Buying a home is one of the biggest steps in life, but before you begin your search, it is important to ask yourself, How much loan can I get on my salary?

Your income plays a key role in deciding the size of your home loan. Still, banks also consider your credit score, existing debts, and Debt Service Ratio (DSR) to assess how much you can afford to repay each month.

With changing living costs and housing prices in 2026, knowing how banks calculate your loan eligibility will help you plan your finances better and buy your home with confidence.

| Table of Contents 1. How Banks Calculate Your Home Loan Eligibility • What Is Debt Service Ratio (DSR)? • What Is a Good DSR in Malaysia? 2. How Much Home Loan Can You Get Based on Your Salary • Home Loan Outlook in 2026 • Estimated Loan Amounts by Monthly Income 3. Understanding Loan Scenarios Based on Different Situations • Single Applicant with Existing Debts • Joint Application with a Spouse or Family Member • Self-Employed or Freelance Applicants • Young First-Time Buyers 4. What Property Can You Afford Based on Your Income 5. Factors That Affect How Much You Can Borrow • Debt Service Ratio (DSR) • Credit Score • Employment Stability • Loan Tenure and Interest Rate • Existing Financial Commitments • Property Value and Down Payment 6. Tips to Improve Your Home Loan Eligibility 7. Additional Costs to Prepare for When Buying a Home 8. Getting Ready for Your Homeownership Journey |

Discover Homes You Can Afford

Explore properties that fit perfectly within your monthly budget and financing range.

How Banks Calculate Your Home Loan Eligibility

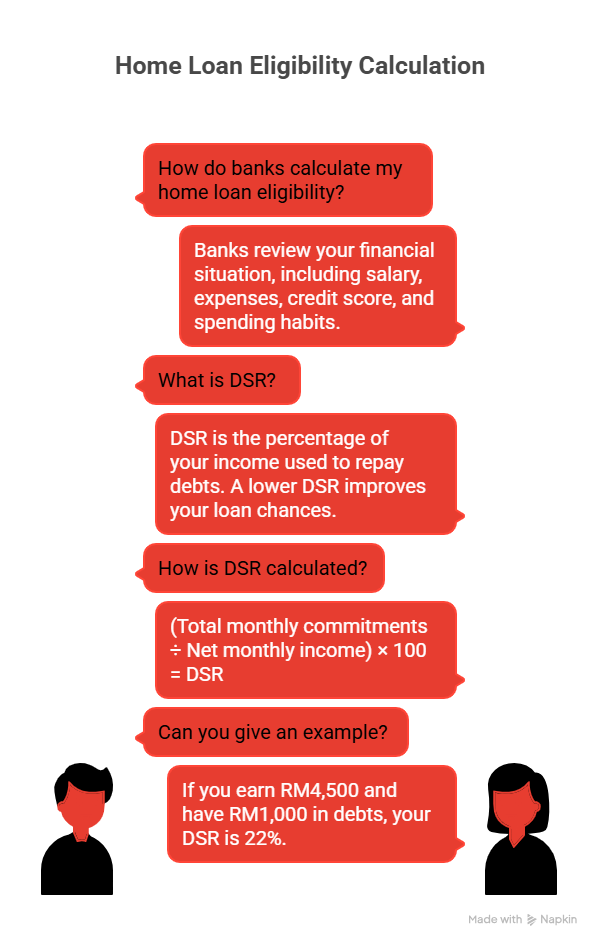

When you apply for a home loan, banks in Malaysia will review your overall financial situation before deciding how much you can borrow. Your salary is the starting point, but lenders also consider other factors, such as your monthly expenses, credit score, and spending habits.

One of the main tools banks use to measure affordability is the Debt Service Ratio (DSR).

What Is DSR?

The DSR shows the percentage of your income that goes towards repaying existing debts. This can include car loans, PTPTN repayments, and credit card bills. The lower your DSR, the better your chances of qualifying for a higher loan amount.

