If you earn rental income in Malaysia, understanding how it is taxed is essential, not only to stay compliant but also to maximise the legally available relief and deductions.

Knowing what qualifies as taxable income, which expenses you may claim, and how recent regulatory shifts affect landlords can significantly improve your overall tax position.

This updated guide to rental income tax in Malaysia for 2026 distils the latest developments, including revised e-invoicing obligations, the expanded scope of Service Tax (SST) now applicable to leasing and rental services, and a clear breakdown of reliefs and rebates relevant to the Year of Assessment (YA) 2025.

It is designed as a concise, reliable reference to help landlords remain informed, well-prepared, and financially efficient.

What Is Rental Income Tax?

Rental income tax is the income tax charged on earnings from letting out property, whether residential or commercial. For most individual landlords who let property passively (i.e., you collect rent but do not provide hotel-type services), rental income is taxable under Section 4(d) of the Income Tax Act 1967.

Suppose your letting activity is active and resembles a business, multiple units, staff, and significant services. In that case, income may be taxed under Section 4(a) as business income, subject to different rules for deductions and allowances.

Rent out your property.

Browse the latest rental listings to see how your unit stacks up.

Deadline for LHDN e-Filing: Key Dates

Filing deadlines depend on whether you carry on a business:

- Resident individuals who do not carry on business: 30 April (the filing year following the YA).

- Resident individuals who carry on business as of 30 June.

For YA 2025 (income for 2025), standard deadlines apply in 2026; however, always confirm the exact dates on LHDN’s MyTax portal, as LHDN may adjust dates or provide filing extensions in particular years. Missing a deadline can result in penalties under the Income Tax Act.

Rental Income vs Business Income: Why It Matters?

The distinction is not academic; it determines what you may deduct, whether you can carry forward losses, and which tax form to submit.

Consider these rules of thumb:

- Rental Income (Section 4(d)): Typically passive; deductible expenses are limited to those directly related to producing rental income (assessment tax, quit rent, loan interest where income is derived, repair and maintenance, agent fees). Capital costs and start-up expenditure are not deductible. Losses are generally limited in the ways they can be used.

- Business Income (Section 4(a)): Active profit-making activities; broader deductions may be allowed, capital allowances may be claimed, and losses may be carried forward according to business tax rules.

Suppose you offer hotel-style facilities, regular cleaning, linen services, or frequent short-term lettings with active management. In that case, you should carefully review your classification or seek professional advice to ensure accuracy.

How Is Rental Income Taxed In Malaysia?

For resident individuals, net rental income is included in your chargeable income and is taxed at progressive rates, up to a maximum of 30%. Non-residents generally face a flat rate (typically 30%) on taxable income derived from Malaysia, and they are not eligible for personal reliefs and rebates. Always compute tax using the current tax schedule and confirm bracket thresholds on LHDN or a reputable tax summary resource.

It’s also sensible to maintain detailed records of rental receipts, allowable expenses, and tenancy agreements, as proper documentation helps streamline filing and supports your position in case of any tax query. Keeping abreast of policy updates can further ensure your compliance remains accurate year after year.

Deductible Expenses For Rental Income

To compute net rental income, you may deduct expenses that are wholly and exclusively incurred in earning that rental.

Typical allowable items for passive renting include:

- Assessment tax (cukai taksiran) and quit-rent (cukai tanah) are paid to local authorities.

- Interest on loans taken to finance the property, if the loan is used to earn rental income.

- Fire and burglary insurance premiums for the property.

- Agents’ commissions for rent collection and lease renewals.

- Ordinary repairs and maintenance to keep the property in a lettable condition.

Non-deductible (capital or initial) expenses include: advertising and marketing for the first letting, legal fees and stamp duty for the initial lease agreement, and agent commission for the first letting; these are regarded as capital or preliminary expenses. Record every receipt; LHDN may request supporting documents if your return is selected for review.

