Stamp duty exemptions can make a significant difference to the upfront cost of buying or transferring property in Malaysia.

Whether you are planning your first home purchase or handling a property transfer between loved ones, knowing exactly which exemptions apply can help you avoid unnecessary costs.

In this guide, we explain the latest stamp duty exemption policies, who qualifies, how much you can save, and the key timelines you should be aware of. By understanding these exemptions early, you can budget more accurately and approach your property transaction with greater confidence.

| Table of Contents 1. Stamp Duty Exemption: Overview For Property Buyers 2. How Stamp Duty Is Calculated 3. Am I Eligible for the First-Time Homebuyer Stamp Duty Exemption 4. What Does the Exemption Actually Cover 5. How Much You Can Save as a First-Time Buyer (Example) 6. Why This Exemption Matters in 2026 7. What First-Time Buyers Should Keep in Mind 8. Stamp Duty Reliefs for Transfers Between Family Members 9. Which Family Transfers Qualify for Stamp Duty Relief 10. How the Family Transfer Stamp Duty Relief Works 11. Example: How Much a Family Transfer Can Save You 12. What Documentation Is Required for Family Property Transfers? 13. Other Stamp Duty Exemptions and Reliefs Worth Knowing 14. Make the Most of Your Stamp Duty Exemptions |

Check Your Home Budget Instantly

Get a quick estimate of your monthly payments and discover your real buying power.

Stamp Duty Exemption: Overview For Property Buyers

Stamp duty is one of the key costs that buyers and homeowners need to understand when dealing with any property transaction in Malaysia. It applies to important legal documents, and the amount you pay can influence how much cash you need upfront. Stamp duty is charged on two main documents:

- Instrument of Transfer, which officially transfers the property to your name.

- Loan Agreement, if you are taking a mortgage to finance your purchase.

Both documents must be stamped by the Inland Revenue Board of Malaysia (LHDN), and the cost depends on the property price and loan amount.

Without exemptions, these charges can add up quickly. For example, a home priced at RM500,000 can attract several thousand Ringgit in stamp duty before you even move in.

This is where stamp duty exemptions come in.

To help ease the financial burden, the Malaysian Government offers several forms of relief, especially for:

To help ease the financial burden, the Malaysian Government offers several forms of relief, especially for:

- First-time homebuyers, who enjoy the most substantial savings.

- Families transferring property between loved ones.

- Specific groups or scenarios, such as certain financing facilities or restructuring exercises.

These exemptions can reduce or completely remove the stamp duty you would normally pay.

Understanding the basics now helps you estimate your total costs more accurately, compare properties more confidently, and avoid last-minute financial surprises before signing your Sale and Purchase Agreement.

How Stamp Duty Is Calculated?

Before exploring the available exemptions, it helps to understand how stamp duty is normally calculated. Stamp duty is based on a tiered structure, which means different portions of the property price are charged at different rates.

These rates apply to the Instrument of Transfer, which officially moves the property into your name.

Here is the tiered rate structure used:

Stamp duty on the Instrument of Transfer:

- One per cent on the first RM100,000

- Two per cent on the next RM400,000

- Three per cent on the next RM500,000

- Four per cent on any amount above RM1 million

To make this clearer, imagine you buy a home priced at RM500,000. The stamp duty is calculated in layers:

- One per cent on the first RM100,000

- Two per cent on the remaining RM400,000

This comes up to RM1,000 + RM8,000, giving you a total of RM9,000 in stamp duty for the transfer alone.

Stamp Duty on Loan Agreements

If you are taking a housing loan, the Loan Agreement also attracts stamp duty. This is calculated at a flat zero point five per cent of the total loan amount.

For example:

- Property price: RM500,000

- Typical loan (90% margin): RM450,000

- Stamp duty on loan: 0.5% of RM450,000 = RM2,250

So, without any exemptions, your total stamp duty for this purchase would be:

RM9,000 (transfer) + RM2,250 (loan) = RM11,250

Stamp Duty for Foreign Buyers

From 1 January 2024, a flat four per cent stamp duty is imposed on the Instrument of Transfer for:

- Non-citizens

- Foreign-owned companies

Malaysian permanent residents are not included in this category.

Once you know what you would normally pay, it becomes easier to appreciate how much you can save under the stamp duty exemption schemes.

