Buying your first commercial property can feel like a big leap, especially when you’re faced with unfamiliar terms, complex documents, and strict loan requirements. Whether you’re a small business owner eyeing your own shop lot or an investor expanding into office spaces, figuring out how commercial loans work is often the most confusing part of the journey.

In today’s market, banks are tightening credit standards while offering new and flexible packages for qualified borrowers. From profit-based Islamic financing to high-margin SME loans, there are now more options and more fine print than ever before.

This guide simplifies everything. You’ll learn how commercial property loans in Malaysia work, what banks look for in applicants, and the key steps to prepare before applying. By the end, you’ll understand how to choose the right loan and make your commercial investment work smarter for you.

| Table of Contents 1. What Are Commercial Property Loans? 2. How Commercial Loans Differ From Residential Loans 3. How Commercial Property Loans Work in Malaysia Today 4. What Are the Types of Commercial Loans Available? 5. How To Apply for a Commercial Property Loan (Step-by-Step) 6. Common Pitfalls To Avoid When Applying for Commercial Loans 7. How Can You Prepare for Your Commercial Loan Application? |

Find Commercial Properties That Suit Your Financing Goals

Explore shop lots, offices, and industrial units that fit your budget.

What Are Commercial Property Loans?

A commercial property loan, often referred to as a commercial loan, is a financing facility designed to help individuals or businesses purchase, refinance, or develop properties used for business or investment purposes.

Unlike a home loan, which helps you buy a place to live, a commercial loan helps you acquire property that can generate income or support business operations.

In Malaysia, commercial loans are commonly used to finance properties such as:

- Shop lots and shop offices

- Office suites and corporate towers

- Warehouses and factories

- SoHo, SoVo, and SoFo units (depending on bank policy)

- Commercial and industrial land

These loans are available to a range of borrowers, including individuals, sole proprietors, partnerships, and private limited companies (Sdn. Bhd.). The amount you can borrow and the terms offered will depend on factors such as your financial strength, business stability, and the type and location of the property.

Commercial property loans in Malaysia can also take the form of Islamic financing, which follows Shariah principles. Under this structure, banks may use concepts like Murabahah (cost-plus financing) or Ijarah (leasing) to structure the repayment instead of charging conventional interest.

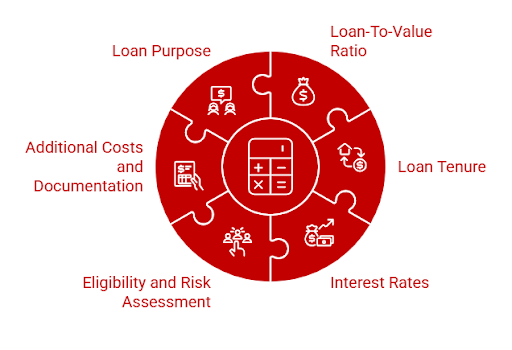

How Commercial Loans Differ From Residential Loans

At first glance, commercial property loans may seem similar to home loans; both help you finance a property purchase through a bank. However, they differ significantly in purpose, eligibility, risk level, and repayment structure.

Understanding these differences can help you plan your finances more effectively and avoid surprises during the loan process.

- Loan-To-Value (LTV) Ratio

Residential loans in Malaysia are subject to Bank Negara Malaysia’s loan-to-value (LTV) limits. For example, you can typically get up to 90% financing for your first or second residential property, but only 70% for your third.

Commercial loans, however, are not bound by the same rules. Banks determine the margin of financing based on their internal policies, usually offering between 80% and 85% of the property’s market value or purchase price. Some banks may even go as high as 90% for strong applicants or owner-occupied properties.

This flexibility makes commercial loans attractive to investors and business owners who need higher leverage for growth.

- Loan Tenure

Residential mortgages in Malaysia can stretch up to 35 years, depending on the borrower’s age and repayment capacity. Commercial property loans, on the other hand, usually have shorter tenures, often capped at 25 to 30 years or until the borrower reaches age 70, whichever comes first.

A shorter loan period means higher monthly instalments but also a quicker payoff and lower total interest over time. Borrowers should plan their cash flow accordingly.

- Interest or Profit Rates

Commercial loans generally carry slightly higher interest or profit rates than residential mortgages, as banks consider them riskier due to their business-related nature.