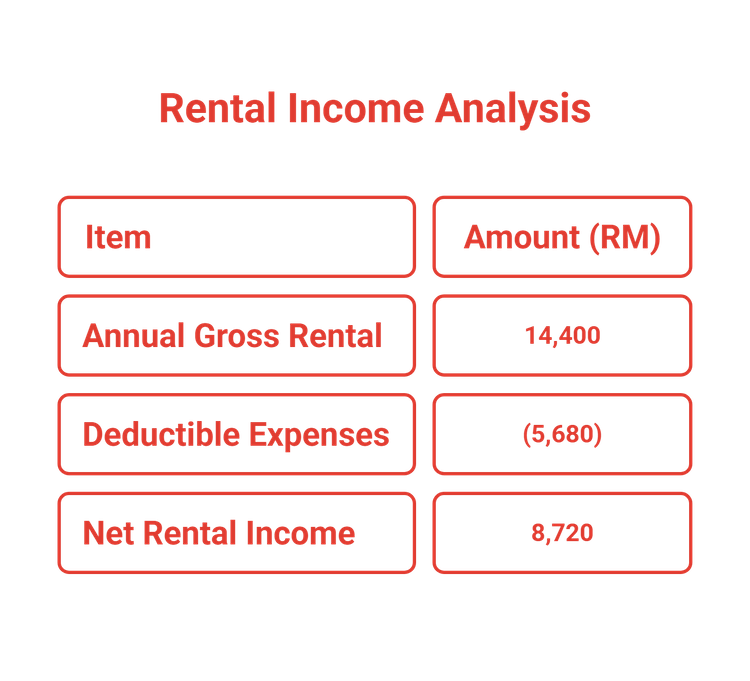

How To Calculate Net Rental Income: Worked Example

Example: You rent a unit for RM1,200 per month for 12 months. Your allowable expenses for the year are: assessment tax RM600, quit-rent RM80, and repair and maintenance RM5,000.

- Gross rental income: RM1 200 × 12 = RM14,400

- Allowable deductions: RM600 + RM80 + RM5,000 = RM5,680

- Net rental income: RM14,400 − RM5,680 = RM8 720

For simplified understanding:

That net amount is included in your total chargeable income for YA 2025 (or whichever YA applies) and taxed at the applicable progressive rates after accounting for personal reliefs.

Note: If you operate multiple rental properties with passive rental losses, tax practice allows offsetting losses against rental profits in the same YA, but conditions apply; losses from passive rental cannot usually be offset against other income types or carried forward. Refer to LHDN guidance or consult a tax practitioner for advice on specific scenarios.

How To Declare Rental Income: Forms, Where To File, And Records To Keep

Before diving into the practical steps of declaring rental income, it is helpful to understand which forms are applicable, where to submit them, and what records to keep.

A little organisation goes a long way in preventing errors and ensuring a smooth filing process.

- Forms: Individuals use Form BE if they have no business income, or Form B if they carry on a business. For e-filing, rental income is typically entered as "Statutory income from rents."

- Where to File: LHDN’s MyTax e-filing portal is the standard route for online submissions. MyTax also provides filing deadlines and guidance notes. Keep originals or scanned copies of receipts, loan statements, insurance invoices, tenancy agreements, assessment tax bills, and agent commission statements for at least seven years.

- Paying Tax: After you calculate chargeable income and apply reliefs, pay the tax due; if tax has been over-deducted through Monthly Tax Deduction (MTD/PCB), you may claim a refund when you file.

By keeping accurate records and utilising the MyTax system efficiently, you can avoid unnecessary complications and ensure compliance.

Plan Your Finances With Our Home Loan Calculator

Estimate your monthly instalments and understand how financing affects your rental income

Digital Record-Keeping for Landlords: Tools and Best Practices

Keeping accurate, well-organised records isn’t just good housekeeping; it’s essential for proving your deductions and ensuring smooth e-filing with LHDN.

While manual filing works, digital record-keeping tools can make compliance easier, faster, and more transparent.

Recommended tools and methods:

- Cloud-Based Spreadsheets: Use Google Sheets or Excel Online to record rental receipts, expenses, and loan interest. This ensures access anywhere and easy updates.

- Accounting Apps: Platforms like QuickBooks, Xero, or Wave allow you to tag expenses, store digital copies of invoices, and even integrate with MyInvois for e-invoicing compliance.

- Cloud Storage for Receipts: Save scanned copies of tenancy agreements, insurance policies, and repair invoices in secure cloud storage (e.g., Google Drive, Dropbox, or OneDrive).

