In July 2025, Bank Negara Malaysia cut the Overnight Policy Rate (OPR) by 25 basis points to 2.75 percent. While this move offers some relief for borrowers, housing loan interest remains one of the biggest long-term costs for Malaysian homeowners.

If you have been wondering how to make the most of lower rates, one key decision is whether to make advance payments vs reduce your loan principal. Both options can help you save interest, but they work in very different ways.

In this guide, we explain how Malaysian home loan interest is calculated, explore both repayment strategies, and share practical steps to help you lower your total interest and pay off your loan sooner.

Find Properties That Match Your Budget

Find homes across Malaysia that fit your financing range.

How Housing Loan Interest Works in Malaysia

Before deciding how to save on your housing loan, it helps to understand how banks calculate interest in Malaysia, because this is what determines how much you can actually save.

Most Malaysian housing loans follow what’s called the reducing balance method. This means that your monthly instalment covers two parts:

- Interest, which is calculated on the outstanding loan amount, and

- Principal, which gradually reduces your total balance.

At the start of your loan, a larger share of your repayment goes toward interest. Over time, as your principal decreases, the interest portion also gets smaller. The faster you lower your principal, the less total interest you’ll pay.

Here’s where it gets interesting: banks calculate interest based on different structures such as term loans, semi-flexi loans, and full flexi loans. These determine how easily you can make extra payments and how those payments are treated.

If you’ve ever made an additional payment and noticed your instalment amount or tenure didn’t change, it’s likely because your loan type doesn’t automatically apply extra funds to reduce your principal.

And that’s exactly why understanding your repayment structure is key before deciding between an advance loan payment or principal reduction.

Advance Loan Payment vs Reduce Loan Principal: What’s the Difference?

When it comes to paying off your housing loan faster, two terms often come up: advance loan payment vs reduce loan principal. They may sound similar, but in reality, they work very differently and can have a big impact on how much interest you pay.

Let’s break it down in simple terms.

Advance Loan Payment

An advance loan payment means paying your future instalments ahead of time. For example, if your monthly instalment is RM2,000 and you decide to pay RM4,000 this month, your bank will treat the extra RM2,000 as a prepayment for upcoming months.

This means your next month’s payment is already covered, but your outstanding principal, or the amount you owe, remains the same. Since interest is still calculated on that balance, you will not see a major difference in the total interest payable over time.

This means your next month’s payment is already covered, but your outstanding principal, or the amount you owe, remains the same. Since interest is still calculated on that balance, you will not see a major difference in the total interest payable over time.

In short, an advance payment gives you temporary breathing space but doesn’t reduce your loan faster.

Reduce Loan Principal

A principal reduction, on the other hand, directly lowers the amount you owe the bank. When you pay extra and specify that it should go toward your principal, your outstanding balance decreases immediately.

As a result, future interest is calculated on a smaller amount, helping you save more in the long run.

As a result, future interest is calculated on a smaller amount, helping you save more in the long run.

This method works best with flexi or semi-flexi loans, where extra payments automatically reduce your principal. However, some term loans require you to submit a formal request for the payment to be applied this way.

Side-by-Side Comparison

To make things clearer, here’s a quick side-by-side comparison of Advance Loan Payment versus Reduce Loan Principal:

Purpose

Pays off future instalments in advance

Reduces the outstanding principal immediately

Impact on Interest

Minimal, as interest continues on the same balance

Significant, as interest is recalculated on a smaller balance

Loan Tenure

Usually unchanged

Can shorten tenure or reduce total payable interest

Flexibility

Offers short-term relief; easy to do

Long-term saving may require bank approval for term loans

Best For

Borrowers who want short-term convenience or flexibility

Borrowers aiming to reduce total loan cost and finish payments sooner

Common Loan Types

Often used in term loans

Works best with semi-flexi or full-flexi loans

Which One Is Right for You?

- If you’re looking for temporary relief, say, to skip a payment or two when you have extra cash, an advance payment might be convenient.

- But if your goal is to reduce your total interest and shorten your loan period, reducing your principal is far more effective.