Some banks also offer flexible or semi-flexible plans that allow borrowers to make prepayments or redraw excess funds to manage interest costs more efficiently.

- Eligibility and Risk Assessment

Commercial property financing involves stricter eligibility checks. In addition to personal income or credit score, banks evaluate:

- Business performance: Annual revenue, profit margin, and cash flow consistency

- Company documents: Form 24, Form 49, and audited financial statements

- Property characteristics: Location, accessibility, tenant potential, and resale value

Properties located in prime commercial hubs like Kuala Lumpur City Centre (KLCC), Petaling Jaya, or Johor Bahru typically have a higher approval chance than those in less established areas.

- Additional Costs and Documentation

Buying commercial property also comes with higher upfront costs compared to residential properties. Borrowers should budget for:

- Valuation and legal fees

- Fire insurance (compulsory)

- Processing or setup fees (commonly RM200–RM500)

- Possible maintenance or service charges for strata-titled buildings

In addition, documentation for Sdn. Bhd. companies or partnerships tend to be more extensive than for individual buyers, as banks need proof of business viability and governance.

- Loan Purpose

A home loan helps you purchase a place to live. A commercial loan, on the other hand, funds a property meant to generate income or support business operations, for instance, a retail space, factory, or office unit.

Some borrowers use commercial loans to buy properties for rental income, while others purchase premises for their own businesses to avoid long-term leasing costs. Either way, the property’s business use and earning potential play a major role in the bank’s approval process.

Commercial loans come with higher costs and stricter requirements, but also greater flexibility and growth potential. They’re designed for borrowers looking to generate income or expand their businesses, rather than for personal homeownership.

How Commercial Property Loans Work in Malaysia Today

Many buyers feel overwhelmed when applying for a commercial loan because the requirements can seem stricter and more complex than a standard home loan.

Understanding how commercial property loans work today helps you avoid these surprises and prepare your application more confidently.

1. Banks Assess Both You and the Property

Commercial loans are evaluated differently from residential mortgages. Banks assess two main components:

Your financial strength:

- Credit score and repayment behaviour

- Business stability and annual revenue

- Cash flow and existing liabilities

- Company documents (Form 24, Form 49, audited accounts, tax filings)

The property’s potential:

- Location and accessibility

- Demand in the surrounding commercial area

- Rental yield and occupancy potential

- Whether it is a completed unit or under construction

- Title type (freehold, leasehold, mixed-use)

In 2025, many banks will also use enhanced digital credit systems that analyse financial health more accurately to reduce risk.

2. Margin of Financing Depends on Risk and Purpose

Most banks in Malaysia offer financing ranging from 80% to 90% for commercial properties. However, the exact margin depends on:

- Whether the buyer will occupy the property or rent it out

- The borrower’s credit strength

- The building’s condition and age

- The type of property (retail, office, industrial, SoHo/SoVo, land)

Owner-occupied properties generally qualify for higher financing because banks view them as lower-risk assets.

3. Commercial Loans Have Shorter Tenures

While home loans can span up to 35 years, commercial loans typically range from five to 30 years, or until the borrower reaches the age of 70, whichever comes first.

A shorter tenure means higher monthly instalments, so borrowers should plan cash flow carefully, especially if the purchase is for rental investment or business expansion.

4. Interest and Profit Rates Are Higher Than Home Loans

Commercial loans typically come with higher rates because they carry higher risk for banks.

Typical 2026 ranges include:

- Conventional loans: Base Rate (BR) + 0.5% to 1.5%

- Islamic financing: Profit rate between 4.5% and 5.8%, depending on the structure and the bank

Many Malaysian banks now offer flexi and semi-flexi commercial loan packages, allowing prepayments, redraws, or offset accounts to help manage interest costs more effectively.

5. A Wider Range of Properties Qualifies for Commercial Loans

Commercial financing can be used for a variety of property types:

- Shop lots and shop offices

- Office suites and corporate units

- Retail units in mixed-use developments

- Factories, warehouses, and industrial spaces

- Commercial and industrial land

- Certain SoHo, SoVo, and SoFo units (based on bank policy)

This flexibility allows investors and SMEs to scale their operations without relying solely on business loans.

