Navigating Malaysia’s property market can be daunting, especially for first-time buyers who face rising prices and a complex array of incentives. Among these, the Home Ownership Campaign, or HOC, stands out as a government-backed initiative designed to make homeownership more attainable while stimulating market activity.

Since its launch in 2019, the campaign has played a pivotal role in reducing unsold housing stock by providing financial relief through stamp duty exemptions, developer discounts, and other targeted incentives.

This guide provides a comprehensive overview of HOC 2025, covering its eligibility criteria, benefits, registration process, market impact, and expert insights, offering practical clarity for those considering their next property purchase in Malaysia.

| Table of Contents 1. What Is HOC and Why Does It Matter in Malaysia? 2. HOC-Like Incentives Under Budget 2025: A Quick Overview 3. The Real Meaning of HOC in Property 4. How HOC Started: From 2019 to 2025 5. HOC 2025: Who Qualifies and How It Works 6. Key Benefits of HOC for Homebuyers 7. Eligible Properties Under HOC 8. How Developers Participate in HOC 9. HOC Registration Process: Step-by-Step 10. Hidden Terms and Conditions You Should Know 11. The Impact of HOC on Malaysia’s Property Market 12. What Happens After HOC Ends? 13. Comparing HOC to Other Government Housing Schemes 14. Is HOC 2025 Still Worth It? Expert Insights 15. Making the Most of HOC in 2025 |

Explore rental homes across Malaysia.

To find units that match your budget

What is HOC, and why does it matter in Malaysia?

If you’ve ever stumbled upon the term HOC while browsing new property launches or developer promotions, you might have wondered what it truly entails. The acronym stands for Home Ownership Campaign, a nationwide initiative first introduced by the Malaysian government to encourage homeownership while helping developers reduce the country’s growing stock of unsold properties.

But understanding the meaning of HOC in property goes well beyond its name. It represents a strategic partnership among the government, REHDA Malaysia, and participating developers, all working together to make homeownership more accessible to Malaysians. The campaign’s primary aim is to bridge the affordability gap by easing buyers’ financial strain through stamp duty exemptions, special developer rebates, and lower entry costs.

For many first-time buyers, the HOC can make a decisive difference, often translating into savings worth tens of thousands of ringgit, allowing them to purchase the same property at a substantially reduced overall cost. More importantly, it fosters market activity, giving both buyers and developers renewed confidence in Malaysia’s evolving property landscape.

HOC-Like Incentives Under Budget 2025: A Quick Overview

While not formally reintroduced as the Home Ownership Campaign (HOC), the 2025 Budget continues HOC-like incentives, including stamp duty relief and developer participation under KPKT oversight, to sustain housing demand and support affordability.

These measures encompass:

- Stamp duty exemptions for first-time buyers of selected residential properties.

- Many developers continue offering voluntary discounts similar to HOC’s structure.

- Several banks offer HOC-style packages, but they are private.

The initiative reflects the government’s ongoing commitment to revitalising the property market, ensuring a balanced approach that benefits both aspiring homeowners and developers navigating a more cautious economic climate.

The Real Meaning of HOC in Property

In essence, the HOC (Home Ownership Campaign) in Malaysia refers to a time-limited, government-backed initiative designed to ease the financial burden of homeownership. Rather than functioning as a loan or grant, it operates as a purchase incentive framework, helping buyers save significantly on upfront costs through stamp duty exemptions, developer discounts, and reduced legal fees.

The scheme is designed to make homeownership more attainable, particularly for first-time buyers navigating rising property prices and living costs. During active HOC periods, only developers certified by REHDA Malaysia and approved by the Ministry of Housing and Local Government (KPKT) are permitted to market their projects under the HOC banner. This oversight ensures that all participating developments meet eligibility criteria and maintain transparency in pricing and incentives offered to buyers.

Ultimately, HOC represents more than a short-term relief measure; it’s a carefully structured effort to stimulate the housing market while promoting responsible, accessible homeownership across Malaysia.

How HOC Started: From 2019 to 2025

The Home Ownership Campaign (HOC) was first introduced in 2019 as part of the Malaysian government’s broader initiative to address two key challenges: the nation’s growing affordability gap and the high volume of unsold housing units, often referred to as a property overhang.