Before deciding, check your loan agreement or ask your bank how extra payments are applied. Some lenders treat additional payments as advance instalments by default unless you specify otherwise.

Estimate Your Monthly Home Loan Repayments

Use our Home Loan Calculator to find out how different loan amounts, tenures, and interest rates affect your monthly instalments.

Which Option Actually Saves More Interest?

If you suddenly have extra cash, maybe from a bonus or investment return, it is natural to wonder whether using it to pay off part of your home loan will help you save more in the long run. The answer depends on how your bank treats that extra payment.

Most Malaysian homeowners fall into one of two approaches: making advance payments or reducing the loan principal. They may sound similar, but they work very differently.

Advance Loan Payment

When you make an advance payment, you are paying your future instalments ahead of time. For example, if your monthly instalment is RM2,000 and you pay RM4,000 this month, your bank will likely treat the extra RM2,000 as next month’s instalment.

When you make an advance payment, you are paying your future instalments ahead of time. For example, if your monthly instalment is RM2,000 and you pay RM4,000 this month, your bank will likely treat the extra RM2,000 as next month’s instalment.

This can be convenient if you want flexibility or expect changes in income. However, it does not actually lower your outstanding loan balance, so interest continues to be charged on the same amount. In other words, it buys you breathing room, not big savings.

Reduce Loan Principal

When you pay directly toward your principal, your outstanding balance drops immediately. Because housing loan interest in Malaysia is calculated on a reducing balance basis, this smaller balance means less interest charged each month.

When you pay directly toward your principal, your outstanding balance drops immediately. Because housing loan interest in Malaysia is calculated on a reducing balance basis, this smaller balance means less interest charged each month.

The long-term savings can be significant.

For instance, on a RM400,000 loan at 4% interest over 30 years, paying an extra RM20,000 toward your principal could save around RM30,000 in total interest and shorten your loan by nearly two years.

For instance, on a RM400,000 loan at 4% interest over 30 years, paying an extra RM20,000 toward your principal could save around RM30,000 in total interest and shorten your loan by nearly two years.

This approach is more effective if your loan is semi-flexi or full-flexi, since these allow extra payments to go straight to your principal. For term loans, you may need to request this arrangement from your bank.

Advance Payment vs Principal Reduction: A Quick Comparison

Now that you understand how both methods work, here’s a side-by-side look at how they differ in real terms.

How It Works

Pays instalments in advance

Directly lowers your balance

Effect on Interest

Minimal

Significant savings

Impact on Tenure

Usually unchanged

Often shortens the loan

Flexibility

High – easier to access funds later

Moderate – depends on loan type

Best For

Short-term convenience

Long-term financial savings

If your goal is to reduce your total loan cost and pay off your mortgage faster, applying extra funds to your loan principal is the smarter choice. If you prefer short-term flexibility, such as covering future instalments, advance payments may suit you better.

Before making a decision, ask your bank exactly how extra payments are handled. A quick check can ensure your money truly reduces your debt, not just pays your loan ahead of schedule.

Understanding the Different Types of Housing Loans

Before deciding how to make extra payments, it’s helpful to know the type of housing loan you have. Each loan structure in Malaysia offers a different level of flexibility when it comes to reducing your principal and saving on interest.

Term Loan

Has a fixed repayment schedule and consistent monthly instalments. Extra payments are often treated as advance instalments unless you formally request them to reduce the principal.

Low – Extra funds do not lower interest automatically.

Semi-Flexi Loan

Allows you to make extra payments that reduce your principal. Some banks may charge a small processing fee or require written notice before you withdraw the extra funds.

Moderate – Reduces interest, but partial flexibility for withdrawals.

Full-Flexi Loan

Linked to a current account where any extra money you deposit automatically offsets your loan balance. You can withdraw the funds anytime without complex procedures.

High – Provides the most flexibility and highest potential interest savings.

Understanding how your loan works is crucial. If your loan is term-based, advance payments may not offer real savings unless your bank allows them to reduce the principal. But if you have a semi-flexi or full-flexi loan, every extra ringgit you pay can work directly in your favour by lowering your balance and saving more on interest.