6. Fire Insurance Is Compulsory

Unlike residential loans, fire insurance is mandatory when financing commercial property. Some banks also include optional coverage such as Mortgage Reducing Term Assurance (MRTA) or Mortgage Level Term Assurance (MLTA).

Borrowers should review the cost of these add-ons, as they contribute to the overall investment cost.

7. More Digital Tools and Faster Applications in 2026

Banks in Malaysia have streamlined their approval processes with digital submissions, online income verification, and automated valuation reports. This has reduced waiting times; however, complex cases, such as financing for older commercial buildings or mixed-use properties, may still require longer processing times.

Commercial property loans in Malaysia today are more accessible, more flexible, and supported by better digital systems. However, they still require solid financial preparation, strong documentation, and a clear understanding of how banks assess both the borrower and the property.

When you know how these loans work, it becomes much easier to plan your investment strategy and secure financing with confidence.

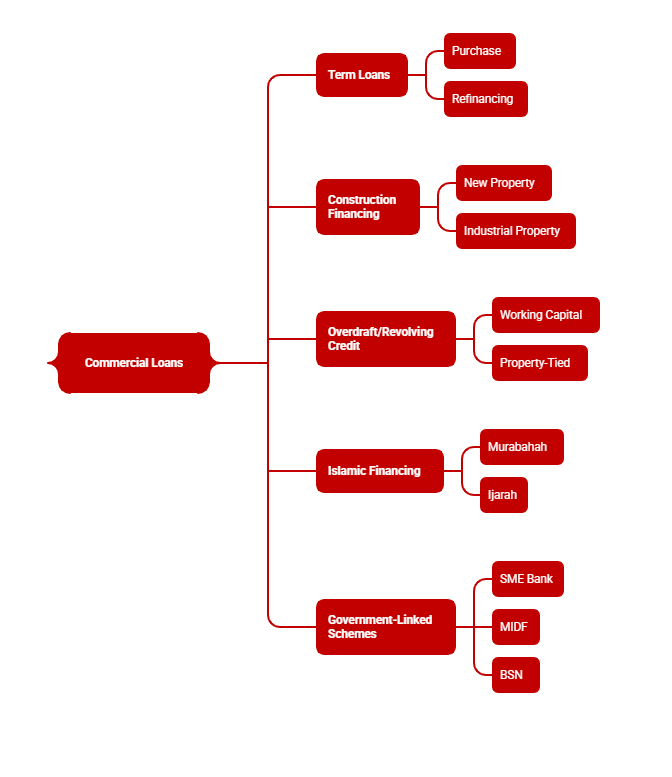

What Are The Types Of Commercial Loans Available?

Commercial buyers in Malaysia have several financing options to choose from, depending on their goals, cash flow, and the type of property they plan to purchase. Understanding the main loan types helps you select the structure that best supports your business or investment strategy.

1. Term Loans

A term loan is the most common financing option for commercial properties. It is used to purchase or refinance completed properties, such as shop lots, offices, and industrial units. Borrowers repay the loan through fixed or variable monthly instalments over a set tenure, usually between five and 30 years.

This option suits buyers with stable cash flow who want predictable repayments.

2. Construction Financing

Construction financing supports borrowers who are building a new commercial or industrial property, such as a warehouse, factory, or customised office facility.

Funds are released progressively based on construction stages, similar to progressive payments in residential developments. Because the risk is higher, banks often require stronger financial documentation, higher equity contributions, or additional guarantees to mitigate the risk.

3. Overdraft or Revolving Credit Facilities

These facilities provide flexible working capital tied to the property or business operations. Instead of fixed monthly instalments, borrowers can draw funds as needed up to an approved limit and only pay interest on the amount used.

This option is ideal for SMEs managing fluctuating cash flow, seasonal revenue, or urgent short-term expenses.

4. Islamic Financing Options

Many Malaysian banks offer Shariah-compliant commercial financing based on concepts such as:

- Murabahah: Cost-plus sale, where the bank purchases the property and sells it to the borrower at a marked-up price.

- Ijarah: A Leasing structure where the bank owns the property and leases it to the borrower for a fixed period.

Islamic banking loans often include flexible payment features and competitive profit rates, making them a popular choice among SMEs and investors.

