Managing several loans at once can be exhausting. Many of us feel the pressure when credit card bills, personal financing, and hire purchase payments stack up each month. If your budget feels tight or you are planning to buy a home soon, loan consolidation Malaysia may offer some relief.

More people are exploring this option as interest rates shift and banks apply stricter Debt Service Ratio checks. Consolidation can help you organise your repayments, improve cash flow, and avoid missed payments.

This guide breaks down how it works, when it helps, and what to watch out for. By the end, you will know whether combining your debts into one repayment fits your financial goals.

See Your Potential Monthly Payment

Get quick mortgage insights and make budgeting easy.

What Is Loan Consolidation?

Loan consolidation means combining several debts into one new loan. Many Malaysians use it when they feel overwhelmed by different instalments each month. Instead of keeping track of credit cards, personal financing, and hire purchase payments, you make a single monthly repayment to one bank.

In Malaysia, consolidation can take a few forms. Some people use a personal loan to settle their outstanding balances. Others choose to refinance their property and use part of the approved amount to clear higher-interest debts.

Borrowers who prefer Shariah-compliant financing can choose a loan based on the Tawarruq concept, which follows Islamic financing principles.

The purpose is simple. You replace multiple commitments with one structured repayment that is easier to manage. This can make budgeting clearer and help reduce the chances of missing a payment.

How Loan Consolidation Works In Malaysia?

Many Malaysians turn to loan consolidation when their monthly payments become unmanageable. High credit card interest rates, rising living costs, and stricter bank checks often leave borrowers seeking a way to catch their breath. Consolidation gives you a chance to organise your debts and avoid the stress of juggling several instalments at once.

Loan consolidation in Malaysia generally works in three ways:

1. Personal loan consolidation.

You apply for a personal loan. The bank uses the approved amount to settle your credit cards, hire purchase, or other personal financing. You then repay one fixed instalment each month. This option is straightforward and does not involve property.

2. Property refinancing with cash-out.

Homeowners can refinance their property if it has built up equity. The bank values the property, offers a new loan amount, and the extra funds can be used to clear higher-interest debts. This method may offer lower rates, but it also requires your property to be used as collateral.

3. Shariah-compliant consolidation.

Borrowers who prefer Islamic financing can apply for a Tawarruq-based loan. It follows Islamic principles but achieves the same outcome: settling multiple debts and replacing them with a single structured repayment.

Regardless of the method, banks will assess:

- Your income and employment stability

- Your credit report from CTOS and CCRIS

- Your Debt Service Ratio

- Your repayment history and current commitments

If approved, the bank pays off the listed debts. You then begin paying one instalment under the new loan. The goal is more precise budgeting, fewer due dates, and a repayment amount that aligns with your monthly cash flow.

Why More Malaysians Are Considering Loan Consolidation in 2026?

Many Malaysians feel the pressure of rising living costs, higher interest charges, and tighter bank requirements. When several instalments fall on the same week, it becomes challenging to manage cash flow.

Loan consolidation can help because it consolidates your debts into a single, structured loan with a lower interest rate. The aim is not to erase your debt, but to make it easier to handle each month.

Here is why many people consider it:

- Fewer monthly payments: Instead of tracking several due dates, you only manage one. This reduces the chance of late payments.

- Lower overall instalment: Consolidation can reduce the amount you pay each month. This frees up cash for daily expenses, savings, or home planning.

- More predictable budgeting: One fixed instalment makes it easier to plan your spending. You know exactly how much you need to set aside every month.

- Potential interest savings: Credit cards and some personal loans have high annual rates. Consolidation may give you a lower rate, depending on the loan type and your profile.

- Better Debt Service Ratio: A cleaner repayment structure can improve your DSR. This matters if you plan to apply for a home loan or refinance your existing mortgage.

- Less financial stress: Many people choose consolidation simply because they want a calmer, more manageable financial routine. Reducing mental load is just as important as cutting costs.

Consolidation is not a quick fix. It is a practical step for borrowers who want more precise control over their monthly commitments and long-term financial goals.

Risks and What You Should Consider Before Consolidating?

Loan consolidation can make your finances easier to manage, but it also comes with risks. It is important to understand these points before you apply. This helps you avoid surprises and choose a repayment plan that fits your long-term goals.