When Does Each Strategy Make Sense?

Every homeowner’s financial situation is different, and the best choice depends on your loan type, income stability, and future plans.

Understanding when to make advance payments versus when to reduce your principal can help you manage both flexibility and savings effectively.

When Advance Payments Make Sense

An advance payment works best if your priority is short-term convenience rather than long-term savings.

Consider this option if:

- You expect temporary income changes, such as maternity leave, job transition, or contract work.

- You want to stay ahead of your instalments for peace of mind.

- Your loan is a term loan, and your bank doesn’t allow direct principal reductions.

- You prefer having quick access to funds later without changing your loan structure.

Example:

You receive a small year-end bonus and want to cover the next two months of instalments in advance. This keeps your repayment on track while freeing up cash for short-term expenses.

You receive a small year-end bonus and want to cover the next two months of instalments in advance. This keeps your repayment on track while freeing up cash for short-term expenses.

When Reducing Your Principal Works Better

If your goal is to save on interest and shorten your loan tenure, applying extra funds directly to your principal is the more effective choice.

Choose this approach if:

- You have a semi-flexi or full-flexi loan that automatically applies extra payments toward principal.

- You have a stable income and want to become debt-free sooner.

- You’re comfortable locking in extra funds for long-term benefit.

- You want to maximise your savings over the life of your loan.

Example:

You receive a RM30,000 performance bonus. Instead of spending it or prepaying instalments, you apply it toward your principal. Your loan balance drops immediately, reducing the total interest you pay and helping you finish your loan a few years earlier.

You receive a RM30,000 performance bonus. Instead of spending it or prepaying instalments, you apply it toward your principal. Your loan balance drops immediately, reducing the total interest you pay and helping you finish your loan a few years earlier.

If you’re managing short-term cash flow or have a fixed-term loan, advance payments may be a practical choice. But if you want real, long-term savings, reducing your principal is far more rewarding.

The right approach depends on your priorities, whether you value flexibility today or lower debt tomorrow.

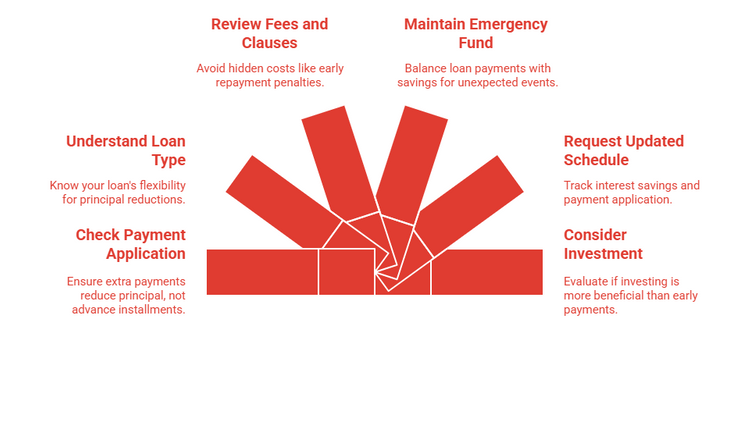

Things to Check with Your Bank Before You Commit

Before you make any advance payments or lump-sum principal reductions, take a few minutes to check how your bank will treat those extra funds. Each financial institution in Malaysia has its own policies, and understanding them upfront ensures your money works exactly the way you intend.

Here’s a quick checklist to guide you.

1. How Will the Extra Payment Be Applied?

Ask your bank whether your additional payment will be used to:

- Pay future instalments in advance, or

- Directly reduce your loan principal.

This single question can make a big difference. If your goal is to save interest, you will want it applied to your principal, not as advance instalments.

2. Are There Any Fees or Penalties?

Some banks charge administrative or processing fees, especially for withdrawals from semi-flexi loans. Others may impose early repayment penalties during the loan’s lock-in period, typically the first three to five years.

Confirm these costs beforehand so your savings are not reduced by unexpected charges.

3. What Are the Rules for Withdrawals?

If you have a semi-flexi or full-flexi loan, check whether you can access the extra money you have paid.

