Buying a home is a major milestone, and sometimes it makes sense to share this journey with someone else. But before you commit, there is an important question to consider: should you apply for a joint home loan?

In Malaysia, joint loans are not limited to spouses. Increasingly, parents and children, or even close friends, are choosing to apply together. Sharing a loan can make it easier to afford the home you want and can offer practical financial benefits.

However, joint loans also come with responsibilities. Both parties are legally and financially bound, so it is important to understand the implications. This guide will explore the advantages, potential drawbacks, and key considerations for taking out a joint home loan in Malaysia in 2026.

Planning to buy a home?

Understand how home loans work in Malaysia before you apply.

Why a Joint Home Loan Could Be Your Shortcut to Your Dream Home?

Applying for a joint home loan can make buying a property more achievable. By combining financial resources, you may qualify for a higher loan amount and have access to options that might be out of reach on your own.

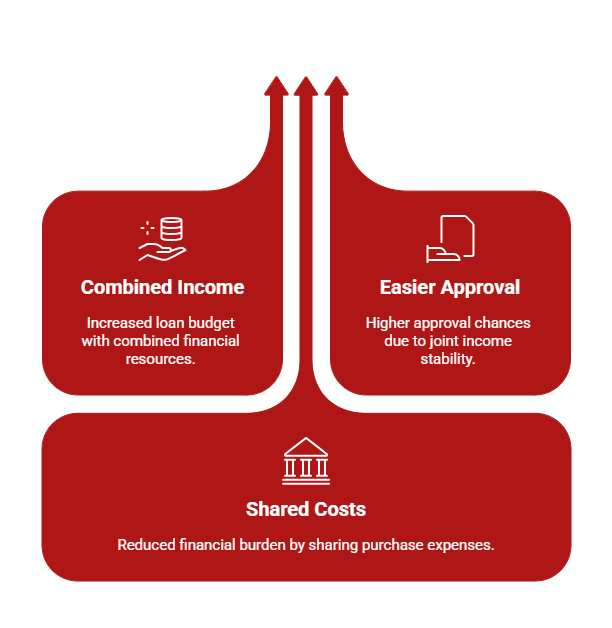

Pro 1: Combined income increases home loan budget

A joint application considers the total income of both parties. This can significantly boost your borrowing capacity, allowing you to aim for a property that better fits your needs and lifestyle.

A joint application considers the total income of both parties. This can significantly boost your borrowing capacity, allowing you to aim for a property that better fits your needs and lifestyle.

Pro 2: Easier loan approval thanks to joint income

Banks assess your combined financial profile. With two incomes, lenders may be more confident in your repayment ability, which can improve your chances of loan approval.

Banks assess your combined financial profile. With two incomes, lenders may be more confident in your repayment ability, which can improve your chances of loan approval.

Pro 3: Sharing purchase costs with a partner

Owning a home involves more than monthly repayments. By sharing the down payment, legal fees, and other costs, a joint loan can reduce the financial burden for each party.

Owning a home involves more than monthly repayments. By sharing the down payment, legal fees, and other costs, a joint loan can reduce the financial burden for each party.

Estimate your monthly repayments in seconds.

Use our home loan calculator to plan your budget wisely.

Hidden Drawbacks You Shouldn’t Ignore Before Signing a Joint Loan

While joint home loans offer clear advantages, there are important considerations to keep in mind. Understanding these potential drawbacks can help you make a more informed decision.