During its initial run between 2019 and 2022, the campaign proved remarkably effective. According to REHDA Malaysia, it generated over RM23 billion in property sales, providing much-needed momentum to a market subdued by economic uncertainty.

For many Malaysians, it represented a tangible opportunity to own a home at a more accessible price point, supported by developer discounts and government-backed reliefs.

After a brief pause, the spirit of the HOC was reintroduced through a series of housing-related incentives in Budget 2023 and later reaffirmed in Budget 2025. While not always branded as HOC, these measures, including stamp duty exemptions and developer participation under KPKT oversight, continue to carry out their core purpose.

This evolution highlights how the HOC has become more than a one-off campaign; it now functions as a recurring policy framework that adapts to shifting market conditions, supporting both first-time buyers and existing homeowners looking to upgrade. In essence, HOC remains a cornerstone of Malaysia’s ongoing effort to make homeownership more achievable and sustainable for its people.

HOC 2025: Who Qualifies and How It Works?

HOC benefits are primarily for Malaysian citizens purchasing new residential properties from participating developers.

Eligibility Requirements

- Buyer must be a Malaysian citizen.

- The property must be used for residential purposes (not commercial).

- Purchased directly from a developer registered under the scheme.

- SPA (Sales and Purchase Agreement) must be signed within the active campaign period.

Typical Price Range

Under previous HOC editions (the latest confirmed as of 2021), properties valued up to RM2.5 million qualified.

Key Benefits of HOC for Homebuyers

The main attraction of HOC lies in its financial advantages. Here’s what buyers typically enjoy:

| Benefit | Description |

| Stamp Duty Exemption (SPA) | Full exemption for residential properties within the price range, significantly reducing upfront costs. |

| Stamp Duty Exemption (Loan Agreement) | Often waived or reduced, subject to campaign guidelines. |

| Minimum 10% Discount from Developers | All registered developers must offer a minimum 10% discount on the selling price. |

| Additional Bank Incentives | Selected banks partner with the government to offer competitive home loan rates. |

| Legal Fee Support | Many developers offer partial coverage of legal fees for SPA and loan agreements. |

These advantages can translate into tens of thousands of ringgit in savings, a decisive factor for many first-time buyers.

Looking for HOC-approved homes? Browse PropertyGuru’s new project listings for the latest developments under government incentives.

Eligible Properties Under HOC

Typically, only residential properties are covered, which include:

- Condominiums and apartments

- Landed homes (terrace, semi-D, and bungalows)

- Serviced residences (where approved for residential titles)

Properties with commercial titles, subsales, or those owned individually are excluded from this analysis.

This keeps HOC focused on new, developer-launched homes that support the national supply chain.

How Developers Participate in HOC?

To participate in the Home Ownership Campaign, developers must first be registered with REHDA Malaysia, SHEDA in Sabah, or SHAREDA in Sarawak. Each developer is required to submit their proposed projects for official vetting and approval, ensuring that every listing under the campaign adheres to strict standards of transparency, eligibility, and pricing integrity.

This approval process is not merely procedural; it serves as an essential safeguard for buyers. Once a project has been certified, it can then carry the HOC branding, a clear indication that its advertised discounts, stamp duty exemptions, and incentives have been verified and endorsed by the authorities.

For homebuyers, this verification offers peace of mind, reducing the risk of misleading marketing and reaffirming that the advertised savings are genuine, regulated, and officially sanctioned under the HOC framework.

HOC Registration Process: Step-by-Step

For buyers, the process is simple:

- Check REHDA’s official list of participating developers.

- Select a qualifying property.

- Sign the Sales and Purchase Agreement within the campaign period.

- Submit your application for stamp duty exemption via the LHDN (Inland Revenue Board).

- Keep all documentation for audit or refund verification.

For developers, REHDA provides a separate developer registration portal for HOC certification.