The main risks to consider include:

- You may pay more interest over time: Consolidation often gives you a lower monthly instalment, but this can happen because the loan tenure is longer. A longer tenure may result in a higher total amount paid, even if the rate is lower.

- There may be extra fees: Some banks charge processing fees, legal fees, stamp duty, or early settlement fees. The final cost depends on the loan type and the amount you consolidate. Always check the complete list of charges before accepting an offer.

- Your credit score may temporarily drop: A new loan application will appear on your CTOS and CCRIS reports. This is normal, but it may temporarily impact your score.

- Your property may be used as collateral: If you consolidate through refinancing, your home becomes part of the loan structure. This carries more risk than an unsecured personal loan because missed payments can affect your property.

- You may fall back into old spending habits: Consolidation frees up cash, but if you continue using credit cards heavily, you may end up in deeper debt than before. Discipline is essential.

- Not all banks accept every type of debt. Some lenders do not consolidate certain types of financing, such as overdue accounts or debts with pending legal action. Always check what the bank is willing to cover.

- The offer depends on your profile: Your rate, tenure, and loan approval depend on your income, credit history, and Debt Service Ratio. Some borrowers may not get a rate that provides meaningful savings.

Before consolidating, review your debts, consider your long-term financial plans, and compare offers from multiple banks. A clear understanding of the risks helps you make a confident and informed decision.

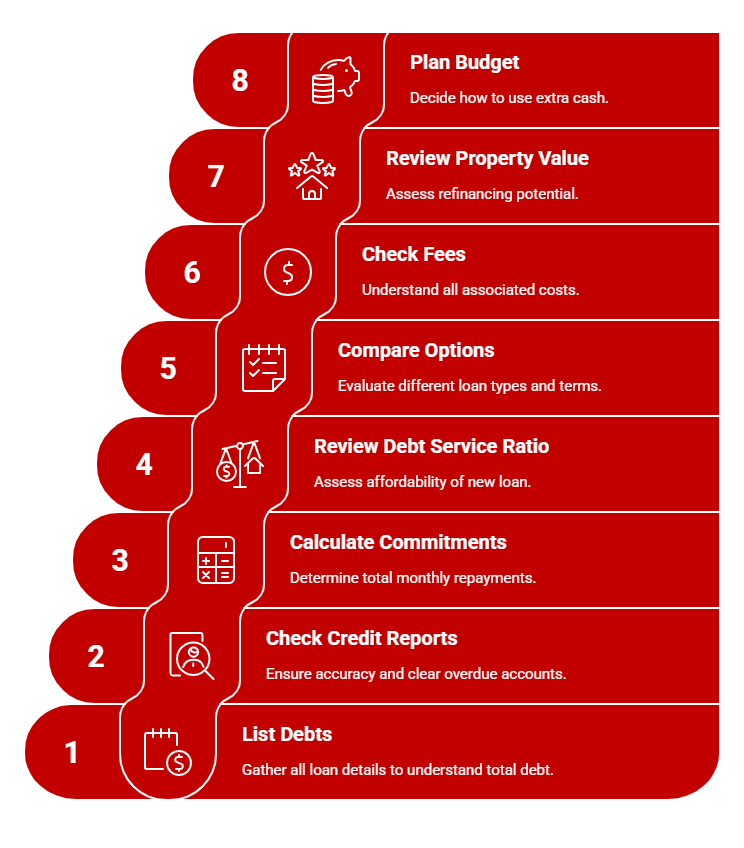

How to Prepare for Loan Consolidation in Malaysia?

Preparing early helps you understand whether consolidation is the right move. It also increases your chances of getting approved. The steps below guide you through what to check before applying.

Step 1: List All Your Existing Debts

Write down every loan you have. Include credit cards, personal financing, hire purchase, and any other commitments. Note the outstanding balance, interest or profit rate, and monthly instalment. This gives you a clear view of your total debt.

Step 2: Check Your CTOS and CCRIS Reports

Your credit report affects your chances of approval. Download your latest CTOS and CCRIS reports. Make sure the information is correct. Clear overdue accounts if you can. A healthier record may help you get a better rate.

