Your credit profile is one of the most important aspects of your financial health. Whether you are planning to buy your first home, apply for a car loan, or simply want to maintain financial discipline, understanding your creditworthiness is essential.

In Malaysia, one of the key tools for assessing your financial standing is the CTOS Report, provided by CTOS Data Systems Sdn Bhd. This report provides a comprehensive view of your credit history and is widely used by banks, property developers, and other financial institutions to evaluate loan applications.

In this guide, we explain what the CTOS Report is, how to check your credit score, and 10 actionable steps you can take to improve it.

| Table of Contents 1. What Is a CTOS Score? 2. How to Check Your CTOS Credit Score (Step-by-Step) 3. 10 Steps to Improve Your CTOS Score in Malaysia 4. Why Your CTOS Score Matters for Property Buyers in 2025 5. Get Credit-Ready Before You Buy Your Dream Home |

Find Properties That Match Your Loan Eligibility

Discover homes within your approved financing range across Malaysia.

What is a CTOS Score?

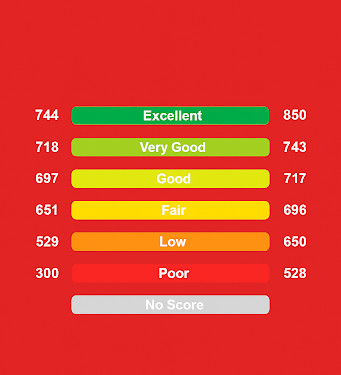

Your CTOS Score is a numeric representation of your creditworthiness, ranging from 300 to 850. The score is calculated based on factors such as repayment history, outstanding loans, credit utilisation, and any legal or bankruptcy records.

How it works:

- CTOS uses the internationally recognised FICO scoring methodology, which is trusted by lenders worldwide.

- A higher score indicates better financial discipline and reliability.

- When you apply for credit, such as a home loan, personal loan, or credit card, banks and financial institutions typically check your CTOS Score as part of their risk assessment.

A strong CTOS Score not only improves your chances of getting approved for loans but may also help you secure better interest rates and more favourable financing terms. Conversely, a low score may result in higher interest rates, stricter loan conditions, or even rejection.

How to Check Your CTOS Credit Score (Step-by-Step)

Checking your CTOS Report is a crucial step if you are planning to apply for a loan or buy property in Malaysia. A correct understanding of your credit profile can help you secure better financing terms and avoid surprises. Here’s the step-by-step process for 2025:

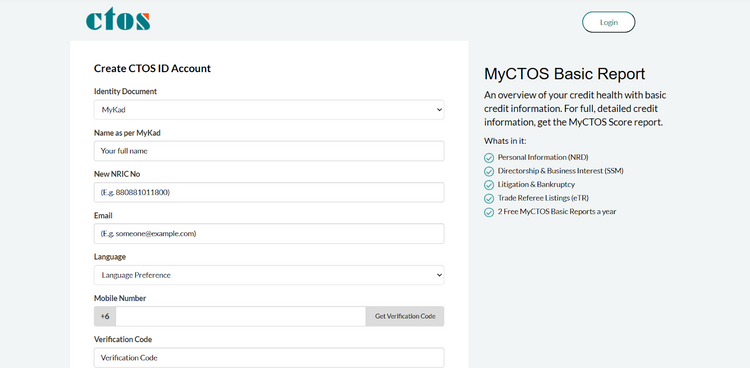

Step 1: Register on the CTOS Website or MyCTOS App

- Visit the CTOS official website or download the MyCTOS mobile app from Google Play or the Apple App Store.

- Click Register or Sign Up and enter your NRIC/new IC or passport number, email address, and mobile number.

- Create a secure password, then confirm your registration via the email or OTP link sent by CTOS.

- Once your account is active, you can log in to access CTOS services.

Step 2: Choose the Report Type

CTOS offers three main options:

- MyCTOS Basic Report – includes basic credit information, available for free or at minimal cost twice a year.