The formula is simple:

(Total monthly commitments ÷ Net monthly income) × 100 = DSR

Example

If you earn RM4,500 a month and have total debt commitments of RM1,000, your DSR works out like this:

(1,000 ÷ 4,500) × 100 = 22%

What Is a Good DSR in Malaysia?

Most banks prefer your DSR to stay within 30% to 40% of your net income. This level shows that you can manage new loan repayments comfortably.

However, some lenders may allow a DSR of up to 60% or 70%, especially for applicants with higher incomes or excellent credit history. It varies by bank, but as a general rule, keeping your DSR low improves your chances of approval.

How Much Home Loan Can You Get Based On Your Salary

Once you know how your Debt Service Ratio (DSR) works, the next step is to find out how much you can actually borrow. The amount depends on your income, monthly commitments, loan tenure, and the interest rate offered by the bank.

Home Loan Outlook In 2026

In 2026, most housing loans in Malaysia carry interest rates ranging from 3.8% to 4.2% per year. These rates are influenced by the Overnight Policy Rate (OPR) set by Bank Negara Malaysia. While the OPR has remained fairly stable, even a small change can affect how much you qualify to borrow.

Most banks now offer home loans with flexible tenures of up to 35 years, depending on your age and repayment ability. A longer tenure can lower your monthly instalments, making it easier to qualify for a higher loan amount, although it also means paying more interest in the long run.

Estimated Loan Amounts By Monthly Income

Here is a general guide to how much loan you can afford based on your salary. These calculations assume a 4% interest rate, a 35-year tenure, and that 30% of your income is allocated towards loan repayment.

3,000

900

250,000

4,000

1,200

330,000

5,000

1,500

415,000

7,000

2,100

615,000

10,000

3,000

880,000

These are approximate figures intended to give you an idea of what you can afford. The actual amount may vary depending on your bank’s policies, existing debts, and overall financial profile.

What These Numbers Mean For You

If your income is around RM3,000 a month, you might qualify for a loan of about RM250,000. This could be enough for a small apartment or an affordable home outside major cities. With an RM5,000 salary, a loan of around RM415,000 may help you buy a mid-range apartment or a small landed house in suburban areas.

For those earning RM10,000 or more, the loan amount could reach RM900,000, giving you the flexibility to consider condominiums or landed properties in well-connected locations.

These examples are a starting point to help you plan your home search realistically. Your exact loan amount will depend on your financial commitments, credit record, and whether you are applying alone or with a co-borrower.

Understanding Loan Scenarios Based on Different Situations

Knowing how much you can borrow is helpful, but your personal situation also plays a big role in determining your final loan amount.

Here are some common scenarios to help you understand how lenders assess different cases.

1. Single Applicant with Existing Debts

If you apply alone, your bank will focus on your monthly income, current financial commitments, and repayment capacity.

For example, let’s say you earn RM5,000 per month and already pay RM1,100 in car and credit card instalments.

If your bank allows a maximum DSR of 60%, your total repayment limit is RM3,000 (60% of RM5,000). After deducting your existing debts (RM1,100), you can afford a monthly housing repayment of RM1,900. With that, you may qualify for a home loan of around RM500,000, depending on the interest rate and tenure.

Keeping other debts low helps increase your eligible loan amount and strengthens your chances of approval.

2. Joint Application with a Spouse or Family Member

Applying for a home loan jointly can increase your borrowing power, as both incomes are taken into account.

For instance, a couple with a combined net income of RM8,000 can usually afford a higher monthly repayment, allowing them to qualify for a loan of about RM700,000 or more.

However, joint loans also mean shared responsibility. Both borrowers are equally liable for repayments, and any delay will affect both credit records. Always discuss long-term financial plans with your co-borrower before applying for a loan.