- Full-flexi loans usually allow withdrawals at any time through your linked current account.

- Semi-flexi loans may require a written notice or a small processing fee for each withdrawal.

Understanding these details helps you plan your cash flow without locking in funds you might need later.

4. Is There a Lock-In Period?

Most housing loans in Malaysia have a lock-in period, during which early repayments or full settlements may trigger a penalty, usually around 2% to 5% of the outstanding balance.

If you are still within this lock in period, check whether your extra payments are allowed without penalty or whether it is better to wait until it ends.

5. Will You Receive Updated Statements or Recalculations?

After you make any extra payment, ask your bank for a revised statement or loan schedule.

This will show how much interest you are saving, how your principal has reduced, and whether your repayment period has shortened.

Keeping track helps you ensure the payment was applied correctly.

This will show how much interest you are saving, how your principal has reduced, and whether your repayment period has shortened.

Keeping track helps you ensure the payment was applied correctly.

Before transferring any extra funds, always get clarity on:

- How your payment will be applied,

- Whether fees or penalties apply, and

- What flexibility does your loan offer?

A quick call or visit to your bank today can prevent costly assumptions later and help you make the most of your extra repayments.

Common Mistakes to Avoid When Reducing Your Housing Loan Interest

Even with the best intentions, some homeowners end up saving less interest than they expected. Avoiding a few common mistakes can make a big difference in how effectively you reduce your loan balance and shorten your repayment period.

1. Assuming Extra Payments Always Reduce Your Principal

Many borrowers believe that paying extra automatically lowers their principal. However, some banks treat these payments as advance instalments instead.

Always check with your bank how your extra funds will be applied before transferring any amount.

Always check with your bank how your extra funds will be applied before transferring any amount.

2. Ignoring Loan Type Restrictions

Not every loan gives you the same flexibility. If you have a term loan, your ability to make principal reductions may be limited unless your bank allows it.

Semi-flexi and full-flexi loans offer more flexibility, but the process differs between banks. Understanding your loan type helps you plan the right repayment strategy.

3. Overlooking Fees and Lock-In Clauses

Some borrowers rush to make lump-sum payments without considering hidden costs such as withdrawal fees or early repayment penalties.

Always review your loan agreement for lock-in periods and associated charges before making any large extra payment.

Always review your loan agreement for lock-in periods and associated charges before making any large extra payment.

4. Using All Savings for Early Payments

It may be tempting to put every extra ringgit into your housing loan, but keeping an emergency fund is just as important. Life events such as medical expenses or job changes can require quick access to cash.

Make sure you have at least three to six months of living expenses saved before making a large lump-sum payment.

Make sure you have at least three to six months of living expenses saved before making a large lump-sum payment.

5. Not Requesting an Updated Loan Schedule

After making an extra payment, some borrowers forget to request a revised statement from their bank.

Without it, you cannot track exactly how much bank interest you have saved or whether the payment was applied correctly. Always confirm these updates in writing or through your online banking portal.

Without it, you cannot track exactly how much bank interest you have saved or whether the payment was applied correctly. Always confirm these updates in writing or through your online banking portal.

6. Focusing Only on Interest Savings

Reducing your housing loan interest is important, but it should fit into your wider financial goals.

If your home loan rate is relatively low, you might benefit more from investing a portion of your extra funds instead of paying everything into the loan.

Balance your long-term savings and investment plans before deciding how much to pay early.

Balance your long-term savings and investment plans before deciding how much to pay early.

Key Takeaways and Next Steps

Reducing your housing loan interest is not about quick fixes; it is about making smart, informed decisions that suit your financial goals.

Whether you choose to make advance payments or reduce your principal, understanding how your loan type works and how your bank applies extra funds can make a significant difference.

Whether you choose to make advance payments or reduce your principal, understanding how your loan type works and how your bank applies extra funds can make a significant difference.

For more property insights, expert tips, and financing guides, visit the PropertyGuru Malaysia Guides section.

Still looking for your next home? Explore thousands of new project launches across Malaysia on PropertyGuru and find one that fits your lifestyle and budget.

[2026]

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.