Landlord insurance is no longer an optional extra in Malaysia’s rental market. With rising tenancy disputes, increased repair costs, stricter tenancy expectations, and the growth of digital tenancy platforms, landlords in 2026 face more financial risks than ever before.

A standard tenancy agreement can only protect you on paper, but when something goes wrong, you need a policy that actually compensates you.

This guide breaks down exactly what landlord insurance covers, why it matters, and how it protects Malaysian landlords from losses that ordinary home insurance typically does not. It takes the original PropertyGuru intent, "why you should get landlord insurance", and widens it into a modern, practical, highly relevant 2026.

Discover Rental Options Across Malaysia

See Homes That Match Your Budget

What Is Landlord Insurance?

A standard homeowner or household policy primarily protects the physical structure and contents of a home. Landlord insurance, on the other hand, is designed to address the broader, more complex risks that arise only when a property is rented to tenants.

These risks extend far beyond accidental damage or fire. They include financial exposures, legal complications, and scenarios where a landlord’s income or asset security may be disrupted.

For this reason, landlord insurance has become an increasingly important part of responsible property management in Malaysia.

A typical landlord insurance policy may offer protection for:

- Loss of Rental Income: Compensation if the unit becomes temporarily uninhabitable due to insured damage.

- Rent Default: Cover for tenants who fail to pay rent, often subject to specific conditions or time limits.

- Damage Caused by Tenants: Including accidental, negligent, or malicious damage to fixtures, fittings, and furnishings.

- Theft by Occupants: Coverage varies; some insurers require proof of forced entry for tenant-related theft claims.

- Legal Expenses: Protection for lawyer fees, filing costs, termination proceedings, and other tenant-related legal matters.

- Landlord Liability: Covers situations in which someone is injured inside the rented unit, and the landlord is held responsible.

- Emergency Repairs: Reimbursement or assistance for urgent issues such as burst pipes or electrical faults.

- Forced Eviction-Related Losses: Support for certain costs incurred during eviction or subsequent vacancy.

Some insurers now offer protection for smart-home equipment, with products such as the Allianz Smart Home add-on. However, short-term rental cover for platforms like Airbnb remains limited, and vacancy protection for periods between tenants is not yet widely available.

These additions signal a gradual move towards more comprehensive landlord-focused products, though careful policy comparison remains essential.

Why Standard Home Insurance Isn’t Enough

Landlord insurance is a specialised form of insurance designed for property owners who lease residential or commercial units.

They include financial exposures, legal complications, and scenarios where a landlord’s income or asset security may be disrupted.

For this reason, landlord insurance has become an increasingly important part of responsible property management in Malaysia.

A typical landlord insurance policy may offer protection for:

- Loss of Rental Income: Compensation if the unit becomes temporarily uninhabitable due to insured damage.

- Rent Default: Cover for tenants who fail to pay rent, often subject to specific conditions or time limits.

- Damage Caused by Tenants: Including accidental, negligent, or malicious damage to fixtures, fittings, and furnishings.

- Theft by Occupants: Coverage varies; some insurers require proof of forced entry for tenant-related theft claims.

- Legal Expenses: Protection for lawyer fees, filing costs, termination proceedings, and other tenant-related legal matters.

- Landlord Liability: Covers situations in which someone is injured inside the rented unit, and the landlord is held responsible.

- Emergency Repairs: Reimbursement or assistance for urgent issues such as burst pipes or electrical faults.

- Forced Eviction-Related Losses: Support for certain costs incurred during eviction or subsequent vacancy.

As of 2025, Malaysian insurers have begun expanding their offerings to reflect modern tenant behaviour and evolving property needs.

