Home renovation in Malaysia can be both exciting and nerve-racking. On one hand, giving your home a new lease of life, whether it is a modern kitchen makeover, a brighter living area, or a refreshed bathroom, can be deeply satisfying. On the other hand, renovation projects often stretch budgets, test patience, and sometimes cost far more than expected.

Still, taking on debt is a serious decision. Should you borrow to upgrade your home now, or wait until you can afford it comfortably?

This guide explains what renovation loans are, when they make sense, and how to plan your renovation wisely in Malaysia’s 2026 property market.

Exclusive Sales Listings

Find properties that match your estimated resale potential.

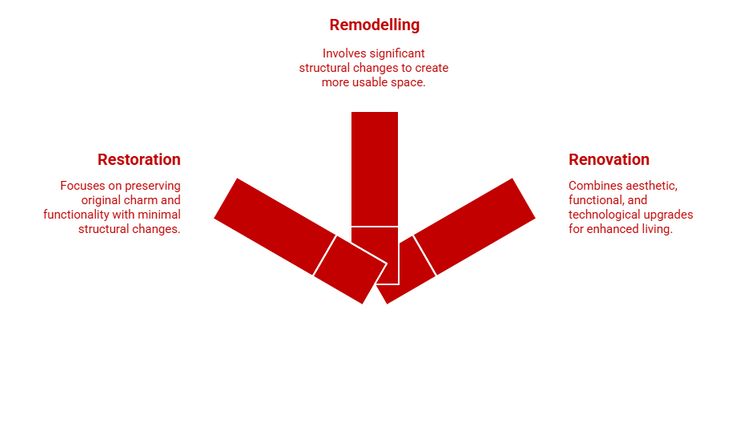

Understanding What Renovation Really Means

Before applying for a loan for renovation, it helps to understand what “renovation” truly involves. In Malaysia, the term is often used loosely to describe any form of home improvement, but not all upgrades are the same. Depending on the scale and purpose of your project, it could fall under restoration, remodelling, or renovation.

1. Restoration: Bringing Back a Home’s Original Charm

Restoration focuses on returning a property to its original condition. It is ideal for older houses that need essential repairs or replacement of worn-out parts without changing the layout.

Examples include fixing plumbing leaks, repainting walls, restoring timber flooring, or repairing roof tiles.

This approach is common among homeowners who wish to maintain the character of a heritage property or keep renovation costs low while improving functionality.

2. Remodelling: Transforming Spaces and Layouts

Remodelling goes one step further. It involves changing the structure or layout of a home to create more usable space.

Common examples include knocking down walls to form an open-plan kitchen, converting a store room into a study, or adding an extra bedroom.

These projects tend to cost more and may require professional architects, engineers, and local council approval. For many homeowners, remodelling has become popular as families grow or as remote working increases the need for multi-functional rooms.

3. Renovation: Upgrading for Comfort, Efficiency, and Style

Renovation is the broadest category and usually combines both restoration and remodelling. It covers aesthetic, functional, and technological upgrades that improve daily living. Examples include:

- Updating kitchen cabinets, flooring, and bathroom fittings

- Installing energy-efficient lighting or air-conditioning

- Adding solar panels or rainwater harvesting systems

- Introducing smart home features such as automated lighting or security systems

Renovation focuses on enhancing comfort, efficiency, and long-term property value. It is also where many homeowners consider taking a loan for renovation, as costs can range from a few thousand ringgit for cosmetic improvements to several hundred thousand for full-scale transformations.

Comparison of Home Improvement Types

To help you decide which approach best fits your renovation goals and budget, here’s a quick comparison of the main types of home improvement projects in Malaysia.

Restoration

Repairing or replacing existing features to maintain condition

Repainting, fixing leaks, and replacing tiles

5,000 – 30,000

Yes

Remodelling

Structural or layout changes for better use of space

Room extensions, open-concept kitchen, home office

30,000 – 150,000+

Yes (usually requires proof of contractor work)

Renovation

Upgrading aesthetics, functionality, or efficiency

Full interior upgrade, energy-efficient installations, smart systems

20,000 – 300,000+

Yes (covered under renovation loan or home + renovation loan)

Smart and Sustainable Renovation Trends in 2025

Renovation trends in Malaysia are evolving rapidly. Homeowners are prioritising:

- Energy efficiency: Solar panels, LED lighting, and insulation to reduce electricity bills.