- MyCTOS Score Report – full credit report with CTOS Score (300–850), CCRIS records, and more; cost ~RM 26.50–RM 27.

- CTOS SecureID – subscription-based service with credit monitoring, fraud alerts, and identity protection; ~RM 99/year.

PropertyGuru Tip: For property financing, it is recommended to provide lenders with a complete picture of your creditworthiness through the Score Report.

Step 3: Verify Your Identity

Alt text: Malaysian ID card with key features highlighted. | Source: CTOS

- To comply with Malaysian regulations, CTOS requires identity verification.

- Upload your IC or passport, a clear photo of yourself, and proof of address if required.

- Verification typically takes a few hours to a day. Once complete, your profile will be activated for report access.

Step 4: Access and Download the Report

- After logging in, navigate to My Reports or Download Report.

- Select your purchased or free report and click either ‘Download’ or ‘View’. Reports are usually in PDF format.

- Save a copy to your device, and optionally print a physical copy for your records.

Step 5: Review the Report and Identify Errors

Check the following key sections:

- Personal identification

- CTOS Score

- Outstanding loans and credit facilities

- Business directorships or ownerships

- Litigation or bankruptcy records

- CCRIS summary

Look for any inaccuracies, such as:

- Accounts you do not recognise

- Settled loans are still showing as active.

- Legal or bankruptcy records that are outdated

- Incorrect personal or contact information

PropertyGuru Tip: Identifying errors early prevents issues when applying for a home loan.

Step 6: Dispute Inaccuracies with CTOS

If you find any inaccuracies or entries that should no longer appear on your report, please notify us. Call us at (03) 2722 8833, complete the online form, or email your details to sarus@ctos.com.my.

PropertyGuru Tip: File disputes 3–6 months before applying for a property loan to ensure lenders see an accurate credit profile.

Checking your CTOS credit score helps you understand your financial standing, correct errors early, and improve your chances of getting better loan offers when buying property.

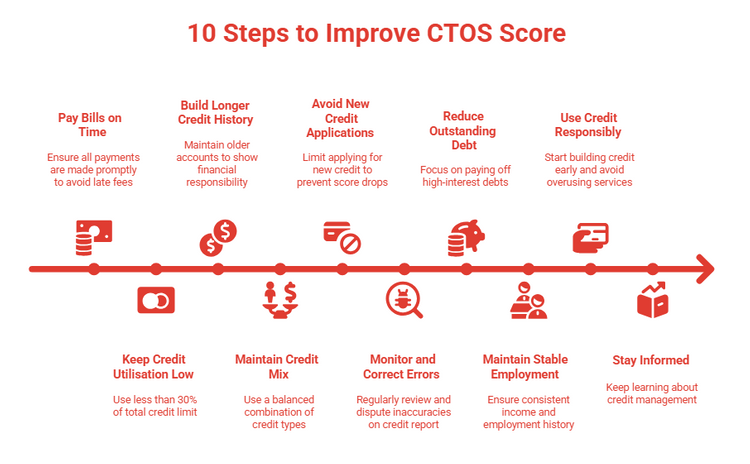

10 Steps to Improve Your CTOS Score

Improving your CTOS Score takes time, consistency, and good financial habits. Whether you’re planning to buy a home, refinance an existing home loan, or simply maintain a strong financial profile, these ten practical steps will help you strengthen your credit standing in Malaysia.

1. Pay All Bills and Instalments on Time

Late or missed payments have the biggest negative impact on your credit score. Your payment history accounts for a significant portion of your CTOS Score, reflecting your reliability as a borrower.

What to Do:

- Set up automatic payments or reminders for all credit cards, loans, and utilities.

- Schedule payments after salary day to ensure sufficient funds.

- Always pay at least the minimum due amount on time, even if you cannot pay in full.