- Digital Backups: Always keep an offline backup for critical records, especially tenancy agreements and tax correspondence.

Digital documentation also strengthens your position during LHDN reviews or audits, ensuring every deduction is traceable and compliant.

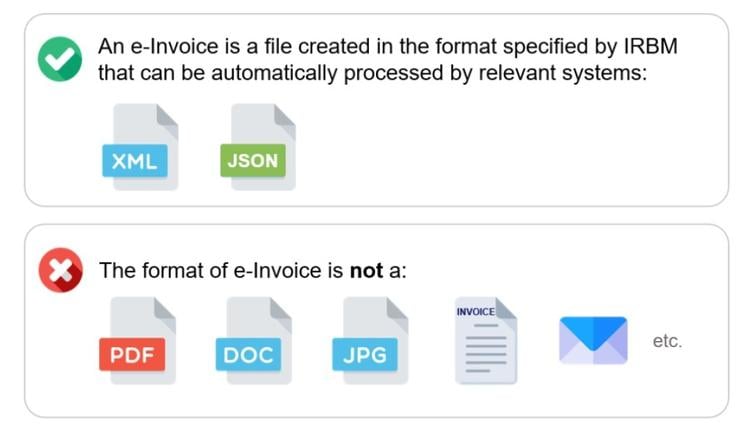

E-Invoicing Initiative (MyInvois) in Malaysia: Timeline, Process, and Benefits

Malaysia’s e-invoicing initiative, MyInvois, is a government-led programme designed to digitalise the invoicing process and enhance tax compliance across all sectors. The MyInvois portal is freely accessible to smaller taxpayers, while larger businesses can integrate their accounting systems through an API for higher transaction efficiency.

The MyInvois rollout is a phased e-invoicing implementation that spans from August 1, 2024, to July 1, 2026, structured by turnover bands and supported by six-month relaxation periods before full enforcement. Taxpayers with higher turnovers are required to comply earlier, while smaller entities are gradually brought into the system as follows:

- Above RM100 million turnover: 1 August 2024 (enforcement from 1 February 2025)

- RM25 million to RM100 million: 1 January 2025 (enforcement from 1 July 2025)

- RM5 million to RM25 million: 1 July 2025 (relaxation until 31 December 2025)

- RM1 million to RM5 million: 1 January 2026 (relaxation until 30 June 2026)

- Up to RM1 million: 1 July 2026 (relaxation until 31 December 2026)

Businesses with an annual turnover below RM500,000 are currently exempt; however, they may be required to comply in the future if their turnover exceeds the prescribed threshold.

The MyInvois system enables the issuance of validated invoices and near real-time reporting to the Inland Revenue Board of Malaysia (LHDN). Each e-invoice is assigned a unique identifier, ensuring authenticity and minimising administrative errors. This initiative marks a significant step toward greater transparency, efficiency, and alignment with Malaysia’s evolving digital tax landscape.

Why e-invoices matter for landlords?

Suppose you operate a business that issues invoices for rental or leasing services. In that case, you will likely need to comply with e-invoicing requirements under MyInvois or establish tenant self-billing arrangements, depending on your business structure.

When a tenant is a registered business, it may issue the e-invoice on your behalf under the self-billing provisions. Regardless of the arrangement, maintaining accurate records and documentation remains essential for compliance.

Important Note: LHDN continues to refine and update the MyInvois implementation timeline, enforcement phases, and technical documentation. Taxpayers are strongly advised to refer regularly to the official MyInvois portal and LHDN publications to stay informed before adopting or upgrading their invoicing systems.

Service Tax (SST) And Rental/Leasing Services: What Changed From 1 July 2025?

The Government expanded the scope of Service Tax to include particular rental and leasing services under Group K of the Service Tax Regulations. While the policy and regulations were set to take effect on 1 July 2025, the Royal Malaysian Customs Department issued guidance and temporary exemptions relating to registration and penalties, giving taxpayers time to register and adapt.

The Service Tax guide and policy documents explain which types of leasing and rental services are subject to tax, registration thresholds, and transitional reliefs. These documents help taxpayers understand their obligations clearly, ensuring proper registration and compliance as the framework takes effect.