3. Self-Employed or Freelance Applicants

For self-employed individuals, banks typically require proof of stable income through financial statements, tax records, and consistent bank deposits. Since income may vary, lenders often calculate affordability using an average of the past 6 to 12 months.

If your monthly income fluctuates, try maintaining a healthy DSR by reducing business loans or credit card balances. You can also strengthen your application by providing complete documentation and maintaining a good credit score.

4. Young First-Time Buyers

If you’re early in your career and your income is still growing, it may be wise to start with a smaller property or an affordable apartment. Choosing a longer tenure, such as 35 years, can reduce monthly instalments and keep your DSR in a safer range.

Many first-time buyers also explore joint applications or government initiatives such as the My First Home Scheme or i-Miliki stamp duty exemptions to make ownership more achievable.

Every borrower’s situation is different. Understanding how banks view your financial profile, whether you apply as an individual, a joint applicant, or a self-employed buyer, helps you set realistic expectations. The stronger your financial position and documentation, the better your chances of securing a home loan that fits your salary and lifestyle.

What Property Can You Afford Based on Your Income

Once you have an idea of how much you can borrow, the next step is to understand what type of property fits within that budget. Your income plays a crucial role in determining what you can comfortably afford, but other factors, such as loan tenure, interest rate, and monthly commitments, will also influence your choices.

Here is a general guide to what different income levels can typically afford in Malaysia’s current property market. These figures assume a 35-year loan tenure with an average interest rate of around 4%.

3,000–4,000

250,000–330,000

Affordable apartments or flats in smaller towns and secondary cities such as Ipoh, Alor Setar or Seremban

5,000–6,000

400,000–500,000

Mid-range apartments or small landed homes in suburban areas like Kajang, Nilai or Johor Bahru

7,000–9,000

600,000–750,000

Condominiums or family-sized apartments in developing townships near Kuala Lumpur, Penang or Shah Alam

10,000 and above

850,000+

Larger condominiums or landed properties in mature neighbourhoods such as Petaling Jaya, Damansara or Bangsar

These estimates serve as a starting point to help you plan realistically. Prices can vary by location, property age, and size, so it’s always wise to compare listings within your preferred area.

You can use the PropertyGuru Home Loan Eligibility Calculator to match your salary and borrowing power with suitable homes in your budget range. It gives you a clearer idea of monthly repayments and helps narrow your search to properties you can truly afford.

Calculate Your Monthly Home Loan Repayments

Plan your finances with confidence and find out what fits your budget.

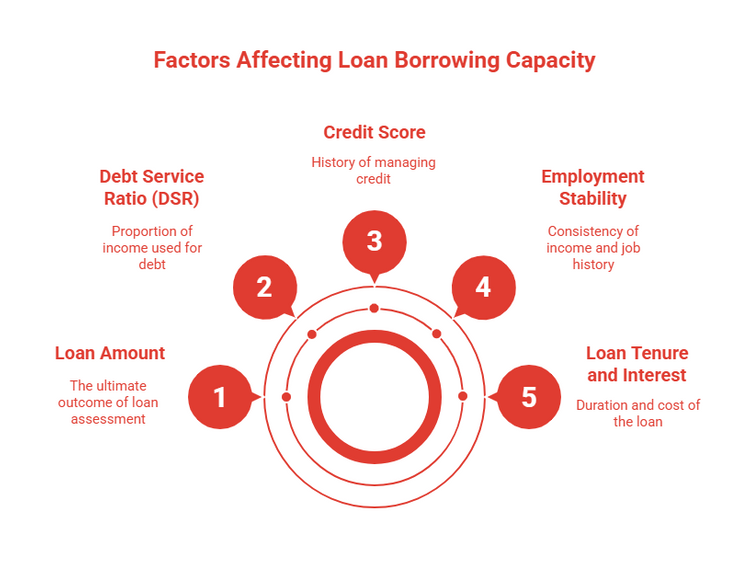

Factors That Affect How Much You Can Borrow

Your salary is an important factor in your home loan application, but it’s not the only thing banks consider. When deciding how much you can borrow, lenders will assess your overall financial health to make sure you can manage the monthly repayments comfortably.