PropertyGuru Tip:

Banks view on-time payments as a sign of responsible financial behaviour. A clean payment record enhances your chances of securing a mortgage with competitive or lower home loan interest rates.

Banks view on-time payments as a sign of responsible financial behaviour. A clean payment record enhances your chances of securing a mortgage with competitive or lower home loan interest rates.

2. Keep Your Credit Utilisation Low

Your credit utilisation ratio, the percentage of available credit you’re using, directly affects your score. High balances on your credit cards or revolving credit lines signal financial stress.

What to Do:

- Keep credit usage below 30% of your total limit.

- Pay off balances in full whenever possible.

- Request a limit increase (without increasing spending) to lower your utilisation rate.

Example:

If your card limit is RM 10,000, try not to exceed RM 3,000 at any time.

If your card limit is RM 10,000, try not to exceed RM 3,000 at any time.

3. Build a Longer Credit History

The longer you’ve managed credit responsibly, the more confidence lenders have in your stability.

What to Do:

- Keep old credit cards or loan accounts open and active (if no annual fees).

- Use them occasionally for small transactions and pay them off promptly.

- Avoid cancelling old accounts too quickly, as it shortens your credit history.

PropertyGuru Tip:

Borrowers with a longer, positive credit history are often seen as "low-risk" by mortgage lenders.

Borrowers with a longer, positive credit history are often seen as "low-risk" by mortgage lenders.

4. Maintain a Healthy Mix of Credit Types

A mix of credit shows that you can manage different types of obligations, such as short-term (credit cards) and long-term (car or home loans).

What to Do:

- Combine different types of credit (credit card, hire purchase, personal loan, etc.) responsibly.

- Avoid taking multiple new loans just to diversify; apply only when needed.

Example:

A person managing a car loan, one credit card, and a personal loan responsibly is seen more favourably than someone with multiple short-term credit cards maxed out.

A person managing a car loan, one credit card, and a personal loan responsibly is seen more favourably than someone with multiple short-term credit cards maxed out.

5. Avoid Frequent New Credit Applications

Each credit application triggers a “hard inquiry” on your CTOS Report, which can temporarily lower your score.

What to Do:

- Space out your credit applications, and avoid applying for multiple cards or loans at once.

- Apply only when absolutely necessary, especially if you plan to take a home loan soon.

- Check your eligibility before applying to reduce the chances of rejection.

PropertyGuru Tip:

Frequent rejections can make lenders perceive you as high-risk.

Frequent rejections can make lenders perceive you as high-risk.

6. Monitor and Correct Errors on Your Report

Incorrect or outdated data, such as wrongly listed debts or identity mix-ups, can lower your score..

What to Do:

- Review your CTOS Report at least once a year, especially before applying for credit.

- Flag suspicious accounts, unfamiliar debts, or outdated court cases.

- Use the CTOS dispute form to correct issues quickly (as outlined in Step 6).

PropertyGuru Tip:

Always ensure your report is accurate before submitting home-loan documents. Banks verify your score against this data.

Always ensure your report is accurate before submitting home-loan documents. Banks verify your score against this data.

7. Reduce Outstanding Debt Gradually

High levels of debt, especially unsecured debt like credit cards or personal loans, can weigh down your CTOS Score.

What to Do:

- Prioritise paying off high-interest debts first (e.g., credit cards).

- Consider the "debt avalanche" method, which focuses on paying off the debt with the highest interest rate first, then moving down.

- Avoid taking new loans unless necessary.

Example:

If you have RM 20,000 in personal loans and RM 10,000 in credit card balances, start reducing your credit card debt to demonstrate a lower risk profile.

If you have RM 20,000 in personal loans and RM 10,000 in credit card balances, start reducing your credit card debt to demonstrate a lower risk profile.

8. Maintain Stable Employment and Income

Consistency in income reassures lenders that you can meet repayment obligations, even if this doesn’t directly change your CTOS Score.

What to Do:

- Keep your employment steady for at least 6–12 months before applying for major loans.

