Choosing the correct home loan interest rate is one of the most defining financial decisions you’ll make as a homeowner, shaping not just your monthly repayments but your overall financial stability for years to come.

Whether you lean towards the steady security of a fixed rate or the adaptable nature of a variable (floating) interest rate, understanding how each works is essential for building long-term financial confidence.

As Malaysia moves into 2026, shifting market conditions are creating a new landscape for borrowers. Economic recovery, digital innovation in lending, and Bank Negara Malaysia’s (BNM) evolving monetary policies are influencing how rates move and how banks structure their loans.

Property demand continues to hold firm, but borrowing costs are now more fluid than ever, making it vital to know exactly how your mortgage rate could shape your financial journey.

| Table of Contents 1. Understanding How Mortgage Interest Rates Work in Malaysia 2. Fixed Rate Mortgages: Predictability and Stability 3. Variable Interest Rate Mortgages: Flexibility and Market Responsiveness 4. Malaysia’s Interest Rate Landscape in 2025 5. From BLR to BR: A More Transparent System 6. Practical Example: Fixed vs Variable Rate Loans (2025 Scenario) 7. Pros and Cons Summary Table 8. 2025-2026 Market Trends: What Borrowers Should Know? 9. Tips for Managing a Variable Interest Rate Loan 10. Choosing Between Fixed and Variable: How to Decide? 11. Expert Insight: What 2026 Could Bring 12. Making an Informed Choice in 2026 |

Explore rental homes across Malaysia.

Find units that match your budget.

Understanding How Mortgage Interest Rates Work in Malaysia

When you apply for a housing loan, the interest rate determines how much extra you’ll pay the bank on top of your loan principal. Over decades, that difference can easily add up to hundreds of thousands of ringgit, so even a small variation matters.

There are two main types of housing loan rates available in Malaysia:

- Fixed Rate Mortgages: where your interest rate remains constant throughout your loan tenure.

- Variable (Floating) Rate Mortgages: where your rate moves up or down in line with changes in market benchmarks such as the Base Rate (BR).

Both types can be appealing depending on your financial goals, risk appetite, and income stability.

Estimate your monthly repayments with ease

To understand your financing range before you commit

Fixed Rate Mortgages: Predictability and Stability

A fixed-rate mortgage offers certainty. Your interest rate stays the same throughout your loan term, regardless of market fluctuations. For instance, if you secure a 4.50% rate for 25 years, you’ll continue paying that percentage even if Malaysia’s OPR rises or falls.

This predictability helps borrowers plan. It’s particularly suitable for:

- First-time buyers managing tight monthly budgets

- Families or retirees with fixed incomes

- Anyone who values stability over potential savings

However, fixed-rate loans often have slightly higher initial rates than floating-rate loans, as the bank assumes the risk of future rate changes.

Benefits of Fixed Rate Mortgages

Here are the key advantages to keep in mind:

- Budget Certainty: Your instalments never change, making financial planning simpler.

- Protection Against Rising Rates: Even if the OPR jumps, your payments remain unaffected.

- Peace of Mind: Eliminates the worry of unexpected rate hikes that could stretch your finances.

Drawbacks of Fixed Rate Mortgages

Now let’s look at the potential downsides:

- Higher Initial Interest Rates: Fixed loans tend to cost 0.3% to 0.6% more than floating options.

- Potential Loss of Savings: If market rates fall, you won’t benefit unless you refinance.

- Lock-In Period Penalties: Many fixed-rate packages charge early settlement fees (2-3%) if you refinance too soon.

Overall, a fixed-rate mortgage is best for anyone prioritising stability and long-term financial peace of mind.

Variable Interest Rate Mortgages: Flexibility and Market Responsiveness

A variable interest rate mortgage, also known as a floating rate loan, adjusts according to the Base Rate (BR) set by individual banks. The BR, in turn, is influenced by Bank Negara Malaysia’s OPR, as well as other factors such as funding costs and liquidity risks.

The impact of OPR changes, however, does not occur instantly; banks may adjust their BRs at different times, depending on internal policies and market conditions.

Your total rate is calculated as:

Effective Lending Rate = Base Rate (BR) + Spread

- The Base Rate (BR) reflects the bank’s funding cost and compliance with statutory reserve requirements.