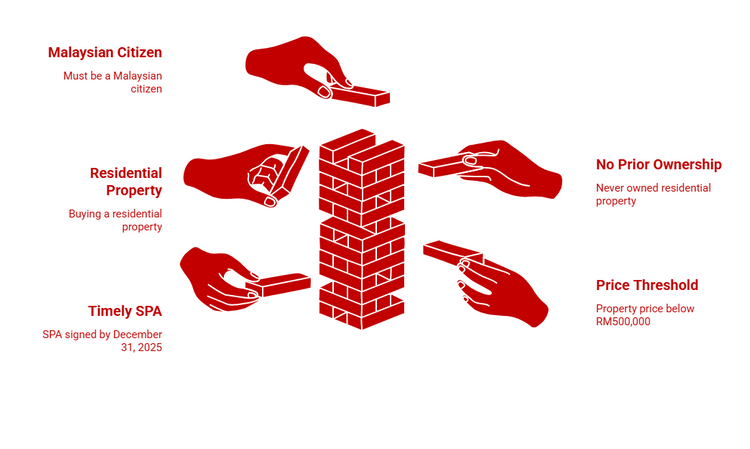

Am I Eligible for the First-Time Homebuyer Stamp Duty Exemption?

Not everyone buying a home for the first time qualifies automatically. The exemption is meant specifically for Malaysians who have never owned any residential property before. To qualify, all the following conditions must be met:

1. You must be a Malaysian citizen

Only Malaysians are eligible. Permanent residents, expatriates, and foreign buyers do not qualify for this exemption.

2. You must never have owned a residential property

This is an important condition. “Owned” is defined broadly and includes:

- A home you bought previously

- A home you inherited

- A home gifted to you through a voluntary transfer

- A jointly owned property (even partial ownership counts)

If you have had your name on any residential title before, even if you never lived there, you will not qualify.

3. The property must be a residential property

To qualify for the exemption, the home must fall under a residential category, such as:

- Terrace, semi-D, or bungalow

- Condominium

- Apartment or flat

- SOHO units with residential use (subject to state approval)

Commercial properties, shop lots, and office units do not qualify.

4. The property price must be RM500,000 or below

This is the maximum threshold for full exemption. Homes priced above RM500,000 are not eligible for the first-time buyer exemption from 2024 onwards.

5. The SPA must be signed by 31 December, 2025

Timing is crucial. Even if your loan is approved or you pay your booking fee before the deadline, you will not qualify unless the Sale and Purchase Agreement (SPA) is executed within the specified period.

What Does the Exemption Actually Cover?

Understanding what the exemption includes helps you estimate your real savings. The exemption may apply to:

1. Stamp Duty on the Instrument of Transfer (MOT)

This is the document that formally transfers the property’s ownership into your name. Without exemption, this document is charged based on the tiered stamp duty rates.

2. Stamp Duty on the Loan Agreement

Housing loans typically attract a stamp duty of zero point five per cent of the loan amount. Under certain eligibility conditions, this may also be exempted.

Combined, these exemptions reduce thousands of Ringgit from your upfront expenses.

How Much You Can Save as a First-Time Buyer (Example)

Let’s look at a realistic example to show how the exemption works in practice.

Imagine you are purchasing your first home for RM480,000:

For the Instrument of Transfer:

- One per cent on the first RM100,000 = RM1,000

- Two per cent on the next RM380,000 = RM7,600

- Total = RM8,600

For the Loan Agreement:

- Assuming a 90% loan (RM432,000)

- Zero point five per cent of RM432,000 = RM2,160

Total Stamp Duty Without Exemption = RM10,760

Stamp Duty With the First-Time Homebuyer Exemption

If you meet all the criteria:

- Instrument of Transfer = Fully exempted (RM0)

- Loan Agreement = May be exempted or significantly reduced (depending on current scheme)

This means you could instantly save RM8,600 or more, easing your upfront financial load.

Why This Exemption Matters in 2026?

The property market has evolved steadily, and upfront costs remain one of the biggest barriers for aspiring homeowners.

For many young Malaysians, the deposit, legal fees, renovation costs, and moving expenses already stretch their budgets. Stamp duty adds an additional layer of cost that can feel heavy during the initial stage of ownership.

The first-time homebuyer exemption removes some of this pressure by:

- Reducing upfront cash outflow

- Making homeownership more accessible

- Helping buyers focus on other essential costs

- Improving affordability for younger households

- Offering substantial savings during a time of rising living expenses

With the exemption running until 31 December 2025, this is an important window for eligible Malaysians to take advantage of the relief while planning their first purchase.

What First-Time Buyers Should Keep in Mind?

To ensure the exemption is applied correctly, buyers should:

- Double-check that the SPA is signed within the eligible period

- Confirm that the property price does not exceed RM500,000

- Ensure the developer or seller has provided complete documentation

- Verify with your lawyer that the correct forms are submitted to LHDN

- Keep personal records (IC, statutory declaration, proof of non-ownership)

Being prepared helps ensure a smooth stamping process and prevents delays that could impact your eligibility.