Step 3: Calculate Your Total Monthly Commitments

Add up all your monthly instalments. This shows how much of your income is already tied to repayments. It also helps you compare the difference before and after consolidation.

Step 4: Review Your Debt Service Ratio

DSR is important in Malaysia. Banks use it to decide whether you can afford a new loan. A single repayment after consolidation may help you bring your DSR to a more acceptable range.

Step 5: Compare Different Consolidation Options

Consider personal loans, refinancing, and Shariah-compliant financing options. Compare interest or profit rates, tenures, and charges. The right choice depends on your income, long-term plans, and the type of debts you want to clear.

Step 6: Check All Fees and Charges

Some loans come with processing fees, legal fees, valuation fees, or stamp duty. Always look at the total cost, not just the monthly instalment. A loan with a low monthly payment may still cost more in the long run.

Step 7: Review Your Property Value if You Plan to Refinance

If you want to consolidate through refinancing, check your property’s latest valuation. The cash-out amount depends on the market value and the bank’s financing margin.

Step 8: Plan Your Budget After Consolidation

Decide how you will use the extra cash each month. Many borrowers build savings or set up an emergency fund. Avoid taking on new debts unless it is necessary.

Preparing through these steps helps you approach consolidation with confidence. It also ensures the new loan supports your long-term financial goals.

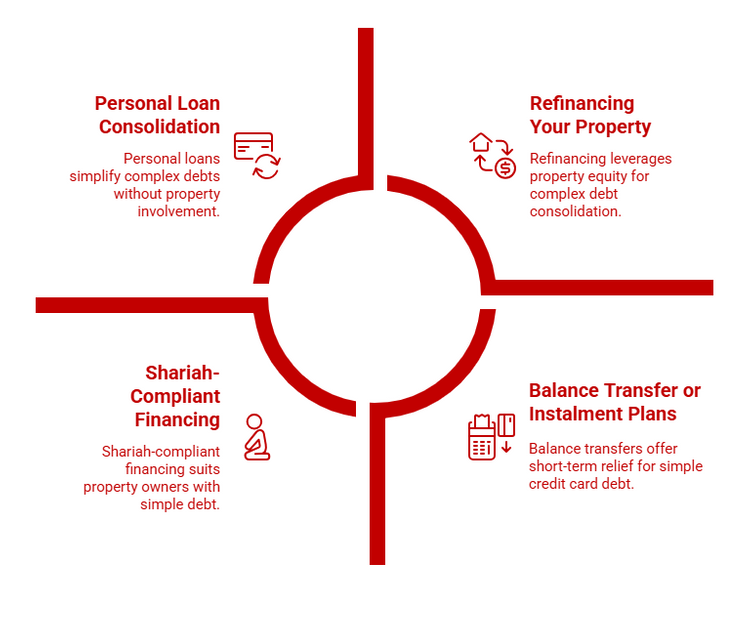

Types of Loan Consolidation Options in Malaysia

Malaysians have a few different ways to consolidate their debts. Each type of loan works differently, and the right one depends on your income, property ownership, and the type of loans you currently have.

Below are the common consolidation methods used in Malaysia.

1. Personal Loan Consolidation

This is one of the simplest options. You apply for a personal loan, and the bank uses the approved amount to settle your outstanding debts. You then repay one fixed instalment each month.

It works well if you have:

- High credit card balances

- Several small loans

- No property to refinance

Approval depends on your income, credit history, and Debt Service Ratio.

2. Refinancing Your Property

Homeowners can consolidate debts by refinancing their home loan. If your property has enough equity, the bank may approve a higher loan amount. The extra funds can be used to clear higher-interest debts.

This option is suitable if you:

- Own a property with a strong valuation

- Want a lower interest rate

- Prefer a longer tenure for easier monthly payments

Keep in mind that your property becomes collateral for the new loan, so you must manage the repayment carefully.

3. Shariah-Compliant Financing

Borrowers who prefer Islamic principles can apply for a Tawarruq-based loan. It works towards the same goal as conventional consolidation but follows Islamic financing rules.

This option is often chosen by borrowers who:

- Prefer Shariah-compliant financing

- Want a clearer repayment structure under Islamic terms

Profit rates and fees vary by bank, so it is important to compare offers.