Practical implications for landlords and property managers:

- If your leasing or rental activities constitute taxable services under the new rules, you may need to register for Service Tax and charge it to your tenants. Consult the Customs guide to determine whether your property type and turnover meet the criteria.

- The Government signalled certain transitional exemptions (for example, limited enforcement of penalties for late registration until year-end) to ease compliance, but this is time-sensitive; confirm the effective dates and any exemptions on the Customs website.

For landlords and investors navigating these regulatory shifts, staying informed is key to maintaining compliance and profitability.

Practical Tax Planning For Landlords: Mistakes To Avoid

Before diving into the details, it’s worth noting that effective tax planning begins with awareness. Many landlords unintentionally invite penalties simply by overlooking minor compliance requirements or misinterpreting what qualifies as deductible.

Keeping these essentials in mind can help safeguard your rental income and reduce unnecessary stress during tax season:

- Not Declaring Rental Income: Understatement or omission can trigger penalties under Section 113 of the Income Tax Act. Always declare all rental receipts.

- Claiming Capital Expenditure As Deductible: Major renovations and acquisition costs are capital in nature and not allowable as revenue deductions; claim only ordinary repairs.

- Weak Record-Keeping: Keep tenancy agreements, receipts for repairs, mortgage interest statements, assessment tax invoices, and agent commission slips for at least seven years.

- Confusing Passive Renting With Business Activity: Active services may convert your tax treatment from passive rental to business income, with altered deductions, obligations, and possibly GST/SST or other compliance requirements.

- Missing e-Invoicing or SST Obligations: If you operate at scale, you may need to issue e-invoices or register for SST on rental services. Check the LHDN and Customs guides early to avoid retroactive penalties.

Avoiding these common pitfalls can make a significant difference to your long-term returns and peace of mind.

Tax Reliefs For YA 2025, Complete List And Notes

Tax reliefs reduce your chargeable income. The following list reflects the YA 2025 reliefs as published by LHDN and cross-checked against reputable commentary and local tax guides.

Personal Reliefs (Selected Items):

- Individual and Dependent Relatives: RM9,000.

- Medical Treatment, Special Needs, and Carer Expenses for Parents and Grandparents: Up to RM8,000 (medical certification required).

- Purchase of Basic Supporting Equipment for Disabled Family Members: RM6,000 (restricted).

- Disabled Individual (Self): RM7,000.

- Education Fees (Self): Up to RM7,000 (restrictions apply; upskilling components often limited to RM2,000).

- Medical Expenses For Serious Disease, Fertility Treatment, Vaccination: Combined reliefs up to RM10,000 in specific categories.

- Complete Medical Examination, Covid-19 Detection Test, Mental Health Consultation: Up to RM1,000 (subset relief).

- Expenses For Early Intervention Or Intellectual Disability Assessment For Child: Up to RM4,000.

- Lifestyle Relief (Books, Computer, Smartphone, Sports Equipment, Internet): RM2,500.

- Breastfeeding Equipment (Child ≤2, once every two YAs): RM1,000.

- Childcare Fees (Registered Centre, Child ≤6): RM3,000, with the relief now extended until YA 2027.

- Net Deposit In SSPN (National Education Savings): RM8,000.

- Husband/Wife/Alimony To Former Wife: RM4,000.

- Disabled Spouse: RM6,000.

- Child Reliefs: RM2,000 for each unmarried child ≤18; higher reliefs apply for children in higher education, with specific RM8,000 allowances for some instances.

- Life Insurance, EPF, and Pension Contributions: Combined limits apply, typically RM7,000 across items.

- Deferred Annuity and Private Retirement Scheme (PRS): RM3,000 (relief extended until YA 2030).

- SOCSO Contribution: RM350.

- Expenses for EV Charging Facilities (Non-Business Use): Up to RM2,500 for installation or subscription costs; relief extended through YA 2027, and now includes food-waste composting machines under the same cap.

If you are filing for YA 2025, ensure receipts and documentation adequately support each relief; LHDN may ask for proof.

Note: For confirmation, always refer to LHDN’s official relief pages.

Tax Rebates For YA 2025 And Non-Resident Rules

Tax rebates reduce the tax payable after computing tax on chargeable income. For YA 2025, standard rebates included modest amounts for individual taxpayers (for example, RM400 bandings in some categories) and rebates for zakat paid, subject to limits. These rebates can make a meaningful difference to your final liability when applied correctly, particularly when combined with allowable deductions and reliefs.