- If self-employed, maintain verifiable records of income (bank statements, invoices, tax filings).

- Avoid large employment gaps when preparing for mortgage loan approval.

PropertyGuru Tip:

A stable income, combined with a healthy CTOS Score, gives banks greater confidence in approving your home loan.

A stable income, combined with a healthy CTOS Score, gives banks greater confidence in approving your home loan.

9. Use Credit Responsibly from Early On

Start building your credit profile even if you are young or have no prior history. Responsible use over time helps create a solid foundation.

What to Do:

- Use a credit card for small purchases and pay it off monthly.

- Avoid maxing out new credit lines.

- Avoid relying excessively on "buy now, pay later" options, as they can lead to unanticipated debt.

Example:

A young graduate who uses one credit card wisely for a few years will likely have a stronger score than someone who starts managing credit later.

A young graduate who uses one credit card wisely for a few years will likely have a stronger score than someone who starts managing credit later.

10. Stay Informed and Financially Literate

Understanding how the credit system works helps you make smarter financial choices.

What to Do:

- Read guides from trusted sources, such as Bank Negara Malaysia and CTOS Data Systems.

- Attend online workshops or webinars on financial literacy.

- Stay alert for scams or fraudulent activities that could damage your credit.

PropertyGuru Tip:

The more you understand about how your credit profile is built and maintained, the better your chances of getting favourable property loan terms.

The more you understand about how your credit profile is built and maintained, the better your chances of getting favourable property loan terms.

Improving your CTOS Score is not instant; it usually takes three to six months of consistent effort.

The key is steady progress: paying on time, reducing debt, and maintaining a clean credit report.

DOWNLOAD THE PROPERTYGURU APP

Tired of searching every day? Save your preferences and get curated listings on the go.

Why Your CTOS Score Matters for Property Buyers in 2025

When applying for a home loan in Malaysia, your CTOS Score plays a major role in determining whether you get approved and on what terms. Lenders use your credit profile to evaluate how financially reliable you are and how much risk they’re taking by lending to you.

A higher score signals that you’re a responsible borrower, while a lower one can limit your chances of approval or lead to higher borrowing costs.

A higher score signals that you’re a responsible borrower, while a lower one can limit your chances of approval or lead to higher borrowing costs.

1. Why Banks Check Your CTOS Score Before Approving a Home Loan

In 2025, Malaysian banks are expected to rely on both CTOS and CCRIS (Central Credit Reference Information System, operated by Bank Negara Malaysia) when assessing loan applications.

Your CTOS Report provides insights into your repayment behaviour, outstanding loans, and any legal or bankruptcy history, helping lenders determine whether you’re a low-risk or high-risk applicant.

Your CTOS Report provides insights into your repayment behaviour, outstanding loans, and any legal or bankruptcy history, helping lenders determine whether you’re a low-risk or high-risk applicant.

Most financial institutions follow a credit grading system, where:

- High CTOS Scores (above 700) = Low-risk borrower → higher approval chances

- Medium CTOS Scores (650–699) = Moderate-risk borrower → approval possible but with stricter terms

- Low CTOS Scores (below 650) = High-risk borrower → higher rejection likelihood or higher interest rate

Example:

If two applicants apply for a RM 500,000 home loan:

If two applicants apply for a RM 500,000 home loan:

Applicant A has a CTOS Score of 760 and a clean payment history, so the application is approved quickly, and a lower rate is offered.

Applicant B has a CTOS Score of 580 with a history of missed payments, so they may be required to provide a larger down payment or a guarantor.

2. How Your CTOS Score Affects Interest Rates and Loan Terms

Your credit score doesn’t just determine approval; it also influences the interest rate and loan conditions you receive.

Banks reward financially disciplined borrowers with lower rates because they represent lower default risk.

Banks reward financially disciplined borrowers with lower rates because they represent lower default risk.