- Sustainability: Eco-friendly paints, recycled materials, and water-saving fixtures.

- Smart Home living: Home automation systems, security cameras, and digital climate control.

These upgrades not only improve quality of life but can also increase a property’s market value, making them attractive reasons to explore financing options.

Whether you are restoring an old home, remodelling your current layout, or carrying out a full-scale renovation, understanding the project’s scope helps you choose the right loan for renovation and plan your budget effectively.

The Rising Cost of Renovation in Malaysia

Home renovation costs in Malaysia have continued to rise in recent years, and 2025 is no exception. Whether you are planning to update your kitchen, expand your living area, or remodel your entire home, understanding the latest price trends is essential before deciding if a loan for renovation is the right move.

Current Renovation Cost Ranges

Renovation costs vary based on property type, design complexity, and materials used. On average:

- Basic refresh: Painting, lighting, or minor fixture replacements can cost between RM10,000 and RM30,000.

- Mid-range renovation: A full kitchen or bathroom upgrade, including cabinetry and tiling, typically ranges from RM30,000 to RM70,000.

- Major structural work: Adding extensions, reconfiguring layouts, or complete home overhauls can range from RM80,000 to RM400,000 or more.

- Luxury or high-end renovation: Large landed homes or condominiums with custom finishes can easily exceed RM1 million, according to interior design firms in Kuala Lumpur.

Why Renovation Costs Are Rising?

Several factors have contributed to the steady increase in renovation expenses across Malaysia:

- Material and labour inflation: Prices of cement, steel, tiles, and fittings have risen due to global supply chain issues and higher demand for skilled labour.

- Smarter and greener upgrades: More homeowners are investing in energy-efficient air-conditioners, solar panels, and smart home systems, which cost more upfront but save on utilities in the long run.

- Design and regulatory considerations: Custom-built designs, local authority permits, and professional consultation fees add to the total bill.

- Combined project scopes: Many homeowners now combine multiple improvements, such as plumbing, wiring, and interiors, into one major renovation phase to save time, but this also increases the lump-sum cost.

How Rising Costs Affect Your Financing Decision?

With renovation budgets expanding, fewer homeowners can rely solely on savings. A loan for renovation can bridge the gap, allowing you to start your project sooner without depleting your emergency funds. However, it is important to:

- Prepare a realistic cost estimate that includes materials, labour, permits, and furnishings.

- Add a 10% to 15% contingency buffer for unexpected costs.

- Compare the total projected cost against your borrowing capacity and repayment ability before applying for a loan.

While higher costs make renovation loans more relevant, they also underline the need for careful financial planning. The key is to ensure that the borrowed amount enhances your home’s comfort or value, rather than turning into long-term debt pressure.

What Is a Loan for Renovation and How Does It Work (2026 Update)

If you are planning a major home improvement, chances are you have come across the term loan for renovation. In Malaysia, this type of financing is designed specifically to help homeowners fund upgrades, repairs, or extensions without having to dip too deeply into their savings.

Understanding how it works will help you choose the right loan and avoid unnecessary costs later.

Types of Renovation Loans in Malaysia

Most renovation loans today fall under two main categories:

1. Standalone Renovation Loans (Unsecured Personal Loans)

These are fixed-rate loans that do not require collateral. You can borrow a set amount and repay it over a fixed tenure, usually between one and ten years. Because they are unsecured, interest rates are generally higher, but the application process is faster.

2. Home-Plus-Renovation Loans (Secured Loans)

Many banks now offer combined home and renovation financing, where the renovation portion is added to your mortgage. This option allows you to borrow more at a lower interest rate, as the loan is secured against your property. However, it may involve a longer approval process and additional documentation.

Some homeowners also consider refinancing or home equity loans, which use the property’s built-up value to fund larger renovation projects.

How Renovation Loans Work?

Renovation loans in Malaysia are typically offered at a fixed interest rate, meaning your monthly repayment stays the same throughout the loan period. This makes budgeting easier, especially for homeowners managing other ongoing expenses.

Most banks require the following documents during the application process:

- Copy of IC and proof of property ownership

- Quotation or invoice from a registered contractor

- Latest payslips or income statement (usually three months)

- EPF statement or tax return for income verification

Approval usually takes between one and three weeks, depending on the bank and loan type. Once approved, the funds are disbursed directly to your account or to your appointed contractor.