4. Balance Transfer or Instalment Plans

Some borrowers consolidate only their credit card debt. Balance transfer plans allow you to move your credit card balance to a lower-rate plan. Some banks offer zero per cent instalment plans for a limited period.

This is helpful if you:

- Want a short-term solution

- Have only credit card debt

- Want to avoid long-term loans

This method does not consolidate all types of debt, but it can reduce your card interest significantly.

How Loan Consolidation Affects Your Debt Service Ratio (DSR)?

A high DSR makes it harder to get new financing, especially for home loans. This is why many borrowers look at consolidation when they want to improve their DSR.

Loan consolidation can affect your DSR in a few ways:

- One repayment replaces several instalments.

When you move from multiple payments to a single structured loan, your total monthly commitment may drop. A lower commitment means a healthier DSR.

- Lower interest or profit rates can reduce your monthly amount.

Credit cards and some personal loans have high rates. Replacing them with a lower-rate loan can bring your DSR to a more comfortable range.

- A longer tenure can reduce pressure on your income.

A longer tenure spreads your repayment over a longer period. This lowers your monthly instalment and improves your DSR, but it may increase the total interest you pay over time.

- Banks usually calculate DSR based on your new consolidated loan, not the old scattered debts.

When debts are combined, the bank looks at the new loan’s instalment. This is often lower than the combined payments of your existing loans.

Loan consolidation supports a healthier DSR, but the final outcome depends on your loan amount, tenure, and financial discipline.

Find Homes That Match Your Style

Stop scrolling endlessly. Set your filters once and discover homes tailored to you.

Types of Debts You Can Consolidate in Malaysia

Loan consolidation works best when you know which debts can be included. Most banks in Malaysia allow the following debts to be consolidated:

- Credit card balances: These are usually the most expensive due to high annual interest rates. Many borrowers start consolidation with their card balances.

- Personal loans or personal financing: If you have several personal loans, consolidation can merge them into one repayment with a fixed instalment.

- Hire purchase (car loans): Some banks allow you to consolidate outstanding hire purchase amounts. This is helpful if your car loan still has a large balance.

- Education loans: Certain study loans can be included, depending on your lender and your repayment history.

- Medical bills or other unsecured debts: Unsecured debts with clear documentation may be considered for relief. This depends on the bank’s policies.

Not all debts can be consolidated. The following may not qualify:

- Debts under legal action: If your account has already been handed to a lawyer or is in default, most banks will not consolidate it.

- Business loans: Business-related financing is usually handled separately and may not fall under personal consolidation plans.

- Overdue debts with no active repayment: Some banks require accounts to be active or have ongoing payments to be included.

Each bank has different criteria, so it is important to confirm what they accept. A clear list of your debts helps the bank assess your application faster and offer options that match your financial needs.

How Loan Consolidation Can Support Your Home Loan Plans?

Many Malaysians turn to consolidation when they are preparing to buy a home. Banks want to see a stable financial profile, and consolidation can help you organise your commitments before submitting a mortgage application. It does not guarantee approval, but it can place you in a stronger position.

Below are the ways consolidation can support your home loan goals.

1. Lower Monthly Commitments

When several small instalments are combined into one, your total monthly commitment may drop.

A lower amount improves your DSR and brings it closer to the bank’s acceptable range.

Why this matters:

- Banks follow strict DSR limits.

- A smaller instalment can be the difference between approval and rejection.

- A lower DSR gives you more flexibility to choose your mortgage package.

2. Clearer Repayment Structure

Banks prefer borrowers who show consistency. One fixed monthly repayment signals stability and responsible financial management.

Why banks like this:

- It is easier to evaluate one loan instead of many.

- A structured payment pattern reduces risk in the bank’s eyes.

- It reflects good planning and financial discipline.

3. Fewer Late Payments on Your Record

Managing several due dates increases the risk of missing a payment. Even one late payment can appear on your CCRIS report.

How consolidation helps:

- One repayment reduces confusion.

- It improves your repayment behaviour over the next few months.

- A cleaner payment history makes your mortgage profile stronger.

4. Better Control Over Your Credit Utilisation

High credit card usage weakens your borrowing ability. Clearing these balances through consolidation may help you rebuild your credit standing.