For example:

750 – 850

Excellent

Very High (90%+)

Typically, access to the lowest interest rates offered by lenders

700 – 749

Good

High (70–85%)

Likely to receive competitive interest rates, slightly above the top tier

650 – 699

Fair

Moderate (40–60%)

May face moderately higher rates due to perceived risk

530 – 649

Low

Low (20–30%)

Usually, higher interest rates reflect higher credit risk

Below 530

Weak

Very Low / Likely rejected

Loan approval unlikely; if approved, interest rates will be significantly higher

As of June 2025, most major banks offer effective lending rates for a typical 30-year housing loan of RM350,000 in the range of about 4.15% to 5.67% per year. Some promotional packages may provide slightly lower rates based on the borrower’s financial profile and the specific loan terms.

PropertyGuru Tip:

Even a 0.5% difference in interest rate can save you tens of thousands of ringgit over a 30-year mortgage.

Even a 0.5% difference in interest rate can save you tens of thousands of ringgit over a 30-year mortgage.

3. Impact on Down Payment and Loan Margin

Banks determine how much they can safely lend to you based on your credit profile. With a strong CTOS Score, you may qualify for a higher margin of financing, up to 90% for first-time buyers. Malaysia also offers the "My First Home Scheme" (Rumah Pertamaku), which allows eligible first-time buyers to obtain up to 100% financing, meaning they can secure a full housing loan.

If your score is weak, the bank may approve only 70%–80% of the loan amount, requiring you to pay a larger down payment up front.

Example:

- High Score (750+) → 90% loan margin → RM 50,000 down payment on RM 500,000 home.

- Low Score (600) → 75% loan margin → RM 125,000 down payment on the same home.

This difference can make or break a property purchase, especially for first-time home buyers.

4. Common CTOS-Related Issues That Affect Loan Applications

When reviewing your CTOS Report, lenders often focus on red flags such as:

- Missed or late payments

- Outstanding or high unsecured debt (e.g., credit cards, personal loans)

- Litigation or bankruptcy records

- Frequent credit applications within a short period

- Overlapping loans that indicate financial strain

Even if you’ve cleared old debts, some records remain visible for up to 24 months after settlement.

That’s why checking your report regularly helps ensure lenders see the most accurate picture.

That’s why checking your report regularly helps ensure lenders see the most accurate picture.

5. How to Prepare Your Credit Profile Before Applying for a Home Loan

To increase your chances of approval, plan 3–6 months ahead:

- Check your CTOS Report for errors or outdated information.

- Dispute inaccuracies and ensure updates are reflected before applying.

- Pay down high-interest debt and reduce credit utilisation below 30%.

- Avoid new credit applications during this period.

- Maintain consistent employment and income proof (salary slips, EPF, or tax filings).

A little preparation can make a big difference in your final approval outcome.

6. PropertyGuru Tip: Use Tools and Listings Wisely

Once your CTOS Score is in a healthy range, explore properties confidently using PropertyGuru’s tools:

- Try our Home Loan Tools and Calculators to get an estimate of your monthly home loan payments.

- Browse homes within your approved budget using our latest Property Listings.

With the right credit profile and preparation, your dream of owning a home in Malaysia can become a reality faster than you think.

See Your Home Budget In Seconds

Estimate your monthly repayments and find out how much home you can afford.

Get Credit-Ready Before You Buy Your Dream Home

Planning to apply for a home loan or purchase your first property in 2025 or 2026? Before you start browsing listings, take a moment to review your CTOS Report and understand your current credit health.

A strong CTOS Score not only improves your chances of loan approval but can also help you secure better interest rates and higher financing margins from banks.

By following the steps in this guide, such as regularly checking your report, disputing errors, and developing good credit habits, you’ll be in a stronger position to confidently achieve your property goals.

For more insights on financial readiness, home loans, and property buying tips, visit the PropertyGuru Guides Section.

Still searching for your ideal home? Check out the exclusive sale listing on PropertyGuru Malaysia today!

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.