Typical Loan Example (2026 Rates)

Here is a simplified example of how a loan for renovation might look based on current market rates:

50,000

5.5

5

57,063

951

50,000

7.0

10

70,164

584

As the table shows, a longer tenure reduces monthly instalments but increases the total amount you pay over time. It is important to calculate both short-term affordability and long-term cost before deciding on your loan structure.

Interest Rate Trends in 2026

According to Bank Negara Malaysia (BNM), the Overnight Policy Rate (OPR) has remained stable at around 2.75% in early 2025. This means borrowing costs are moderate, though banks still set their own profit margins based on customer credit profiles.

For renovation financing, the profit rates can be 5.37% – 11.51% per annum, depending on:

- Loan type (secured vs. unsecured)

- Your credit score and income stability

- The size and duration of the loan

It is advisable to compare rates across multiple banks and check if you qualify for promotional packages offered to existing mortgage holders.

Borrowing Responsibly

While a loan for renovation can help you achieve your dream home sooner, it is essential to borrow within your means. Personal loans remain one of the leading causes of debt distress among Malaysians. To avoid overextension:

- Keep your Debt Service Ratio (DSR) below 40% of your monthly income.

- Maintain an emergency fund for unexpected project costs.

- Avoid borrowing the maximum amount offered; focus only on what you truly need.

A well-planned renovation loan can turn your home improvement ideas into reality without compromising your financial stability. The key lies in understanding your repayment capacity, comparing available loan options, and choosing a plan that fits both your renovation goals and long-term budget.

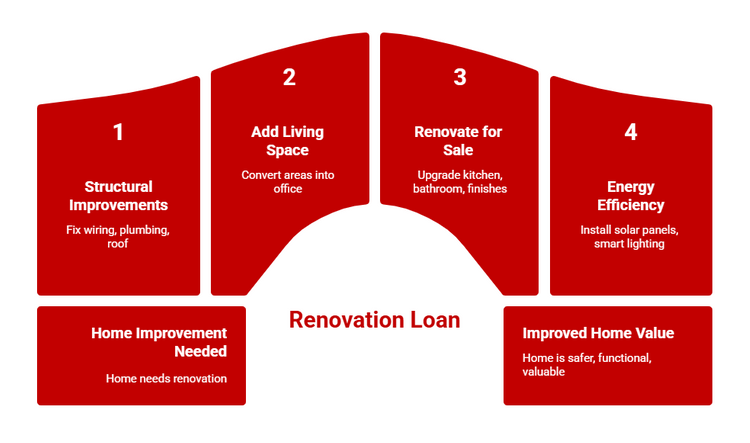

When Taking a Loan for Renovation Makes Sense?

A loan for renovation can be a smart financial move if the project improves your home’s safety, functionality, or long-term value. Here are some common situations where borrowing makes sense for Malaysian homeowners:

1. Structural or Safety Improvements

If your home’s wiring, plumbing, or roof is showing signs of wear, fixing these issues early can prevent further damage and higher repair costs later. Borrowing for essential repairs such as rewiring, waterproofing, or structural reinforcement is often justified because these improvements directly protect your property’s integrity.

2. Adding Functional Living Space

With more Malaysians embracing hybrid work arrangements, converting underused areas into a home office or study room has become increasingly popular. Similarly, adding a new bedroom, extending the kitchen, or reconfiguring layouts can significantly enhance daily comfort. A well-planned extension funded through a manageable renovation loan can be a practical long-term investment.

3. Renovating Before Selling or Renting

If you are preparing your property for sale or rental, targeted renovations can boost its appeal and potential return on investment.

For instance, spending RM80,000 to upgrade a kitchen and bathroom, add built-in wardrobes, and refresh interior finishes could increase resale value by around RM100,000, depending on market demand and location. While returns vary, strategic improvements can make your property stand out in a competitive market.

4. Energy Efficiency and Modernisation

Homeowners are also turning to energy-efficient and smart upgrades to reduce long-term costs. Installing solar panels, smart lighting, and water-saving fixtures can lower utility bills and attract eco-conscious buyers.

In 2025, the Malaysian Government continues to support sustainable housing through initiatives such as the Solar for Rakyat Incentive Scheme (SolaRIS), which offers rebates of up to RM4,000 for eligible solar installations, and the Net Energy Metering (NEM) Rakyat programme, which allows households to offset electricity bills by exporting solar energy to the grid.