5. Government-Linked Financing Schemes

Several Government-backed institutions offer financing assistance to SMEs and entrepreneurs, particularly those purchasing commercial or industrial properties. Examples include:

- SME Bank: Facilities for business expansion and property acquisition.

- MIDF: Soft loans for industrial development and automation.

- BSN SME Financing: Suitable for micro and small businesses seeking more accessible terms.

These schemes typically offer lower profit rates, longer tenures, or relaxed collateral requirements, depending on the programme.

How To Apply For a Commercial Property Loan (Step-by-Step)

Applying for a commercial loan can feel intimidating, especially if it’s your first time dealing with business-related financing. The process is more detailed than a residential loan, but breaking it down into clear steps can help you prepare with confidence and avoid unnecessary delays.

Here is a simple, step-by-step guide to follow.

Step 1: Define Your Objective

Before speaking to any bank, be clear about why you want to purchase the commercial property.

Are you buying it for your own business or as an investment for rental income?

Are you buying it for your own business or as an investment for rental income?

Your purpose affects the bank’s assessment because owner-occupied properties are generally considered lower risk. This may lead to better financing terms, including a higher margin or more flexible repayment options.

Step 2: Review Your Financial Health

Banks assess both your personal and business financial strength. Prepare the basics early to avoid document requests later.

For individuals, this includes:

- Proof of income

- Bank statements

- Tax filings

- Credit history

For companies or partnerships, documents include:

- Form 24 and Form 49

- Business registration documents

- Latest audited accounts

- Management accounts

- Company bank statements

Strong cash flow, a clean credit record, and consistent revenue significantly improve approval chances.

Step 3: Compare Loan Packages Across Banks

Different banks offer different commercial loan structures, so comparing your options is essential. Look for:

- Interest or profit rate

- Margin of financing

- Loan tenure

- Flexi or redraw features

- Lock-in period

- Fees and insurance requirements

In 2025, many banks will also offer digital pre-assessment tools, which help you estimate your eligibility before submitting a full application.

Step 4: Confirm Property Eligibility

Not all commercial properties are financed equally. Before committing to a purchase, check:

- Whether the property type is within the bank’s approved list

- Remaining lease tenure (for leasehold properties)

- Location, accessibility, and tenancy potential

- Whether it sits within a mixed-use development

Some lenders are more cautious with older commercial buildings or strata-titled units with limited business demand.

Step 5: Prepare and Submit Your Application

Once you’ve selected a bank, compile all required documents and submit your application. Missing or outdated files are one of the most common causes of approval delays.

During this stage, the bank will:

- Review your personal and business documents

- Conduct a credit check.

- Perform a valuation of the property.

- Assess tenancy income (if applicable)

Approval typically takes between one and two weeks, depending on case complexity.

Step 6: Review the Letter of Offer

If your loan is approved, the bank will issue a Letter of Offer outlining all key terms. Review it carefully before signing.

Important items to check include:

- Loan amount

- Tenure and repayment schedule

- Interest or profit rate

- Fire insurance requirements

- Early settlement penalties

- Monthly service or flexi fees

Do not hesitate to ask questions. A commercial loan is a long-term commitment, and clarity at this stage avoids problems later.

Step 7: Loan Agreement, Disbursement, and Repayment

Once the Letter of Offer is accepted, your lawyer will prepare the loan agreement. After signing, the bank will arrange disbursement to the seller or developer.

Repayment usually begins immediately after disbursement. If your loan is a flexi or semi-flexi plan, consider making periodic prepayments to reduce your outstanding balance and long-term financing cost.

Check Your Commercial Loan Eligibility Before You Buy

Estimate how much you can borrow and understand your financing limits with our easy-to-use calculator.

Common Pitfalls To Avoid When Applying for Commercial Loans

Even financially strong buyers can face hurdles when applying for a commercial property loan. Many of these issues can be avoided with the right preparation. Here are some of the most common mistakes to watch out for.

