When preparing to buy, sell, or invest in real estate, you’ll often hear the phrase’ property valuation.’ It’s a vital part of the process that determines your property’s actual value, not just what someone is willing to pay.

In today’s Malaysian property market, where prices fluctuate due to economic trends, infrastructure growth, and changing demand, understanding how a valuer property works can help you make smarter, risk-free decisions.

In this guide, we’ll explore how property valuation works in 2026, who the valuer is, how banks rely on them, what affects valuation accuracy, and why you should never skip this step, whether you’re a buyer, seller, or investor.

Looking for a place to rent in Malaysia?

Filter by price, location, and space that works for you.

What Is Property Valuation?

Property valuation is a professional assessment of a property’s current market value, conducted by a certified valuer. It serves as an impartial benchmark for banks, developers, and buyers to determine a fair price before a sale, purchase, or refinancing.

Unlike market value, which reflects what a buyer and seller are willing to agree on, valuation is based on objective analysis. A qualified valuer considers recent comparable transactions, prevailing market trends, the property’s physical condition, location, and other measurable factors to arrive at an evidence-based figure.

In Malaysia, all valuations are guided by data from the Valuation and Property Services Department (JPPH) and regulated under the Board of Valuers, Appraisers, Estate Agents, and Property Managers (BOVAEP), also known by its Malay acronym LPPEH. This ensures transparency, professionalism, and consistency in determining property values nationwide.

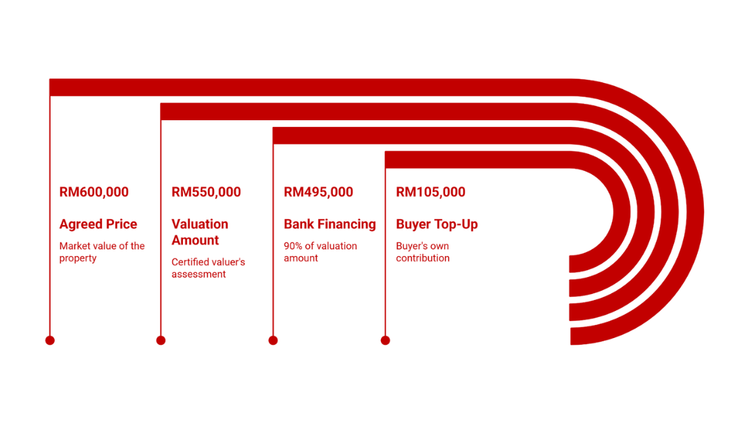

Example of How Valuation Affects Financing:

In this case, even though the buyer and seller agree on RM600,000, the bank will only finance up to 90% of the valuation amount (RM550,000).

The buyer must therefore cover the RM105,000 shortfall from their personal funds.

Explore properties for sale across Malaysia

Find homes that match your budget

Who Is a Property Valuer and What Do They Do?

A valuer is a licensed property professional registered with the Board of Valuers, Appraisers, Estate Agents, and Property Managers (BOVAEP). Their core responsibility is to determine a property’s fair and accurate market value through an impartial, evidence-based assessment.

Unlike agents or developers, valuers operate independently, ensuring that every appraisal is free from commercial bias. Their expertise enables both financial institutions and private buyers to make informed, data-driven decisions, whether for loan approvals, investment analysis, or estate planning.

In practice, a valuer’s work typically involves the following steps:

- Conducting thorough site inspections: to examine the property’s condition, layout, and quality of finishes.

- Assessing features and specifications, such as land area, built-up size, accessibility, and surrounding amenities.

- Analysing recent comparable sales: using verified data from the Valuation and Property Services Department (JPPH) to anchor their findings to real market activity.

- Preparing an official valuation report, which is then submitted to the client or financing bank as a professional record of value.

Most Malaysian banks either maintain a panel of approved valuers or operate their own in-house valuation teams. For investors and homebuyers, however, engaging an independent valuer can be particularly useful for assessing potential rental yields and capital appreciation, or for deciding between competing developments.

A credible valuation not only protects buyers from overpaying but also strengthens an investor’s ability to negotiate confidently, ensuring every property decision rests on a solid financial footing.

How Property Valuation Works in Malaysia?

Understanding how the valuation process unfolds can help buyers and investors appreciate the importance of this crucial step in any property transaction.

In Malaysia, valuations form the basis for bank financing, ensuring that loans are granted based on a property’s market value rather than the agreed purchase price.

Here’s a simplified step-by-step overview of how it typically works:

- Loan Application: The process begins when the buyer submits a loan application for a housing loan. The bank then requires an official valuation to confirm the property’s fair market value.