Get The PropertyGuru App

Stop scrolling endlessly. Save your search and receive personalised listings instantly.

Stamp Duty Reliefs for Transfers Between Family Members

Property transfers within a family are very common in Malaysia, whether it is a parent gifting a home to a child, a spouse transferring ownership for financial planning, or grandparents passing down property as part of their legacy. These transfers often carry sentimental value, but they also come with legal and tax implications. One of the most important parts to understand is stamp duty, which can be substantial without the right exemptions.

To make these situations more manageable, the Government provides specific stamp duty reliefs for transfers between loved ones. These reliefs help reduce the upfront cost of changing ownership, making family transfers more affordable and accessible.

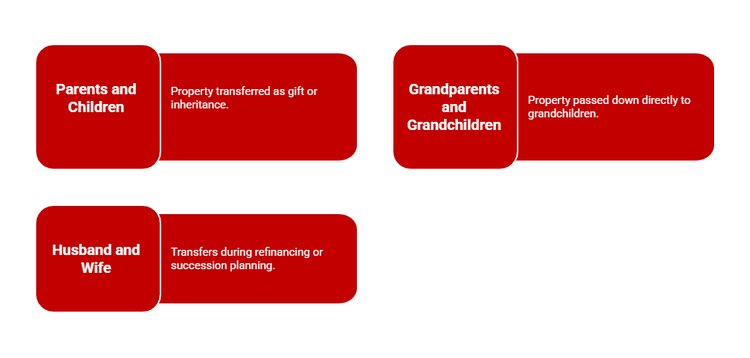

Which Family Transfers Qualify for Stamp Duty Relief?

Not all family-related transfers automatically receive exemptions. The relief is limited to direct family relationships and only applies under specific conditions. In 2026, the following types of transfers are recognised:

1. Transfers Between Parents and Children

This is the most common scenario. Property may be transferred as a gift, part of inheritance planning, or to help children start their homeownership journey.

2. Transfers Between Grandparents and Grandchildren

This applies when grandparents wish to pass down a property directly to grandchildren. It supports multigenerational planning.

3. Transfers Between Husband and Wife

Spousal transfers often arise during refinancing, succession planning, or rebalancing joint ownership.

These relationships are eligible for stamp duty relief because they involve immediate or direct family members. Transfers to siblings, cousins, or more distant relatives do not qualify under the current rules.

How the Family Transfer Stamp Duty Relief Works?

Family transfer exemptions differ from the first-time homebuyer exemption. Instead of being tied to a fixed property value threshold, relief is offered through tiered exemptions, depending on the transfer type.

Here is how the relief applies:

1. Husband–Wife Transfers

Transfers between spouses receive a full stamp duty exemption on the Instrument of Transfer.

This means no stamp duty is charged regardless of the property’s value.

This means no stamp duty is charged regardless of the property’s value.

2. Parent–Child or Grandparent–Grandchild Transfers

These transfers are eligible for:

- Full exemption on the first RM1 million of the property’s value

- Fifty per cent remission on the remaining amount above RM1 million

This relief applies to Malaysian citizens only. If the recipient is not a Malaysian citizen, normal stamp duty rates apply.

Example: How Much a Family Transfer Can Save You

Let’s look at a practical example so you can clearly see the impact of this exemption.

Scenario

A parent transfers a property valued at RM1.2 million to their child.

A parent transfers a property valued at RM1.2 million to their child.

Without Exemption

Stamp duty would be calculated as follows:

- One per cent on first RM100,000 = RM1,000

- Two per cent on next RM400,000 = RM8,000

- Three per cent on the next RM500,000 = RM15,000

- Four per cent on final RM200,000 = RM8,000

Total stamp duty without any relief = RM32,000

With Family Transfer Relief

Under the rules:

- First RM1 million = Full exemption

- Remaining RM200,000 = 50% remission

Normal rate on RM200,000 is RM8,000 (four per cent).

With 50% remission, the payable duty becomes RM4,000.

With 50% remission, the payable duty becomes RM4,000.

Total stamp duty saved = RM28,000

This is a significant reduction, especially for families planning generational transfers or balancing ownership across family members.

What Documentation Is Required for Family Property Transfers?

Because family transfers must be proven with legal certainty, the following documents are usually required:

- Identification documents (ICs) for both parties

- Proof of relationship (birth certificate, marriage certificate, or supporting documents)

- Instrument of Transfer (Form 14A)

- Valuation report or evidence of property value

- Statutory declaration confirming the relationship

- Legal documents related to inheritance, if applicable (e.g., will, Grant of Probate, Letter of Administration, or Faraid certificate)

Your solicitor will prepare and submit the necessary documents to the land office and LHDN.