Why this matters:

- Credit utilisation influences your credit score.

- Lower balances show healthier financial behaviour.

- A healthier profile supports your future home loan application.

5. More Stable Cash Flow for Your Down Payment

Lower monthly instalments help you save. Buying a home involves more than just the monthly mortgage payment, and having strong cash flow gives you room to prepare.

What this allows:

- Set aside money for booking fees and a down payment.

- Plan for renovation and moving costs.

- Build an emergency buffer, which banks like to see.

6. A Smoother Refinancing Process

Some homeowners consolidate before refinancing to show a stable repayment pattern. This can improve their chances of getting a better package.

How this helps:

- A cleaner financial profile supports refinancing approval.

- It may help you negotiate a better rate.

- Banks view you as a lower risk when your commitments are well-managed.

Consolidation can support your home loan plans, but review your budget and avoid new debts. A steady repayment record will strengthen your application.

Realistic Examples: How Loan Consolidation Changes Monthly Payments

Clear examples help you see how consolidation affects your monthly budget and long-term plans. Below are two common scenarios faced by Malaysian borrowers and how consolidation changes their repayment structure.

Example 1: Consolidating Credit Cards and a Personal Loan

This is a common situation for salaried Malaysians who rely on credit cards and personal financing.

Current Financial Situation

Credit Card

RM18,000

RM900 (minimum)

Personal Loan

RM12,000

RM350

Total Monthly Commitment

—

RM1,250

This borrower pays high interest on the credit card and struggles to manage cash flow.

They want a simpler monthly structure and a more manageable instalment.

They want a simpler monthly structure and a more manageable instalment.

After Consolidation (Personal Loan)

They apply for a personal loan consolidation:

- New loan amount: RM30,000 (includes outstanding balances and small fees)

- Tenure: 5 years

- Estimated monthly instalment: RM650

Outcome is:

Total Monthly Payment

RM1,250

RM650

Number of Payments

2 lenders

1 lender

Credit Card Interest

High

Cleared

Cash Flow

Tight

Improved

What This Means:

- The borrower frees up RM600 each month.

- DSR improves because monthly commitments are lower.

- The repayment schedule becomes predictable.

- Suitable for someone preparing for a home loan.

This example shows how a personal loan can create a clear and stable repayment plan for everyday borrowers.

Example 2: Using Property Refinancing to Consolidate Several Debts

This example reflects many homeowners who have multiple loans and want to tidy up their finances before applying for a new mortgage or refinancing.

Current Financial Situation is:

Credit Card

RM25,000

RM1,250 (min 5%)

Hire Purchase

RM20,000

RM550

Personal Financing

RM15,000

RM450

Total Monthly Commitment

—

RM2,250

The borrower owns a property and wants lower monthly commitments.

Property Information

- Property value: RM500,000

- Existing home loan outstanding: RM330,000

If they refinance, the bank may offer:

- New home loan amount: RM420,000

- Cash-out amount: RM90,000 (used to clear all debts)

- Estimated new monthly instalment: RM1,750

Outcome is:

Monthly Payments

RM2,250

RM1,750

Number of Payments

3 lenders

1 lender

Credit Card Interest

High

Cleared

Cash Flow

Tight

Better

Debt Structure

Scattered

Organised

What This Means

- The borrower reduces monthly commitments by about RM500.

- DSR improves because only one instalment is considered.

- Their financial profile becomes clearer for future refinancing or home loan applications.

- Total interest may increase due to a longer tenure.

Refinancing works well when a borrower wants both cash flow relief and long-term repayment stability.

Refinance And Save More

Update your loan details to estimate new repayment options and potential savings.

Considering Loan Consolidation in Malaysia: Is It the Right Move for You?

Loan consolidation can make your finances easier to manage, especially when you have multiple repayments that feel overwhelming. However, it works best when you review the costs, compare your options, and select a plan that aligns with your long-term budget.

If your current commitments feel heavy or scattered, take a moment to check your credit report and calculate your DSR. These numbers will help you determine whether consolidation aligns with your financial goals.

Want to learn more about managing debts, home loans, and property financing in Malaysia? Explore more guides in the PropertyGuru Home Financing section.

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.