- Appointment of Valuer: The bank assigns the task to a certified valuer from its approved panel to ensure objectivity and compliance with BOVAEP standards.

- Market Data Analysis: The valuer reviews recent transaction data from the Valuation and Property Services Department (JPPH), focusing on comparable sales within the same area and property type.

- On-Site Inspection: A detailed physical inspection follows, where the valuer assesses the property’s structure, finishes, neighbourhood appeal, and overall condition.

- Preparation of Valuation Report: The findings are consolidated into a formal valuation report that outlines the property’s current market value, supported by data and reasoning.

- Bank Loan Approval: Based on this valuation, the bank determines the financing amount, typically up to 90% of the appraised value, depending on the borrower’s profile and loan eligibility.

This process protects both parties: the bank is safeguarded from over-financing, and the buyer gains reassurance that the property price reflects real market conditions.

In a fast-moving market, this independent valuation serves as a reality check, keeping financial decisions grounded in data rather than sentiment.

Different Methods of Property Valuation

Not all properties are valued equally. Professional valuers in Malaysia employ various approaches, depending on the property’s nature, use, and income potential.

Each method offers a unique lens to determine what a property is truly worth in current market conditions:

1. Comparison Method

This is the most commonly used technique, particularly for residential properties. It involves analysing recent transactions of similar properties within the exact location, adjusting for differences such as lot size, floor area, renovations, or view. The result reflects what a willing buyer would be willing to pay in today’s market.

This is the most commonly used technique, particularly for residential properties. It involves analysing recent transactions of similar properties within the exact location, adjusting for differences such as lot size, floor area, renovations, or view. The result reflects what a willing buyer would be willing to pay in today’s market.

2. Investment Method

Primarily used for rental properties, this method evaluates a property based on its income-generating potential. Valuers calculate the property’s capital value by estimating the annual rental income and applying an appropriate yield rate. It’s a preferred model for investors assessing long-term returns.

Primarily used for rental properties, this method evaluates a property based on its income-generating potential. Valuers calculate the property’s capital value by estimating the annual rental income and applying an appropriate yield rate. It’s a preferred model for investors assessing long-term returns.

3. Cost Method

Here, the valuer estimates the current cost of rebuilding or replacing the property, then deducts depreciation based on age, wear, and functional obsolescence. This method is typically applied to specialised or newly built assets, where comparable sales data may be limited.

Here, the valuer estimates the current cost of rebuilding or replacing the property, then deducts depreciation based on age, wear, and functional obsolescence. This method is typically applied to specialised or newly built assets, where comparable sales data may be limited.

4. Residual Method

Commonly used for development land, this approach calculates the potential value of a completed project and then subtracts the estimated costs of construction, financing, and marketing. The remainder indicates the land’s present value, helping developers gauge project viability.

Commonly used for development land, this approach calculates the potential value of a completed project and then subtracts the estimated costs of construction, financing, and marketing. The remainder indicates the land’s present value, helping developers gauge project viability.

5. Profit Method

Applied to properties such as hotels, petrol stations, or restaurants, this method bases valuation on the business’s profitability rather than the property alone. It accounts for turnover, operating expenses, and net profit before capitalising an appropriate yield.

Applied to properties such as hotels, petrol stations, or restaurants, this method bases valuation on the business’s profitability rather than the property alone. It accounts for turnover, operating expenses, and net profit before capitalising an appropriate yield.

Each method serves a distinct purpose, but together, they form the foundation of Malaysia’s professional valuation standards, ensuring accuracy, transparency, and investor confidence across every segment of the property market.

Why Valuations Differ from Market Prices?

While both valuation and market price aim to reflect a property’s worth, they often diverge, sometimes by a surprising margin.

This difference arises because valuation is an objective, data-driven process, whereas market price is ultimately shaped by sentiment, urgency, and negotiation between buyer and seller.

1. Time Lag in JPPH Data

JPPH data may lag actual transactions by 3 to 6 months, affecting accuracy in fast-moving markets.

2. Economic Conditions

Changes in interest rates or new Government policies can significantly impact property demand, causing values to fluctuate rapidly.

3. Renovations and Upgrades

Not all renovations increase value. Functional upgrades, such as permitted extensions, new flooring, built-ins, and smart home systems, typically boost valuation; cosmetic ones may not.

4. Location and Accessibility

Proximity to highways, MRT (Mass Rapid Transit) stations, such as MRT Kajang (KG), or lifestyle amenities significantly impacts valuation.