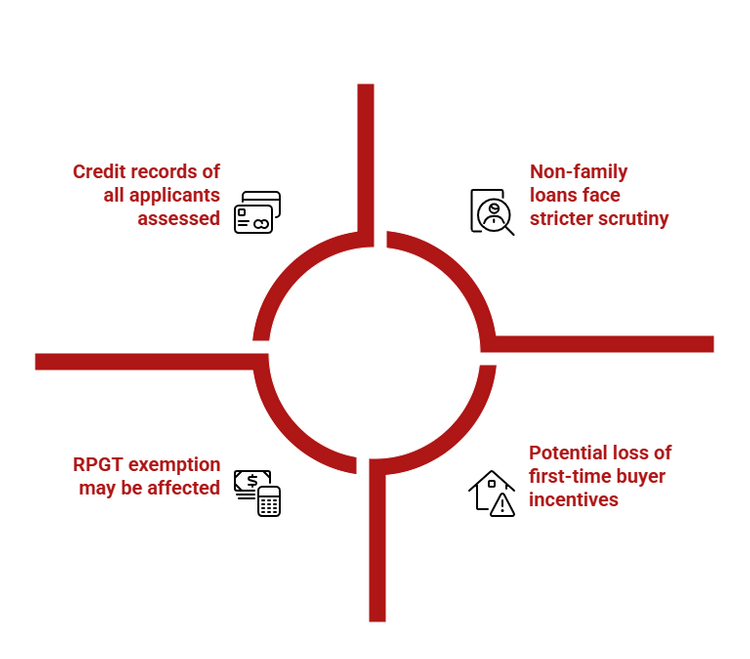

Con 1: Credit records of all applicants assessed

Lenders review the credit history of every applicant. If one party has a poor credit history, it can impact loan approval, even if the other applicant has a strong financial profile.

Lenders review the credit history of every applicant. If one party has a poor credit history, it can impact loan approval, even if the other applicant has a strong financial profile.

Con 2: Potential loss of first-time buyer incentives

Some financial incentives in Malaysia are available only to first-time homebuyers. With a joint loan, not all applicants may qualify, which could limit access to certain benefits.

Some financial incentives in Malaysia are available only to first-time homebuyers. With a joint loan, not all applicants may qualify, which could limit access to certain benefits.

Con 3: RPGT exemption may be affected

The Real Property Gains Tax exemption is offered to Malaysian citizens under specific conditions. Joint ownership may impact eligibility, meaning one party could lose out on this financial benefit.

The Real Property Gains Tax exemption is offered to Malaysian citizens under specific conditions. Joint ownership may impact eligibility, meaning one party could lose out on this financial benefit.

Con 4: Non-family loans face stricter scrutiny

Loans between friends or non-family members are usually assessed more carefully by banks. Lenders may perceive a higher risk if the parties do not share a familial relationship, which could affect approval terms.

Loans between friends or non-family members are usually assessed more carefully by banks. Lenders may perceive a higher risk if the parties do not share a familial relationship, which could affect approval terms.

Want to check your credit standing?

Here are three simple ways to get your CCRIS report.

Eligibility Criteria for a Joint Home Loan

Not everyone can apply for a joint home loan, so it is important to understand the eligibility requirements before starting the process.

- Who can apply

Joint home loans are most commonly taken out by spouses, but they can also be applied for by parents and children or even close friends. Banks typically require a strong financial relationship between the applicants to reduce risk. - Minimum income requirements

Lenders assess the combined income of all applicants to determine the loan amount they can offer. Each bank sets its own minimum income thresholds, and applicants must meet these to qualify. - Age limits and employment stability

Most banks require applicants to be at least 21 years old, with the loan term ending before a certain age, usually 60 or 70. Steady employment and a reliable income stream are also important factors in eligibility. - How banks evaluate joint applicants

Banks assess the financial profiles of all applicants, including credit history, existing debts, and repayment capacity. Each applicant’s financial health is considered individually and collectively to decide on approval and loan limits.

Use our Home Loan Eligibility Calculator to check how much you can borrow based on your income and financial details.

How Joint Loan Repayments Work?

A joint home loan means that all applicants share responsibility for repaying the loan. It is important to understand how this works to avoid potential financial complications.

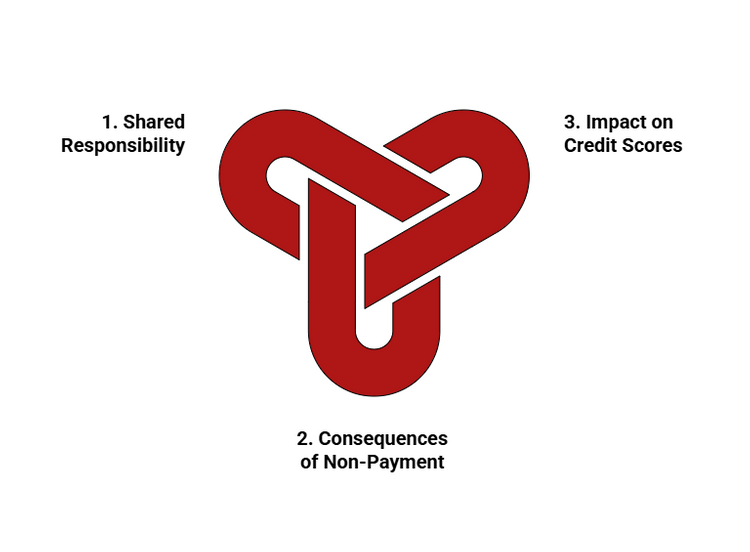

- Shared responsibility for monthly repayments

Every applicant is equally responsible for ensuring that monthly repayments are made on time. The bank considers the combined income and commitment of all applicants when approving the loan. - What happens if one party cannot pay