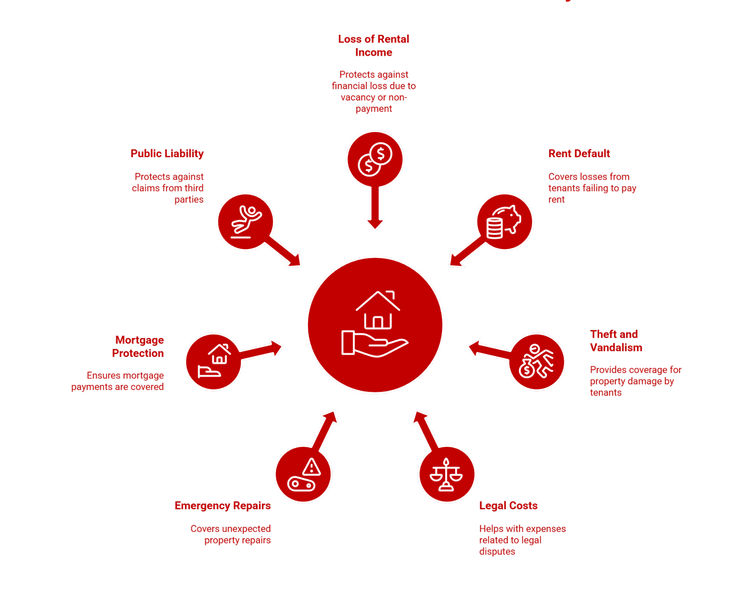

The 7 Critical Reasons Every Landlord Needs Insurance in 2026

Before committing to a tenancy agreement or handing over your keys, it is worth understanding the core protections that safeguard your rental investment.

The following seven pillars explain exactly why landlord insurance has become essential for every Malaysian landlord:

1. Protection Against Loss of Rental Income

Loss of rent is one of the most damaging scenarios for a landlord, especially if the unit is tied to a monthly mortgage.

Insurers typically cover rental income loss under these circumstances:

a) Property damage that makes the unit unlivable

Examples include:

- Flooding from burst pipes

- Short-circuit-related electrical fires

- Severe storm damage

- Ceiling collapse or structural faults

If the tenant must move out during repairs, landlord insurance compensates you for the lost rent, usually up to a fixed number of months.

b) Government-mandated unoccupancy

In certain strata or township cases, authorities may temporarily restrict occupancy due to safety concerns.

Standard home insurance does not cover this; landlord insurance does.

2. Rent Default (Including Runaway Tenants)

Tenancy default remains one of the most frequent, and often most financially damaging, risks a landlord can face.

Scenarios often covered under landlord insurance include:

- Tenant refuses to pay rent

- Tenant disappears ("runaway tenant")

- Tenant breaks the tenancy agreement without notice

- Tenant remains in the property without paying ("holdover tenant")

Some policies reimburse:

- Unpaid Rent Reimbursement: Many landlord insurance policies cover rental arrears for 3 to 6 months, providing crucial cash flow stability when tenants default.

- Reimbursement Caps and Conditions: Some insurers impose tighter limits, capping repayments at two to three months or requiring formal proof of eviction proceedings before approving a claim.

- Legal Fee Coverage: Policies often cover legal costs incurred during eviction, easing the financial burden of resolving tenant disputes.

- Forced Vacancy Protection: Certain plans cover losses arising from property vacancy due to tenant eviction or non-payment, helping landlords stay financially afloat during transition periods.

With rental arrears rising sharply across major Malaysian cities, especially Kuala Lumpur, Shah Alam, Penang, and Johor Bahru, this protection has become indispensable for landlords.

3. Theft, Vandalism, and Malicious Damage by Tenants

This is one of the most underestimated risks for Malaysian landlords, especially in furnished or partially furnished units.

While landlord insurance does provide protection, the scope of coverage varies by insurer. In particular, "theft by tenant" may not be covered unless there is clear evidence of forced entry or criminal intent.

Therefore, understanding the fine print is crucial.

Most policies typically cover:

- Theft of Appliances: Such as refrigerators, washing machines, ovens, and other fixed or semi-fixed items provided by the landlord.

- Theft of Loose Furniture: Including sofas, dining sets, mattresses, and other movable furnishings, subject to policy conditions.

- Deliberate Removal of Fittings: For example, light fixtures, built-in shelves, and bathroom accessories are intentionally removed.

- Intentional or Malicious Damage: Damage caused on purpose by tenants, including broken doors, smashed windows, or vandalised fixtures.

- Party-Related Destruction: Damages arising from unauthorised gatherings, noise complaints, or overcrowding incidents.

- Severe Child-Related Accidental Damage: Accidents that result in substantial harm to floors, walls, or built-in cabinetry.