Non-residents do not qualify for personal reliefs or most rebates and are generally taxed at flat rates (commonly 30%). Always confirm rebate eligibility on the LHDN website before submitting your claim, and retain any supporting documentation in case verification or audit is required later.

Tax Rules for Non-Resident Landlords in Malaysia

If you’re a foreign property owner earning rental income from Malaysia, you’re still subject to Malaysian tax laws, though the treatment differs from that of residents.

Key points to note:

- Flat Tax Rate: Non-resident individuals are typically taxed at a flat rate of 30% on Malaysian-sourced income, including rental earnings.

- No Personal Reliefs: Unlike residents, non-residents cannot claim YA 2025 personal reliefs or rebates such as medical expenses, lifestyle deductions, or child relief.

- Tax Filing Obligations: Rental income must be declared through the MyTax portal using the relevant non-resident form (usually Form M). Keep clear records of rent receipts, tenancy agreements, and bank statements showing payments.

- Withholding or Double Taxation: If you are also a tax resident elsewhere, check whether a Double Taxation Agreement (DTA) exists between Malaysia and your country to avoid paying tax twice on the same income.

- E-Invoicing and SST: Non-resident landlords operating through a Malaysian entity or agent may still be subject to MyInvois or SST obligations, depending on the nature of the rental activity.

Staying compliant as a non-resident landlord ensures smooth property management and avoids penalties or tax complications during the repatriation of funds.

Joint Assessment Vs Separate Assessment: Which To Choose?

For married couples, choosing a joint assessment or a separate assessment can affect the overall tax payable:

- Separate Assessment: Use when both spouses are relatively high earners; the progressive rates are applied to each earner separately, which can sometimes result in a lower combined tax.

- Joint Assessment: Can benefit couples where one partner has substantially lower income; some reliefs may only be claimed once under joint assessment, however, so run the numbers.

The general advice is to compute both ways before filing, or seek guidance from a tax professional, to ensure you choose the option that minimises tax legally.

What Landlords Should Do Today?

Before diving into the details, here’s a clear and practical roadmap for landlords to stay compliant, organised, and financially efficient under Malaysia’s evolving tax framework.

Treat these steps as a working checklist to help you safeguard returns and avoid unnecessary penalties:

- Confirm Your Letting Status: Passive landlord or commercial letting business? If unclear, consult a tax adviser.

- Collect And Keep Records: Tenancy agreements, receipts for assessment tax, quit-rent, loan interest, insurance, repairs, and agent commissions. Retain for at least seven years.

- Check e-Invoicing and SST Obligations: If you operate at scale, assess whether you must issue e-invoices via MyInvois or register for SST on rental services. Use the MyInvois portal for guidance, and refer to the Customs Service Tax Guide for information on leasing.

- Calculate Net Rental Income: Work through deductions carefully; don’t claim capital costs as revenue deductions.

- Claim All Eligible Reliefs: Work through the YA 2025 reliefs checklist and ensure you hold supporting documentation.

- File on Time via MyTax: Avoid Late Penalties. If you’re unsure which assessment method is best (joint vs. separate), calculate both scenarios to determine the most effective approach.

- If You Need Help, Seek A Professional: For multiple properties, structured portfolios, or complex cases, engage a chartered tax adviser.

Implementing these steps ensures your property remains compliant and financially sound throughout your ownership journey.

Looking for more clarity on tax-smart ownership

Explore PropertyGuru Malaysia’s rental guides and landlord insights to manage your investments.

Final Words

Taxation around rental income can be straightforward for the casual landlord or intricate for owners with multiple properties, serviced accommodation, or corporate structures.

The crucial points are to classify your letting correctly, keep impeccable records, comply with e-invoicing and SST requirements where applicable, and claim the YA 2025 reliefs you are entitled to. For the latest LHDN forms, guidance, and MyInvois technical notes, visit the LHDN e-invoicing pages and MyTax portal.

If you need help tracking rental income or want quick access to helpful guides, check out the PropertyGuru Malaysia resources.

You can also browse current sales listings to compare rental yields and better understand today’s market.

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.