If one applicant is unable to contribute, the other co-applicant(s) must cover the shortfall. Failure to repay on time can lead to penalties, additional interest, and may even affect the bank’s willingness to extend future credit. - Impact on personal credit scores

Late or missed repayments by any applicant can negatively affect the credit scores of all parties. Maintaining timely payments is crucial to protect each applicant’s financial standing and future borrowing capacity.

Tax and Legal Considerations for Joint Ownership

Understanding the tax and legal implications of a joint home loan is crucial to avoid unexpected costs and complications.

- Stamp duty and legal fees for joint applicants

All joint applicants are responsible for paying stamp duty and legal fees associated with the property purchase. These costs can be shared, but it is important to budget for them in advance to prevent financial strain. - How ownership shares affect property tax and RPGT

The proportion of ownership held by each applicant can influence property taxes and eligibility for the Real Property Gains Tax exemption. Careful planning ensures that both parties maximise available benefits and comply with Malaysian tax regulations. - Importance of a legal agreement for ownership and exit strategy

A formal legal agreement outlining ownership shares, responsibilities, and procedures in case of a sale or dispute is highly recommended. This document provides clarity and protection for all parties and helps prevent potential conflicts in the future.

Before signing your tenancy agreement, know what you’re paying for.

Learn how stamp duty and admin fees work in Malaysia.

How to Apply for a Joint Home Loan?

Applying for a joint home loan requires careful planning and clear communication between all parties involved. Taking the right steps from the start can make the process smoother and reduce the risk of complications later.

1. Discuss finances and responsibilities upfront

Before applying, have a detailed discussion with your co-applicant about income contributions, repayment obligations, and ownership shares. Agreeing on these points early can prevent misunderstandings in the future.

Before applying, have a detailed discussion with your co-applicant about income contributions, repayment obligations, and ownership shares. Agreeing on these points early can prevent misunderstandings in the future.

2. Choose the right bank or financial institution

Many banks in Malaysia, including Maybank, CIMB, and Hong Leong Bank, offer joint home loans. Compare interest rates, loan terms, and eligibility criteria to find the best fit for your situation.

Many banks in Malaysia, including Maybank, CIMB, and Hong Leong Bank, offer joint home loans. Compare interest rates, loan terms, and eligibility criteria to find the best fit for your situation.

3. Prepare the necessary documents

Banks typically require documents such as:

Banks typically require documents such as:

- Sale and Purchase Agreement or Booking Form

- Passport or MyKad

- Salary slips

- Bank account statements for the past 12 months

- Income tax receipts

Having these ready can speed up the application process and improve your chances of approval.

4. Seek professional guidance if needed

If you are unsure about the process, consider consulting a qualified financial advisor or real estate professional. They can help you understand your options and guide you through the application efficiently.

If you are unsure about the process, consider consulting a qualified financial advisor or real estate professional. They can help you understand your options and guide you through the application efficiently.

What Happens If Things Don’t Go As Planned?

While joint home loans can be highly beneficial, it is important to plan for the possibility that circumstances may change. Understanding your options in advance can reduce stress and protect both parties financially.

1) Sell the House and Split the Proceeds

This is the most straightforward approach. Both parties agree to sell the property and divide the profits according to their ownership shares, allowing each person to move on with a fair share of the financial outcome.

This is the most straightforward approach. Both parties agree to sell the property and divide the profits according to their ownership shares, allowing each person to move on with a fair share of the financial outcome.

2) Buy Out Your Partner’s Share

One party can take full ownership by purchasing the other’s share. This option may require additional financing and bank approval, but it allows one person to retain the property while assuming full responsibility for the loan.

One party can take full ownership by purchasing the other’s share. This option may require additional financing and bank approval, but it allows one person to retain the property while assuming full responsibility for the loan.