- Graffiti and Vandalism: Marks, scratches, or defacement requiring professional repainting or surface treatment.

Without this layer of protection, landlords in Malaysia routinely face repair costs of RM5,000 to RM20,000 before the unit can be made tenant-ready again, a cost that can significantly delay rental income recovery.

4. Coverage for Legal Costs

Legal disputes between tenants and landlords have increased significantly due to:

- Inflation-driven rental pressure

- Unpaid rent

- Breaches of tenancy agreements

- Misuse of property

- Illegal subletting

A single legal demand letter or eviction process can already cost a landlord RM500 to RM5,000.

Landlord insurance typically provides essential legal support through both standard legal-expense extensions and more advanced coverage options.

Depending on the policy tier, landlords may be protected against a range of legal costs, including:

- Lawyer Fees: Coverage for professional representation during disputes, negotiations, or court proceedings.

- Filing and Administrative Fees: Reimbursement for the costs of submitting legal documents, including court filings and statutory notices.

- Demand Letter Costs: Protection for the expenses involved in issuing formal demand letters to tenants in breach.

- Tenancy Termination Proceedings: Coverage for legal steps taken to terminate a tenancy due to non-payment, damage, or contractual violations.

- Claims Brought Against Tenants: Support for pursuing claims related to property damage, arrears, or breach of agreement.

This remains one of the most underestimated yet consistently valuable components of landlord insurance, offering reassurance and practical protection when disputes escalate.

5. Emergency Repairs and Building Damage

Sometimes the issue lies not with the tenant but with the property itself, where underlying defects or maintenance lapses can trigger unexpected disputes, disruptions, or repair costs.

Landlord insurance often includes cost coverage for:

- Burst water pipes

- Faulty wiring

- Broken windows

- Break-ins

- Roof leaks

- Collapsed plaster ceilings

- Electrical system failures

- Most policies also allow claims for:

- Emergency locksmith services

- Plumbing replacements

- Temporary repairs to secure the property

With construction material and labour costs rising sharply in Malaysia, emergency repair protection is now a major must-have.

6. Mortgage Instalment Protection

Some insurers offer a unique protection that mirrors personal accident insurance.

If the property becomes unlivable due to insured damage, for example, a significant fire or structural collapse, landlord insurance may cover:

- Up to 6 months of mortgage instalments in rare cases

Or

- A fixed payout benefit

This helps keep the landlord afloat financially while repairs are underway.

7. Public Liability Coverage

Public liability is widely regarded as one of the most essential components of landlord insurance, as it protects you when unexpected incidents occur within your rental property.

While many landlords focus on rent loss or tenant damage, liability risks can be far more financially damaging if left uninsured.

Who Can Make a Claim Against You?

If someone is injured or suffers a loss inside your rental unit, you, as the property owner, may be held legally responsible.

This applies not only to the tenant but also to anyone entering the premises, including:

- Tenants and their family members

- Guests or visitors

- Delivery riders or couriers

- Maintenance teams, contractors, or cleaners

Common Liability Scenarios

Claims can arise from a wide range of everyday hazards, such as:

- Slips and falls inside the unit

- Injuries caused by broken fixtures or fittings

- Harm resulting from electrical faults

- Accidents linked to structural defects

- Loss or damage to valuables caused by property-related hazards

Any of these situations can lead to legal action, medical claims, or compensation demands.

What Public Liability Insurance Covers?

A landlord insurance policy helps shield you from the financial consequences of such incidents by covering:

- Compensation payouts awarded to affected individuals

- Medical cost reimbursements if the injured party requires treatment

- Legal defence fees, should the case escalate into a lawsuit

Most Malaysian landlord policies offer liability protection ranging from RM100,000 to RM1 million, depending on the insurer and the selected plan.

Taken together, these seven protections form a comprehensive safety net that shields your investment from financial shocks, tenant risks, and unforeseen property issues, ensuring your rental business remains stable, resilient, and confidently managed in 2026 and beyond.

Calculate Your Monthly Home Loan Costs

Know Your Financing Range Before You Decide

Why Landlord Insurance Has Become Even More Important?

As Malaysia’s rental market evolves, landlords today face a broader set of risks than ever before.