Special Cases: Transfers Under Will, Faraid, or the Distribution Act

For property inherited through:

- A will

- Faraid (Islamic inheritance distribution)

- Distribution Act 1958

A fixed stamp duty fee of RM10 applies to the transfer documents. This rule helps reduce the financial burden on beneficiaries, especially when settling estate matters.

This RM10 fee applies only when a beneficiary relinquishes rights to another eligible beneficiary within the same estate process, not for general gifting.

Important Things to Keep in Mind

When planning a family transfer, it is helpful to remember:

- Relief applies only to Malaysian citizens.

- Transfers to siblings, in-laws, or distant relatives do not qualify.

- The exemption applies only to the Instrument of Transfer; other legal fees still apply.

- State land office procedures may vary slightly, so timelines differ across states.

- A valuation report may be required to determine the current market value.

- Transfers must follow the correct legal process to qualify for exemption.

Understanding these conditions early helps you prepare the right documents and ensures the transfer is processed smoothly without unexpected fees.

Other Stamp Duty Exemptions and Reliefs Worth Knowing

While first-time homebuyers and family transfers receive the most attention, they are not the only situations where Malaysians can enjoy stamp duty relief. The Government offers several other exemptions designed to support different groups, encourage economic activity, and ease the financial burden in specific scenarios.

These exemptions also serve as a useful reminder that stamp duty is not a one-size-fits-all cost. Depending on your situation, you may be entitled to partial or full relief without realising it.

1. Stamp Duty Relief for Small and Medium Enterprises (SMEs)

SMEs play a major role in Malaysia’s economy, and to support their financing activities, certain exemptions apply to loan or financing agreements issued to qualified SMEs. These exemptions are particularly helpful for small businesses purchasing commercial property or restructuring their financing.

While the specific criteria depend on the nature of the financing, eligible SMEs may receive:

- Full stamp duty exemption on specific financing instruments

- Partial exemption, depending on the financing type and value

This relief helps reduce operating costs for micro, small, and medium enterprises, especially during periods of expansion or asset acquisition.

If you are an SME owner planning to purchase or refinance commercial property, it is worth checking whether your financing qualifies for this relief.

2. Stamp Duty Relief for Corporate Restructuring

Businesses undergoing internal restructuring or intercompany transfers may be eligible for stamp duty relief under Section 15 and Section 15A of the Stamp Act 1949. These provisions are commonly used in situations such as:

- Mergers and acquisitions

- Group restructuring

- Transfers of assets between related companies

Under these sections, eligible transfers may enjoy:

- Full exemption on the Instrument of Transfer

- Reduced stamp duty for qualifying documents

Although this relief is primarily used by companies rather than individual homeowners, it is valuable for investors, family-owned companies, and high-net-worth individuals managing property holdings within corporate structures.

3. Microinsurance and Microtakaful Exemptions

To support low-income households and encourage financial protection, the Government has exempted stamp duty on microinsurance and microtakaful products for qualifying plans. These policies typically have very small premiums and are meant to support vulnerable groups.

While not directly linked to property purchases, this exemption matters for many Malaysians managing their overall financial commitments. Reducing costs on essential coverage can free up budget for homeownership planning.

4. Stamp Duty Exemption for Employment Contracts (Small-Value Instruments)

In addition to property-related documents, certain small-value instruments carry stamp duty exemptions. One example is the exemption for employment contracts valued under RM3,000, which supports lower-income workers and encourages formal job placement.

Although this exemption does not affect home purchases directly, it reflects the Government’s broader efforts to make essential legal documents more affordable. Buyers transitioning into new jobs or planning for more stable employment before purchasing a home may find this exemption beneficial.

5. Relief for Real Estate Transfers Linked to Estate Planning

As covered earlier, transfers executed under:

- Wills,

- Faraid (Islamic inheritance), or

- The Distribution Act 1958

May qualify for a fixed RM10 stamp duty, especially when one beneficiary is transferring rights to another. This ensures that inheritance processes remain financially manageable for families who are settling estates.

Make the Most of Your Stamp Duty Exemptions

Stamp duty exemptions can significantly lower your upfront property costs when buying or transferring a home in Malaysia. By understanding the eligibility rules, timelines, and the type of exemption you qualify for, you can plan your finances more accurately and avoid unnecessary expenses.

If you are preparing to buy your first home, it helps to check your financial readiness early so you know where you stand with lenders.

For more property tips and homeownership guidance, explore the PropertyGuru Guides section.

Looking for a new place? Browse the latest new launches across Malaysia on PropertyGuru.

Looking for a new place? Browse the latest new launches across Malaysia on PropertyGuru.

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.