3) Agree on Shared Ownership

In some cases, both parties may choose to maintain a financial stake in the property while allowing one person to reside there. This arrangement requires clear agreements and ongoing communication to manage responsibilities and any future sale of the property.

In some cases, both parties may choose to maintain a financial stake in the property while allowing one person to reside there. This arrangement requires clear agreements and ongoing communication to manage responsibilities and any future sale of the property.

Want to save more on your home loan?

Find some simple strategies to cut down your interest payments.

Tips for Choosing the Right Co-Applicant

Selecting the right co-applicant is one of the most critical decisions when applying for a joint home loan. Your choice will affect not only your chances of loan approval but also the long-term management of the property and your financial relationship.

Choosing someone you trust and who is financially responsible can make the process smoother and reduce potential conflicts in the future.

Importance of trust and financial transparency

Trust is the foundation of any joint home loan arrangement. Both parties must have confidence in each other’s ability to meet financial obligations.

- Have honest conversations about income, expenses, debts, and financial goals before applying.

- Disclose all outstanding loans, credit card debts, and other financial commitments to avoid surprises later.

- Hidden debts or undisclosed financial difficulties can create stress and strain the relationship.

- Trust also applies to property-related decisions, such as renovations or renting. Agree on how these decisions will be made.

- Maintaining clear communication and setting expectations early can prevent disagreements.

How the relationship type affects loan approval and risks

The type of relationship you have with your co-applicant can influence both loan approval and risk exposure.

- Banks are generally more comfortable approving loans for close family members, such as spouses, parents, and children, because these relationships are perceived as more stable.

- Financial institutions may view loans between friends or non-family members as higher risk due to the potential for changes in relationships over time.

- While taking a loan with a friend is possible, it requires careful planning and clear agreements to ensure a smooth process. Banks may require additional documentation or stricter eligibility criteria to mitigate the perceived risk.

- Co-owning a property with someone who is not a family member should only be considered if both parties are fully committed to maintaining the financial and legal obligations of the joint loan.

- Marriage, familial ties, and long-term partnerships often offer more stability than casual friendships or business partnerships.

- Before applying for a joint loan with a friend, assess whether the relationship is likely to remain strong throughout the mortgage term.

Things to discuss before signing a joint loan

Several crucial topics should be discussed and agreed upon before signing a joint home loan agreement. Addressing these issues in advance can prevent misunderstandings and protect both parties financially.

- Ownership shares: Decide how the property will be owned. Will it be split equally or in proportion to each applicant’s financial contribution? Clear ownership shares help define each person’s rights to the property and any proceeds in case of a sale.

- Repayment responsibilities: Agree on how the monthly repayments will be shared. Will it be based on income proportion, an equal split, or another arrangement? Understanding each applicant’s financial capacity ensures that repayments are manageable for everyone involved.

- Handling missed payments: Discuss what will happen if one party cannot make their share of the repayment. Planning for such contingencies is essential to avoid penalties, damage to your credit score, or potential disputes with the bank.

- Decision-making authority: Determine how decisions regarding the property will be made, such as those related to renovations, renting, or selling the house. Setting up a process for joint decisions prevents conflicts and ensures that both parties feel their opinions are valued.

- Exit strategy: Agree on what happens if one applicant wants to leave the loan or sell their share of the property. Options can include selling the property, buying out the other party, or maintaining shared ownership. A clear exit strategy provides security and clarity for both parties.

- Legal agreements: Consider drawing up a formal legal document that outlines all agreements between co-applicants. This may include ownership percentages, repayment obligations, exit strategies, and dispute resolution procedures. A legal agreement protects both parties and ensures that the arrangement is enforceable.

Additional practical considerations

Before finalising a co-applicant, it is also worth considering practical factors such as lifestyle compatibility and long-term financial goals.

For example, if one applicant plans to relocate frequently or has an unpredictable income, this could impact the stability of the loan repayments. Similarly, discuss any plans for future property investments or major expenditures that may affect the joint loan.

By carefully evaluating potential co-applicants and having detailed discussions on these points, you reduce the likelihood of misunderstandings and strengthen the partnership. Taking the time to choose the right co-applicant is as essential as selecting the right property or bank.

When it comes to credit health, there’s a lot to learn! Understanding CCRIS and CTOS is just the beginning. Brush up on the essentials by reading our blogs on how to improve your CCRIS and why your CCRIS and CTOS reports matter.

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.