Understanding these shifts helps you see why comprehensive coverage is no longer optional:

- Higher rental disputes

Post-pandemic pressures and inflation have pushed arrears upwards, particularly in urban rental markets. - Rapid growth in fully furnished units

More landlords now offer furnished apartments, which increases exposure to theft, damage, and wear and tear. - Expansion of short-term rentals (Airbnb, Booking, Agoda Homes)

Faster tenant turnover means higher risk profiles, more claims, and greater liability exposure. - Rising renovation and repair costs

Labour and material prices have risen by 20-30% since 2022, making out-of-pocket repairs far more expensive. - Smart-home adoption

Modern homes now commonly include:- Smart locks

- CCTV and Wi-Fi surveillance

- IoT appliances

- Smart locks

These assets often require additional or specialised coverage.

- Increase in digital tenancy agreements

While digital contracts are convenient, they cannot enforce payment; therefore, insurance becomes the practical safeguard when disputes arise.

In a landscape where risks are multiplying and costs continue to climb, landlord insurance stands as one of the few protections that keep your rental investment secure, stable, and future-ready.

What Landlord Insurance Does Not Cover?

For clarity and realistic expectations, here are the exclusions commonly found in Malaysian landlord policies:

- General wear and tear

- Damage caused by pets (unless explicitly covered)

- Loss of rental income due to voluntary vacancy

- Illegal activities conducted by the landlord

- Intentional damage caused by the landlord

- Flooding in areas excluded by the policy

- Renovations not approved by the insurer.

Since insurers apply different terms, it is essential to review the policy wording carefully to understand your exact protections and exclusions.

How Much Does Landlord Insurance Cost in Malaysia?

To provide landlords with a clearer understanding of what to expect in 2026, here’s a breakdown of the typical annual premiums across various property types and rental setups.

Average range for residential landlord policies:

| Type of Unit | Estimated Annual Premium |

| Condo/Apartment | RM250 – RM600 |

| Terrace/Semi-D | RM350 – RM900 |

| Fully Furnished Unit | RM500 – RM1,200 |

| Luxury High-Rise | RM800 – RM1,600 |

| Short-Term Rental (Airbnb) | RM600 – RM2,000 |

Factors affecting premium:

- Type of building

- Location (KL, PJ, Penang, JB = higher risk)

- Furnishing level

- Rental income level

- Security features

- Claim history

With premiums remaining relatively affordable compared to the risks they offset, landlord insurance has become one of the most practical and high-value safeguards for Malaysian property owners, protecting cash flow, preserving assets, and ensuring peace of mind throughout every tenancy cycle.

How to Choose the Right Landlord Insurance?

Use this checklist to assess whether a plan truly meets the needs of a modern Malaysian landlord. Before committing to any policy, it helps to evaluate the essentials systematically.

Checklist:

- Check rental loss limits: Some policies only cover 1-2 months of rent. Others, 6 months.

- Confirm coverage for runaway tenants: This is not included in every policy.

- Look for public liability: At least RM300,000

- Ensure that theft by tenant is included, as many basic policies exclude this coverage.

- Consider smart-home coverage, especially for newer KL and PJ apartments.

- Evaluate excess (deductible) amounts

- Review exclusions carefully

By carefully selecting your policy and understanding where coverage differs, you ensure that your rental investment remains protected not only from day-to-day risks but also from the unexpected challenges that can quickly disrupt cash flow and long-term returns.

Do Malaysian Landlords Really Need Landlord Insurance?

In short: yes, in 2026, more than ever.

Tenancy agreements provide rules, but insurance provides compensation in the event of unforeseen circumstances.

Without landlord insurance, you risk:

- Thousands of ringgit in unpaid rent

- Expensive repairs

- Long vacancy periods

- Costly legal battles

- Liability lawsuits

The small annual premium is a fraction of the cost of a single major tenancy incident.

Looking to Rent Out Your Property?

Rising repair costs, more complex tenancy behaviours, and the growing prevalence of furnished units mean landlords today face risks that simply did not exist a decade ago.

With the right insurance in place, your rental investment becomes more resilient, more predictable, and far better equipped to weather the unexpected.

Looking to rent out your property? Explore our PropertyGuru Malaysia guide to understand the risks, rising costs, and protections every landlord should have.

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.