When Is It Worth Considering?

If your renovation plans focus on improving safety, functionality, or sustainability, and your financial situation allows for consistent loan repayments, taking out a loan for renovation can be a worthwhile decision.

However, if your project is purely aesthetic or you have not yet factored in hidden costs such as home renovation permits, material price fluctuations, or temporary accommodation, it may be wiser to postpone the renovation until your budget is more secure.

Check Home Loan Eligibility

Quickly find out how much you could borrow.

When You Should Think Twice About Borrowing?

Not every home upgrade justifies taking out a loan for renovation. While financing can help you achieve your dream home sooner, borrowing without a clear purpose or planning can turn an exciting project into a long-term financial strain.

1. Aesthetic or Trend-Based Upgrades

Borrowing for purely cosmetic changes such as designer fittings, imported tiles, or luxury finishes rarely pays off. These upgrades can inflate costs without increasing your property’s market value. If your goal is style rather than structure, it is better to save up or complete the work in phases.

2. Limited Impact on Property Value

Not all renovations boost resale potential. Converting a bedroom into a walk-in closet or building a private gym may suit your needs but reduce your home’s appeal to buyers. Property valuers typically prioritise functional upgrades, like additional bathrooms, kitchen extensions, or rewiring, over aesthetic ones.

3. Market Fluctuations and Overcapitalisation

Before taking a loan, consider your area’s property market. In slower or saturated locations, even well-executed renovations may not deliver high returns. Overcapitalisation, spending more on a home than the market will support, is a common mistake. For instance, investing RM250,000 in a property worth RM400,000 makes little sense if resale value only rises modestly.

If your renovation is driven by lifestyle desires rather than safety, function, or necessity, it may be wiser to wait, save, or scale down. A loan for renovation should improve your home’s comfort and value, not create unnecessary debt.

Costs, Interest Rates, and Repayment Examples

Before taking out a loan for renovation, it is crucial to understand how interest rates and tenures affect your total repayment amount. Renovation loans may seem manageable at first glance, but costs can add up significantly over time.

Current Loan and Interest Rate Landscape in 2026

As of early 2025, Bank Negara Malaysia (BNM) has maintained the Overnight Policy Rate (OPR) at around 2.75%, keeping borrowing costs relatively stable. However, banks still set their own rates depending on your credit profile and whether the loan is secured or unsecured.

Here is how interest rates typically compare across different loan types:

Secured Renovation Loan (Home + Reno Package)

Linked to your existing home loan; lower risk for the bank and often lower rates

May start from around 4% p.a., depending on bank packages

Up to 35 years when bundled with a mortgage

Unsecured Renovation Loan (Personal Loan)

Standalone loan without collateral; approval based on creditworthiness

Typically from about 4.5% to 7% p.a.

1 to 10 years

Home Equity or Refinancing Loan

Allows you to borrow using your property’s built-up value

Generally from 4% to 6% p.a.

10 to 25 years, depending on bank policy

Interest rates vary depending on your income, credit score, and lender promotions. Always compare multiple banks before deciding.

Example: How Loan Tenure Affects Total Cost

Below is a simplified example to show how tenure and interest rate impact your overall repayment:

50,000

5.2

5

56,875

948

50,000

7.5

10

71,310

594

Key Notes:

- A shorter tenure means higher monthly instalments but less total interest paid.

- A longer tenure reduces monthly payments but increases the total repayment amount.

Factors That Influence Your Interest Rate

Banks evaluate several factors before offering a renovation loan rate, including:

- Credit score and repayment history: A higher score may help you secure a lower interest rate.

- Income and debt level: Lenders assess your debt service ratio (DSR) to ensure you can manage repayments.

- Loan amount and tenure: Larger or longer loans often come with slightly higher rates.

- Loan type: Secured loans generally have lower interest rates than unsecured personal loans.

Before You Borrow

When calculating affordability, consider more than just the monthly instalment. Add up the total repayment over the entire tenure to understand the real cost of borrowing.

Tip: Always calculate the total repayment cost, not just the loan amount. This ensures you make informed decisions and avoid underestimating the true financial commitment of your renovation project.

Key Considerations Before Applying for a Renovation Loan

Taking out a loan for renovation is a major financial decision. Before applying, it is important to evaluate your readiness, budget, and repayment capacity to ensure that your renovation enhances your home without straining your finances.

