approved charities, and intra-group transfers where the transferor and transferee meet the 75% ownership test.

These exemptions play a vital role in preventing unnecessary tax charges where no true profit motive exists, ensuring the system remains fair and proportionate.

Get expert insights, practical tools, and up-to-date market guidance.

Looking for clarity on property disposal and tax planning?

Key Rates and Ownership Periods

Understanding the tax rate structure remains vital because it interacts with the reliefs.

Here is a simplified table for the rate regime from 1 January 2022 onwards for individuals who are Malaysian citizens and permanent residents:

| Holding Period | RPGT Rate (Citizen/PR) |

|---|---|

| Up to 3 years | 30% |

| 4th year | 20% |

| 5th year | 15% |

| 6th year and onwards | 0% |

For foreigners/non-permanent residents, or companies, the rate may be 10% or higher for those with a tenure of 6 years or longer.

Understanding this helps you decide whether to use an exemption now or wait for a later year when the rate drops.

How to Calculate Your Chargeable Gain and Apply Exemptions?

Here’s how the maths works and how you factor in exemptions:

Step 1: Determine your gain = Disposal Price – (Acquisition Price + Allowable Expenses)

Allowable expenses may include legal fees, agent commission, renovation/improvement costs, and stamp duty (if eligible).

Step 2: Subtract the exemption you qualify for.

Example: You qualify for RM 10,000/10% relief, which amounts to approximately RM 15,000 (if your gain is RM 150,000, 10% = RM 15,000). Your net gain = RM 150,000 – RM 15,000 = RM 135,000.

Step 3: Multiply your net gain by the applicable rate (depending on your status and holding period).

If your rate is 0% (for example, disposal after 6 years for citizens/PR), you pay nothing. If your rate is 15%, you pay 15% of RM135,000, which is RM20,250.

Worked Example

Suppose you’re a Malaysian citizen who bought a property for RM 500,000 five years ago and now sells it for RM 800,000.

- Chargeable gain = RM 300,000

- Exemption (RM 10,000 or 10% of 300k = RM 30,000) → choose RM 30,000

- Net gain = RM 270,000

- If sold in 5th year, rate = 15% → tax payable = RM 270,000 x 15% = RM 40,500

Check comparable listings on PropertyGuru Malaysia

See how similar properties are priced in today’s market.

Step-by-Step Filing Process for RPGT & Claiming Exemptions

It’s essential to understand that RPGT filing is a structured process that requires accuracy, proper documentation, and adherence to the prescribed timelines.

Here’s a clear step-by-step outline to help you complete your submission smoothly and claim any applicable exemptions with confidence.

- Fill out Form CKHT-1A for the disposer and Form CKHT-2A for the acquirer.

- If you intend to claim an exemption (e.g., once-in-a-lifetime for private residence), you must make an election in writing under Section 8 of the RPGT Act.

- For disposals on or after 1 January 2025, the self-assessment system applies: you must calculate, report, and pay within 90 days of disposal. The CKHT-1A and CKHT-2A forms remain mandatory under this framework, even though the computation is now self-declared.

- Maintain comprehensive documentation, including acquisition costs, improvement costs, legal/agent fees, valuation reports, and SPA. Without supporting proof, you may lose deductions.

Once your filing is complete, monitor your submission status and keep copies of all supporting documents for future reference.

Tax-Planning Tips: Using Exemptions Strategically

With Malaysia’s Real Property Gains Tax (RPGT) framework evolving under the self-assessment system, strategic timing and proper documentation have never been more crucial.

Here are several practical ways to optimise available exemptions and minimise your RPGT liability:

- If your holding period is approaching six years, and you’re a citizen/PR, there may be merit in waiting to qualify for the nil rate rather than disposing early, but you must weigh this against market risk.

- If the property is your only residence and you haven’t used the once-in-a-lifetime private residence relief, ensure you meet all the conditions and apply promptly.

- Always apply the RM 10,000/10% per-disposal relief if eligible; it’s a simple, often-overlooked benefit.

- For low-cost homes (previously defined as properties valued at RM 200,000 or less), an exemption applied under Budget 2019 for disposals after five years. However, this was a past exemption category, and as of 2025, it is subject to reinstatement or further policy updates. Check the latest announcements from LHDN and MOF for confirmation.

- Use PropertyGuru Malaysia’s resources (guides, listing trends, market data) to decide timing and pricing strategy.

- Maintain proper documentation to support allowable deductions, including legal/agent fees, improvements, and valuations.

- File early and accurately under the self-assessment system, as your liability is now primarily on you. Late or incorrect filing can trigger additional penalties.

After going through these tips, take your planning a step further so you’ve bought an investment property. Now what?

Navigating RPGT exemptions in Malaysia for the 2025 financial year requires careful planning, up-to-date awareness of the rules, and strategic decision-making.

By understanding which reliefs apply to you, whether it is the RM10,000/10% basic exemption, the once-in-a-lifetime private residence exemption, for which the election must be made in the CKHT-3 notification within 90 days, family transfers, or the low-cost home relief, you can significantly reduce your tax liability and preserve more of your sale proceeds.

PropertyGuru Malaysia offers up-to-date guides, market insights, and resources to help you plan your property strategy with confidence. Explore Property Guides Now!

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.