Owning a home is a milestone many dream of, and with it comes one of the most significant financial commitments of all, a housing loan. The prospect of settling that loan early can be deeply appealing: the freedom from monthly repayments, the satisfaction of being debt-free, and the potential to save thousands in interest.

Yet, behind that sense of achievement lies an important question: Is early settlement truly the most strategic move for you?

That’s where an early settlement housing loan calculator proves its worth. It provides a clear picture of potential savings, highlights the financial trade-offs, and helps you determine whether paying off your loan early aligns with your long-term goals.

In this guide, we unpack how the calculator works, outline recent changes in bank policies and fees, and share practical insights to help you plan your repayment with confidence.

| Table of Contents 1. Why Consider Early Settlement of a Housing Loan? 2. What Does an Early Settlement Housing Loan Calculator Do? 3. Latest Developments in Early Settlement Fees and Banking Rules for 2026 4. Understanding Early Settlement Charges and Lock-In Periods 5. How to Use the Calculator: Step-by-Step 6. Pros and Cons of Early Settlement (with Calculator Scenarios) 7. Practical Tips for Making the Decision 8. Should You Use an Early Settlement Housing Loan Calculator in 2026? |

Explore rental homes across Malaysia.

To find units that match your budget

Why Consider Early Settlement of a Housing Loan?

For most Malaysians, buying a home is one of the most significant financial commitments of their lives. Once the loan is secured and repayments begin, many start wondering, Should I pay it off early if I’m able to?

The idea certainly has its appeal. Early settlement can unlock several tangible benefits, such as:

- Freeing Up Cash Flow: Once your loan is cleared, you’ll no longer have to make monthly instalments, giving you extra financial breathing room each month.

- Saving on Interest: The earlier you repay your loan, the less interest you’ll pay overall, potentially saving tens of thousands of ringgit across the loan’s lifespan.

- Reducing Financial Stress: Being debt-free lowers financial pressure, especially during uncertain economic periods or if your income fluctuates.

- Greater Flexibility Later in Life: Entering retirement without a mortgage gives you more freedom to manage your lifestyle and future expenses with ease.

However, settling early isn’t always the best option for everyone. In some cases, your extra funds might earn better returns if invested elsewhere, or your bank may impose early settlement penalties that offset the potential savings.

That’s why using an early-settlement housing loan calculator is so helpful; it helps you weigh the pros and cons, showing exactly how much you could save and what costs you might incur before making your decision.

What does an Early Settlement Housing Loan Calculator do?

A calculator designed for early settlement allows you to model how your outstanding loan balance, remaining interest cost, and the effect of early payment change if you pay more than required or settle completely ahead of schedule.

It typically factors in:

- Remaining principal balance.

- Remaining tenure.

- Interest or profit rate.

- Bank charges for early settlement.

- Any rebates or savings from the bank’s interest/profit schedule.

For example, some banks allow prepayments or top-ups to reduce outstanding balances and interest costs, as HSBC Bank Malaysia mentions in its HomeSmart-i product, which helps early settlement with one month’s notice.

On the calculator front, the PropertyGuru Malaysia homepage features its home loan calculator, which provides monthly repayment estimates. You can pair this with early settlement calculations for a more comprehensive picture.

By using both, you can compare the benefits of continuing with scheduled payments versus paying off early.

Latest Developments in Early Settlement Fees and Banking Rules for 2026

Before you plug in numbers, you should be aware of the latest rules, fees, and bank offerings that affect early settlement decisions:

- In March 2025, AmBank (M) Berhad announced that the 2% early settlement fee/charge for housing loans and property loans/financing-i products within the lock-in period would not be imposed until further notice.

- In August 2025, Alliance Bank Malaysia Berhad announced that, effective August 1, 2025, the early settlement fee (for loan settlement within the lock-in period) of 2% would be discontinued.

- In March 2025, CIMB Bank Berhad announced that, effective 23 March 2025, the early settlement charges for property financing would be ceased.

These changes mean that for many borrowers in 2026, the barrier of early settlement fees is lower than in past years, making early settlement and calculator modelling more relevant.