Budget and Quotations

Start by preparing a detailed home renovation budget. Get at least three quotations from licensed or CIDB-registered contractors to compare prices, workmanship, and timelines. Ensure each quote includes both labour and material costs, as well as any additional charges such as permit fees or design consultation.

It is also wise to add a 10% to 15% contingency buffer for unexpected expenses like material price increases or minor scope changes. This cushion helps you stay on track even if costs fluctuate during the project.

Loan Eligibility and Credit Score

Your credit score plays a major role in whether your loan is approved and at what interest rate. Banks in Malaysia assess your repayment history, existing debts, and income stability before approving a renovation loan. A healthy credit score demonstrates reliability and can help you qualify for lower interest rates or higher financing limits.

Before applying, review your CTOS Score to understand where you stand and identify areas for improvement, such as reducing outstanding debts or correcting outdated credit records.

Tenure, Interest Rate, and Repayment Plan

The loan tenure directly affects how much you pay overall. A shorter tenure means higher monthly instalments but lower total interest, while a longer tenure reduces your monthly burden but increases the total repayment amount.

As a rule of thumb, try to keep your monthly loan repayments within 30% to 40% of your household income. This ensures financial flexibility for other commitments such as insurance, education, or emergency expenses. Use your bank’s loan calculator or an online repayment tool to visualise the full repayment amount before signing any agreement.

Risk Management

Even with careful planning, renovation projects can face unexpected challenges such as material delays, contractor disputes, or cost inflation. Always choose reputable, licensed contractors and ensure you have a signed agreement that outlines timelines, payment milestones, and penalties for delays.

Keep an emergency buffer of around 10% of your total renovation cost to manage unforeseen expenses without relying entirely on borrowed funds. Avoid using the entire approved loan amount upfront; stagger disbursements based on project progress to maintain better control of spending.

Proper planning, a strong credit profile, and clear financial boundaries can make your renovation experience smoother and more rewarding. A well-structured loan for renovation should help you enhance your home’s comfort and value, not create unnecessary financial stress.

Pros and Cons of Taking a Loan for Renovation

Before deciding on a loan for renovation, it is important to weigh both the benefits and drawbacks carefully. While renovation loans make it easier to upgrade your home, they also come with long-term financial responsibilities.

| Pros | Cons |

| A renovation loan allows you to begin your project immediately instead of waiting to save. This is especially useful for urgent repairs or safety-related improvements. | A loan adds to your overall debt and monthly obligations. Without proper planning, repayments can strain your budget. |

| Financing helps you spread out renovation costs over time, allowing you to preserve your savings and emergency funds for other priorities. | Longer loan tenures increase total interest paid. For example, a RM50,000 loan over 10 years can cost more than RM70,000 after interest. |

| Well-planned renovations, such as kitchen or bathroom upgrades, can increase your home’s resale or rental value. | Not all renovations lead to higher property value. Highly personalised designs or luxury finishes may not appeal to future buyers. |

| Fixed-rate renovation loans offer predictable monthly instalments, making it easier to manage your finances. | Approval depends on your credit score, income stability, and existing debts. A lower credit score may result in higher interest rates. |

| Malaysian banks offer various financing options, from home-plus-renovation packages to personal loans, giving you flexibility to choose what fits your needs. | Renovation projects can face delays, material price increases, or disputes with contractors, which may inflate costs even after loan approval. |

Balancing the Decision

A loan for renovation can be a smart solution if it enhances your home’s comfort, safety, or long-term value and fits within your repayment capacity. However, if the renovation is purely aesthetic or your financial situation is uncertain, it may be better to wait or scale down your plans.

Before applying, review your renovation goals, compare multiple bank offers, and ensure that monthly repayments remain within your comfort zone. The right renovation loan should help you build a better home, not additional financial stress.

Home Loan Calculator

Estimate monthly repayments and total cost before you borrow.

Making a Smart Renovation Financing Decision

Taking a loan for renovation can be a smart move if it helps you improve your home’s comfort, safety, or long-term value, but it should always be approached with careful planning. Evaluate your renovation goals, compare loan options, and ensure that repayments fit comfortably within your monthly budget.

For more property news, homeowner tips, and financing guides, visit the PropertyGuru Malaysia Guides section.

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.