Here are some of the main factors that can influence your home loan amount:

1. Your Debt Service Ratio (DSR)

Banks use your Debt Service Ratio to determine how much of your income goes toward paying off debts. A DSR between 30% and 60% is usually considered acceptable. The lower your DSR, the higher your chances of securing a larger loan.

If your monthly income is RM6,000 and your total debt repayments are RM2,400, your DSR would be 40%. Maintaining a DSR below 50% demonstrates to the bank that you can handle your financial commitments responsibly.

2. Your Credit Score

Your repayment history plays a big role in loan approval. Lenders check your credit report from CTOS or CCRIS to see how well you’ve managed previous loans or credit cards. A strong credit score can help you get better loan terms, while late payments or high credit utilisation may reduce the amount you qualify for.

3. Employment Type and Income Stability

Banks prefer applicants with a steady income and a stable job history. Full-time employees with regular salaries are often viewed as lower risk. Self-employed individuals or freelancers may need to provide extra documentation, such as bank statements or tax records, to prove consistent earnings.

4. Loan Tenure and Interest Rate

Your loan tenure and interest rate also affect how much you can borrow. A longer tenure can lower monthly instalments, allowing you to qualify for a higher amount. However, this also means you will pay more interest over time.

On the other hand, a shorter tenure results in higher monthly repayments but less total interest.

5. Existing Financial Commitments

Car loans, student loans, or credit card balances can reduce your available income for home loan repayments. Paying off smaller debts before applying for a housing loan can help you qualify for a higher amount.

6. Property Value and Down Payment

Banks typically finance up to 90% of a property’s price for first-time buyers. You’ll need to cover the remaining 10% as a down payment. A higher down payment reduces your loan amount and monthly instalments, making your application stronger.

Before applying for a home loan, take time to review your financial situation. Paying off debts, improving your credit score, and preparing a sufficient down payment can increase your chances of approval and help you secure a loan that fits your income level.

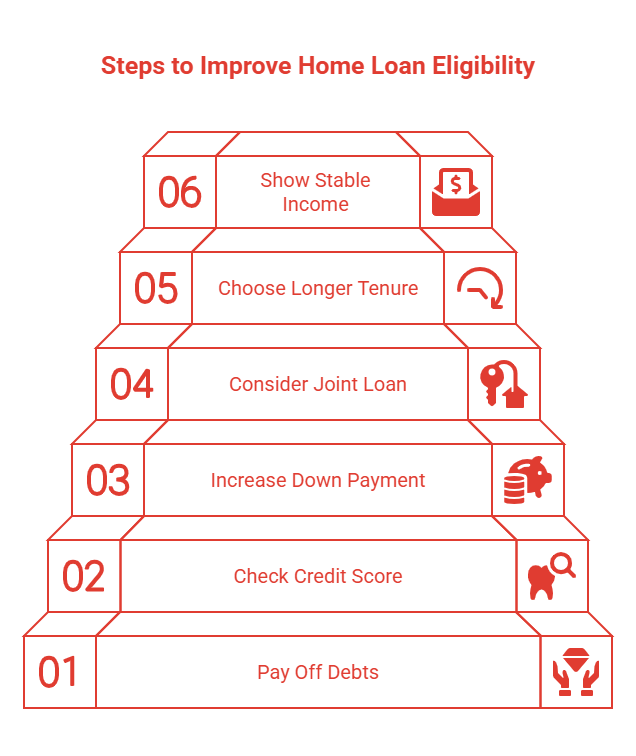

Tips to Improve Your Home Loan Eligibility

If you’ve calculated your estimated loan amount and realised it’s lower than expected, don’t worry. There are practical steps you can take to strengthen your profile and improve your chances of getting approved for a higher home loan.