- The Spread is an additional margin determined by the bank, reflecting its operational costs and risk profile.

So, if your bank’s BR is 3.00% and your spread is 1.10%, your total rate becomes 4.10%.

When the OPR increases, the BR typically follows suit, which means your monthly instalments may rise. When the OPR falls, your repayments may decrease.

Malaysia’s Interest Rate Landscape in 2025

As of November 2025, Malaysia’s OPR remains at 3.00%, after a series of stabilisation measures introduced by BNM earlier in the year. Most major banks, including Maybank, CIMB, and RHB, list their BRs between 2.75% and 3.10%, depending on internal cost structures.

Economic analysts forecast that the OPR may hover between 3.00% and 3.25% throughout 2026, barring any significant inflation spikes or global financial shocks.

This means borrowers choosing variable rate mortgages could see modest rate adjustments in the coming year, but nothing as drastic as the volatility seen during 2022-2023’s global inflation wave.

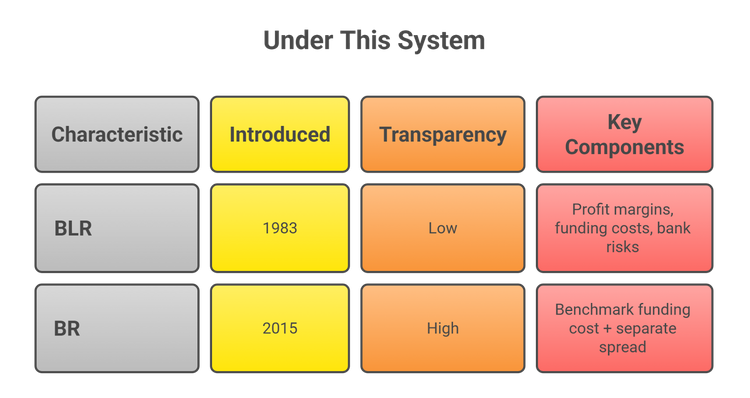

From BLR to BR: A More Transparent System

Before 2015, home loans were based on the Base Lending Rate (BLR), which encompassed a combination of factors, including bank profit margins, liquidity costs, and credit risks.

The problem? It lacked transparency; borrowers couldn’t easily compare loan offers.

In 2015, Bank Negara Malaysia introduced the Base Rate (BR) system to increase clarity.

Now, borrowers can directly compare the BR and the spread between banks to identify the most competitive packages.

Practical Example: Fixed vs Variable Rate Loans in 2025

Imagine you’re applying for an RM500,000 mortgage over 25 years.

Fixed Rate

4.90% p.a.

RM2,885

RM19,960

Variable Rate (BR + 1.10%)

4.40% p.a.

RM2,700

RM17,800

The difference in interest payments for the first year alone is RM2,160.

But if the OPR rises by 1%, pushing the effective rate to 5.40%, your variable-rate instalment could increase to RM2,980, exceeding the fixed-rate payment.

This example illustrates that while variable rates can save you money in a stable or declining OPR environment, they carry more risk when the market shifts upward.

Fixed Vs Variable Home Loans At A Glance

Before making your decision, it’s helpful to compare the two loan types side by side.

The table below summarises the key differences between fixed and variable interest rate mortgages, providing a clearer view of which one might better suit your financial goals and lifestyle:

Rate Stability

High

Low

Initial Cost

Slightly higher

Usually lower

Impact of OPR Changes

None

Direct

Budget Planning

Predictable

Requires flexibility

Refinancing Flexibility

Limited (lock-in period)

Easier (depending on loan terms)

Suitable For

Stable income, long-term planners

Dynamic earners, short-term investors

While both have their merits, the right choice ultimately depends on your financial comfort level and plans. In the following section, we’ll explore current market trends and what borrowers should watch heading into 2025 and 2026.

2026 Market Trends: What Borrowers Should Know?

As Malaysia’s housing market continues to evolve, borrowers need to understand the broader financial trends that could shape their mortgage decisions in 2025 and 2026.