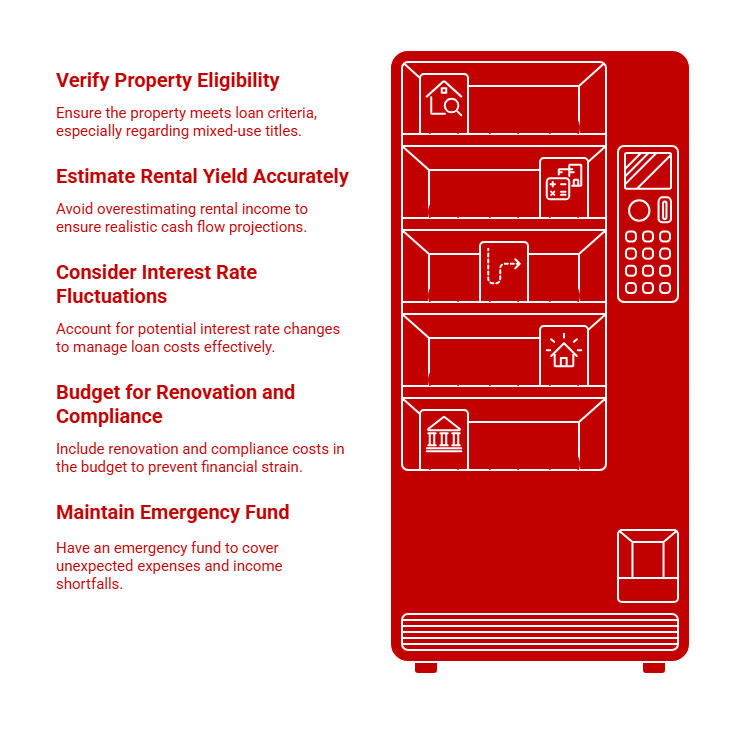

1. Not Checking Whether the Property Is Eligible

Banks have stricter requirements for certain commercial properties. Units in older buildings, mixed-use developments, or strata-titled shop lots may face tighter evaluations.

Some banks also restrict financing for upper-floor retail units or properties with low occupancy rates. Always confirm financing eligibility before committing to a purchase.

2. Overestimating Rental Income or Business Revenue

Many buyers assume that rental income or future business growth will comfortably cover their loan instalments.

In reality, commercial properties can experience longer vacancy periods and more volatile rental demand than residential units. Build a realistic cash flow plan and ensure you have a buffer for slow months.

3. Forgetting About Additional Upfront and Ongoing Costs

Commercial loans come with more fees than standard home loans. These include valuation costs, legal fees, fire insurance, maintenance charges, and renovation costs. For larger units, these expenses can be substantial.

Failing to budget for these costs can stretch your finances in the early months.

4. Not Preparing Complete and Accurate Documentation

Missing or outdated documents are one of the top reasons for delayed approvals. Banks need full visibility of your personal financial health and, if applicable, your company’s performance.

Incomplete audit reports, inconsistent bank statements, or missing Forms 24 and 49 can slow down the entire process.

5. Ignoring Interest Rate Fluctuations

Commercial loans often come with floating interest or profit rates. While this can work in your favour during stable economic periods, it also means your monthly instalments may increase when rates rise.

Plan your budget with potential fluctuations in mind.

6. Rushing Into a Loan Without Comparing Packages

Loan structures vary significantly across banks, especially for commercial properties. Some lenders offer higher margins, while others provide flexible redraw features or lower profit rates for owner-occupied units.

Comparing options can save you thousands of ringgit over the loan’s lifetime.

7. Using the Wrong Loan Type for Your Needs

Some buyers use term loans when they actually need revolving credit for business operations, while others take overdrafts for long-term property financing. Choosing the wrong facility can lead to higher costs or limited flexibility.

Understanding your financial goals helps you pick the right structure.

By avoiding these common pitfalls, you increase your chances of securing a smooth approval process and ensuring your commercial investment remains financially sustainable in the long run.

How Can You Prepare for Your Commercial Loan Application?

Securing a commercial property loan may feel overwhelming at first, but with the right preparation, clear financial planning, and a good understanding of bank requirements, the process becomes much more manageable.

If you are planning to finance a commercial property soon, start reviewing your financial health and exploring your eligibility with various banks. Early preparation helps you avoid delays and ensures you secure the best possible terms for your investment.

For more insights on loans, financing tips, and property investment guides, visit the PropertyGuru Guides section.

Still exploring commercial units? Head over to PropertyGuru to browse the latest listings for sale across Malaysia.

Keep Track of New Launches

Visit our new launches page to find the new launch project of your dreams and submit an enquiry today.

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.