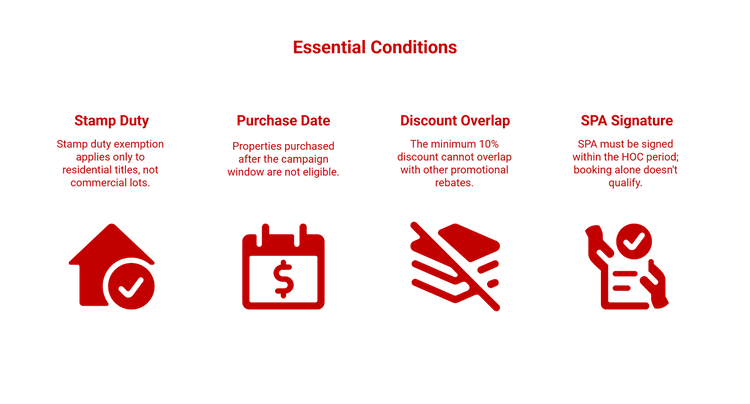

Hidden Terms and Conditions You Should Know

While the HOC offers substantial savings, many buyers overlook the finer print that can affect eligibility and benefits.

Before signing anything, ensure you understand these:

By staying aware of these details, buyers can avoid unexpected disqualifications and fully utilise the HOC’s genuine financial advantages.

The Impact of HOC on Malaysia’s Property Market

According to REHDA, HOC significantly reduced unsold stock in central states such as Selangor, Johor, and Penang between 2019 and 2022.

It encouraged developers to clear existing inventory while maintaining active housing demand, especially among young professionals and first-time buyers.

Even after the campaign’s official end, the "HOC effect" remains visible in market trends: developers continue offering HOC-style packages, recognising that affordability remains a core concern.

What Happens After HOC Ends?

When the campaign concludes, the direct stamp duty exemptions will end. That said, many developers often continue to roll out "HOC-inspired" incentives, such as bundled discounts, furnishing packages, or even covering legal fees.

These offers ensure that buyers can still enjoy tangible savings and added value, even when purchasing outside the official campaign period.

Estimate your monthly repayments with ease

To understand your financing range before you commit

Comparing HOC to Other Government Housing Schemes

HOC is unique because it supports mid-range to higher-end properties, whereas other initiatives, such as PR1MA, RUMAWIP, or BSH housing schemes, focus on affordable housing.

HOC

Middle-income buyers

Stamp duty and discount incentives

PR1MA

M40 and B40 segments

Affordable homes between RM100k and RM400k

RUMAWIP

KL residents

Affordable units under RM300k

My First Home Scheme

First-time buyers

Financing up to 110%

Each caters to different buyer profiles, but HOC bridges the affordability gap for those who can afford mid-range projects but are discouraged by fees.

Is HOC-Style Support Still Worth It in 2026? Expert Insights

As we enter 2026, industry experts agree that HOC-style incentives remain highly relevant given ongoing affordability challenges and a significant volume of unsold residential units.

Although an official HOC has not been relaunched, the government continues to introduce measures that mirror its intent, helping buyers manage rising costs while stabilising the housing market.

What Industry Experts Are Saying

- Market analysts highlight that Budget 2026 maintains full stamp duty exemptions for first-time buyers on homes up to RM500,000, with the exemption extended until 2027. This continues the core benefit that made HOC attractive.

- Property reports also show that affordability remains a top concern, especially among young households, strengthening the need for HOC-like support programmes.

- Developers are expected to keep offering HOC-inspired rebates, furnishing packages and entry-cost assistance, which help clear existing inventory and maintain steady sales momentum.

Why These Incentives Matter in 2026

- Buyers get lower upfront costs through ongoing stamp duty relief.

- Developers continue to offer voluntary discounts, reducing barriers to homeownership.

- Banks are offering competitive loan packages similar to those provided in past HOC collaborations.

- The market remains price-sensitive, making cost-saving incentives more impactful.

Even without a formal HOC relaunch, the incentives available in 2026 still deliver meaningful savings comparable to HOC. For many buyers, these measures remain one of the most effective ways to reduce entry costs and confidently secure a new home.

HOC Meaning in Property: Turning Incentives Into Smarter Homebuying Decisions

The HOC’s meaning in property extends far beyond a temporary housing campaign; it represents Malaysia’s ongoing effort to make homeownership accessible to more citizens.

As housing costs rise and supply adjusts, initiatives like HOC remain critical in helping buyers take that first step confidently.

If you’re planning to purchase a new home this year, explore listings under active government incentives or developer-led HOC programmes to maximise your savings and secure a home that meets your long-term goals.

Keep Track of New Launches

Visit our new launches page to find the new launch project of your dreams and submit an enquiry today.

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.