The following highlights will help you stay ahead of these changes and make more informed choices:

- Digital Banks Are Changing the Game

New digital players, such as GXBank and AEON Bank, are introducing competitive floating-rate packages with minimal fees and faster approval processes. Expect more flexible repayment options and personalised BR-linked loans in 2026. - Refinancing Momentum Growing

With OPR stabilising, many homeowners are refinancing from older, higher-rate loans to newer variable-rate packages that offer better terms or flexi features. - Property Demand Shifts to Urban Centres

Areas such as the Klang Valley, Johor Bahru, and Penang continue to attract homebuyers, prompting banks to offer aggressive rate promotions to first-time buyers. - Inflation Pressure Easing

BNM’s inflation forecast remains moderate at 2.8%-3.2%, reducing the likelihood of sudden OPR hikes, good news for variable-rate borrowers. - Flexi Home Loans Gaining Popularity

Many banks are now offering semi-flexible and fully flexible variable loans, allowing borrowers to deposit extra funds into their mortgage accounts and reduce the interest payable.

These market shifts show that Malaysia’s lending environment is becoming more competitive, digital-first, and borrower-friendly.

Tips for Managing a Variable Interest Rate Loan

The following tips will help you navigate rate fluctuations confidently and make the most of your variable-rate mortgage:

- Track the OPR Regularly

BNM typically reviews it six times a year. Staying informed helps anticipate changes before they affect your repayment. - Set Up an Emergency Fund

Keep 3-6 months’ worth of instalments as a safety net for unexpected rate hikes. - Make Lump-Sum Payments

Whenever you receive bonuses or windfalls, consider paying down your loan principal; it lowers your interest burden. - Opt for Flexi Features

Look for loans that allow redraws or extra repayments without penalties. - Refinance When the Timing Is Right

If market rates drop significantly, explore refinancing to lock in savings.

By adopting these strategies, you can better manage the uncertainties of a floating-rate loan and maintain control over your finances, even in changing economic conditions.

Choosing Between Fixed and Variable: How to Decide?

Deciding between a fixed and variable interest rate can feel daunting, especially when both options have their merits.

Here’s a quick guide based on your borrower profile:

First-Time Buyer

Fixed

Certainty and budget control during early financial years

Young Professional

Variable

Potential savings and flexibility as income grows

Investor

Variable

Lower short-term cost for investment properties

Retiree or Conservative Borrower

Fixed

No exposure to OPR changes

Entrepreneur

Variable

Ability to leverage redraw or overdraft facilities

If you’re unsure, some banks offer hybrid loans, where a portion of the loan is fixed, and the rest is variable. This provides a balanced approach that balances stability and flexibility.

Expert Insight: What 2026 Could Bring

According to BNM’s Financial Stability Report 2025, Malaysia’s household debt-to-GDP ratio has declined slightly to 82%, reflecting improved financial resilience among homeowners.

The central bank is expected to maintain its data-driven approach, adjusting the OPR cautiously to strike a balance between growth and inflation control.

For borrowers, this likely means mild fluctuations in the OPR and continued competition among banks to offer the best mortgage packages.

For borrowers, this likely means mild fluctuations in the OPR and continued competition among banks to offer the best mortgage packages.

Industry experts predict that by mid-2026, more lenders will adopt AI-driven loan assessment models, making variable-rate loans more customised to borrowers’ spending behaviour and credit patterns.

Making an Informed Choice in 2026

Ultimately, choosing between a fixed- and variable-rate mortgage is not just a numbers game; it’s a decision shaped by your financial goals, income stability, and risk appetite.

A fixed rate may be the wiser route if you value certainty, stable repayments, and the comfort of knowing exactly what your monthly commitment will be, regardless of how the market shifts.

On the other hand, a variable rate can be rewarding for borrowers who are confident in managing change and want the flexibility to benefit when interest rates fall. It allows room for potential savings and adaptability, especially for those whose income may rise over time or who plan to refinance strategically.

Whichever path you take, be sure to carefully compare offers from different lenders, study the fine print, and ensure that your loan structure aligns with your long-term financial plans. The best mortgage isn’t simply the cheapest one; it’s the one that supports your lifestyle, future goals, and peace of mind.

Ready to explore your options? Check out property listings on PropertyGuru Malaysia now!

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.