1. Pay Off Existing Debts

Clearing smaller loans or reducing credit card balances can instantly improve your Debt Service Ratio (DSR). The less debt you carry, the more income you have available for new loan repayments, which increases your borrowing capacity.

2. Check and Improve Your Credit Score

Before applying for a home loan, review your credit report through CTOS or CCRIS to ensure accuracy. Ensure all payments are up to date and settle any overdue accounts. A good credit score shows banks that you manage money responsibly and can be trusted with a larger loan amount.

3. Increase Your Down Payment

If you can save up for a higher down payment, you’ll need to borrow less from the bank. This not only improves your approval odds but can also help you secure a better home loan interest rate.

4. Consider a Joint Loan

If you’re applying alone and your income limits your borrowing power, consider applying jointly with a spouse or family member to increase your borrowing capacity. Combining incomes can raise your total eligibility, allowing you to afford a higher-priced property.

5. Choose a Longer Loan Tenure

Opting for a longer repayment period can make your monthly instalments more manageable, which helps keep your DSR within an acceptable range. However, keep in mind that you’ll pay more interest overall, so it’s best to strike a balance between affordability and cost.

6. Show Stable Income and Employment

Banks prefer applicants with a steady income and continuous job history. Avoid switching jobs just before applying for a loan, and maintain consistent earnings for at least six months to one year. For self-employed applicants, keeping accurate financial records and tax filings helps build trust with lenders.

Find Out Loan Eligibility Check

Curious about your budget? Use our Eligibility Calculator to see how much home you can comfortably buy.

Additional Costs to Prepare for When Buying a Home

Getting a home loan is just one part of the journey to homeownership. Before you sign the papers, it’s important to plan for the extra costs that come with buying a property in Malaysia. These additional expenses can influence your overall budget and affect how much you can comfortably borrow.

Here are some of the key costs to consider:

- Down Payment: Most banks require a minimum of 10% of the property price. Paying a higher amount upfront can reduce your monthly instalments and total interest.

- Legal Fees: These cover your Sale and Purchase Agreement (SPA) and home loan documentation. The exact cost depends on your property price, but it usually falls between 1% and 1.5%.

- Stamp Duty: As of 2026, first-time homebuyers can still enjoy full or partial stamp duty exemptions under the i-Miliki initiative. The exemption applies to residential properties priced up to RM1 million, with specific conditions set by the Government.

- Valuation Fees: If you’re buying a sub-sale property, you’ll need to pay a valuation fee, typically ranging from 0.25% to 0.4% of the property’s value.

- Mortgage Insurance: Many banks require Mortgage Reducing Term Assurance (MRTA) or Mortgage Level Term Assurance (MLTA) to protect both you and the lender in case of unforeseen events.

- Renovation and Maintenance Costs: Once you move in, set aside a budget for home improvements, furnishing, and monthly maintenance fees, especially if you’re purchasing a condominium or serviced apartment.

Before you start viewing properties, it’s wise to calculate these costs alongside your home loan repayments. Getting pre-approved for a loan helps you understand your total financial commitment and ensures your home purchase stays within your comfort zone.

Getting Ready for Your Homeownership Journey

Planning to buy your first home soon? Before you start browsing listings, take time to find out how much home loan you can get on your salary. Knowing your Debt Service Ratio (DSR), improving your credit score, and preparing enough savings for a down payment can help you secure a better loan and make your buying experience smoother.

Use the PropertyGuru Home Loan Eligibility Calculator to estimate your borrowing power and monthly repayments. This helps you stay within budget and make confident decisions before applying for a loan.

For more tips on home financing, costs, and property buying guides, visit the PropertyGuru Malaysia Guides section.

Ready to begin your search? Explore PropertyGuru Malaysia to find new launches and resale homes that match your budget and lifestyle.

Keep Track of New Launches

Visit our new launches page to find the new launch project of your dreams and submit an enquiry today.

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.