5. Feng Shui and Environmental Factors

Believe it or not, many Malaysians still consider feng shui elements to be essential. For example, homes facing a T-junction may be valued slightly lower due to safety and practical concerns.

Ultimately, while the market price reflects what a buyer is willing to pay at a given moment, a valuation represents what a qualified professional believes the property is worth.

Understanding both perspectives allows buyers and sellers to negotiate more confidently and make informed financial decisions.

Top Factors Affecting Property Value in 2026

As Malaysia’s property market evolves, valuers are placing greater emphasis on elements that reflect modern living standards and long-term sustainability.

Beyond size and location, factors such as digital readiness, eco-conscious design, and neighbourhood infrastructure are now key determinants of value.

| Factor | Description |

| Green Building Features | Eco-friendly materials, energy-efficient lighting, and solar systems can raise value. |

| Smart Home Integration | Properties with IoT systems (e.g., smart locks and thermostats) appeal to tech-savvy buyers. |

| Connectivity | Proximity to MRT lines, expressways, and central business districts boosts value. |

| Community Development | Nearby shopping centres, such as The Exchange TRX and Pavilion Damansara Heights, increase the area’s desirability. |

| Safety and Security | Gated communities with 24-hour security and surveillance systems command higher valuations. |

These features not only future-proof value but also align with what buyers and tenants increasingly prioritise: comfort, connectivity, and conscientious living.

In short, properties that blend convenience, technology, and sustainability are standing out in 2026’s competitive market.

When and How to Get Your Property Valued?

Timing and process are everything in property valuation. Whether you’re buying, selling, refinancing, or managing an investment portfolio, obtaining an accurate and professional assessment can make all the difference in your financial planning.

You should consider obtaining a valuation when:

- Buying or selling a property: to ensure you’re paying or receiving a fair price.

- Applying for a refinance: banks rely on valuations to determine your loan eligibility.

- In settling estates or divorce matters, valuations establish an equitable division of assets.

- Filing Real Property Gains Tax (RPGT): an official valuation helps determine taxable gains.

- Tracking investment growth: Annual revaluations enable investors to measure appreciation and adjust their strategy accordingly.

Once you engage a certified valuer, the process unfolds in several steps designed to ensure transparency and accuracy:

- Data Analysis: The valuer begins by reviewing transaction data from the Valuation and Property Services Department (JPPH) and other verified sources.

- Site Inspection: A physical inspection follows, assessing property condition, location, and unique features.

- Market Comparison: Comparable transactions are adjusted to reflect current market conditions.

- Valuation Report: A detailed report is prepared, outlining the valuation figure and rationale.

- Bank Assessment: If financing is involved, your lender uses this valuation to determine how much you can borrow.

A clear understanding of when and how valuations are conducted helps ensure you make informed, confident decisions, avoiding the common pitfalls of overpayment, underfinancing, or unrealistic expectations.

Work out your loan instalments quickly

Stay within a budget that fits your lifestyle.

Choosing the Right Valuer and Avoiding Costly Mistakes

A property valuation is only as reliable as the person conducting it. Selecting a qualified, ethical valuer not only guarantees professional accuracy but also protects your interests throughout the transaction.

When appointing a valuer, always:

- Verify registration with BOVAEP (Board of Valuers, Appraisers, Estate Agents, and Property Managers).

- Verify their experience with your specific property type, such as residential, commercial, or industrial.

- Inquire about the turnaround time and the valuation methods used.

- Compare professional fees, which are standardised under the Valuers, Appraisers, and Estate Agents Act 1981.

At the same time, be mindful of common valuation misconceptions that could cost you:

- Don’t assume the asking price equals market value.

- Avoid comparing with listings; always rely on actual transacted prices.

- Never pressure a valuer to inflate figures; their code of ethics requires them to be objective.

- If the valuation comes in lower than expected, use it as a negotiation point or reassess your financing options.

Ultimately, a professional valuation isn’t just a procedural step; it’s your safeguard against misjudgement. By selecting the right expert and adhering to the process, you lay the foundation for a fair, transparent, and financially sound transaction.

Time To Make Your Move

Whether you’re planning to buy, sell, or invest, a trusted property valuer ensures transparency and accuracy in the valuation process.

Start your property journey confidently by browsing the latest verified listings on PropertyGuru Malaysia or exploring our in-depth property guides to make informed decisions.

Keep Track of New Launches

Visit our new launches page to find the new launch project of your dreams and submit an enquiry today.

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.