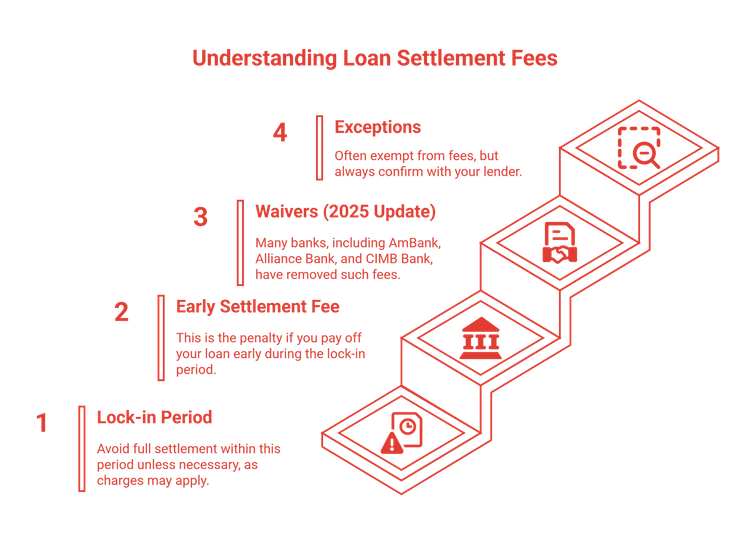

Understanding Early Settlement Charges and Lock-In Periods

Before using an early-settlement housing loan calculator, it’s essential to know how lock-in periods and early settlement charges work, as these can make a big difference to your final savings.

Most Malaysian home loans come with a lock-in period of three to five years from the date the loan is disbursed. If you decide to settle or refinance your loan fully during this time, the bank may impose an early settlement fee.

This fee helps the bank recover part of its administrative costs and the profit it would have earned over the remaining loan tenure.

Here’s a quick look at how this typically works:

This shift towards more borrower-friendly policies in 2025 reflects the increased competitiveness of the housing loan market.

When using a calculator, try running two versions of your repayment plan: one assuming an early settlement during the lock-in period (where a fee may apply) and another after the lock-in ends. Comparing the two helps you understand whether it’s smarter to settle now or wait a little longer for greater savings.

How To Use the Calculator: Step-by-Step

Here’s a walkthrough you can follow to model early settlement and compare options:

Step 1: Gather your loan details

- Loan amount

- Current outstanding principal

- Interest or profit rate (annual)

- Remaining tenure (years or months)

- Monthly instalment amount

Step 2: Use a basic home loan repayment calculator (for example, PropertyGuru Malaysia’s Home Loan Calculator) to determine the baseline monthly cost and the remaining payment schedule.

Step 3: Adjust for the early settlement scenario

- Input the remaining balance and change "remaining tenure" to zero (or make a lump pre-payment).

- Include any applicable early settlement fee or rebate (as per your bank’s terms).

- The calculator will show "total interest saved" and "total amount paid" if you settle now, compared with continuing scheduled payments.

Step 4: Compare results

- Scheduled route: monthly instalment × remaining years + total interest.

- Early settlement route: Lump sum now + any fees – interest saved.

Step 5: Interpret the results

- If the savings (interest + fees avoided) are significant and you have the cash, early settlement may be advantageous.

- If you lose flexibility or miss higher-return investment opportunities, you may consider deferring.

By modelling multiple scenarios (e.g., settle now, settle in 2 years, make extra payments), you can get the whole picture.

Pros and Cons of Early Settlement

Before deciding whether to pay off your housing loan early, weigh the potential benefits against the drawbacks.

Here’s a quick look at both sides of the equation:

Pros

- Lower total interest cost.

- Reduced debt burden and improved cash flow.

- Enhanced financial resilience.

Cons

- Loss of liquidity: once you use the cash, you may not easily access it for emergencies or opportunity investments.

- If the interest rate is relatively low (or variable) and you can earn a higher rate elsewhere, early settlement may have an opportunity cost.

- Some loan products may include early settlement charges or require notice (though many banks are reducing these).

Ultimately, the right decision depends on your personal goals and financial comfort.

Scenario Example

Before diving into the numbers, note that the following figures are purely illustrative and intended to demonstrate how early settlement savings can work in practice; they do not represent actual user data or official calculations.

Let’s say you have:

- Outstanding principal: RM 400,000

- Annual rate: 4.5%

- Remaining tenure: 15 years

- Monthly instalment: RM 3,054 (for illustration)

Option A: Continue payments for 15 years → total paid RM 549,720 (principal + interest)

Option B: Use a calculator to model paying off now (assuming no fee) → you pay RM 400,000 + notice fee of maybe RM 0 → you save RM 149,720 in interest.

In 2025, with lower early settlement fees, the savings may be enhanced.

The early settlement calculator helps you test different payoff amounts (full or partial) and timing.

While these examples are simplified, they illustrate how a slight adjustment in timing or repayment can translate into substantial long-term savings.

Practical Tips for Making the Decision

Before deciding whether to settle your housing loan early, it is helpful to consider the decision from multiple angles: financial, personal, and market-based.

The following points can help you in weighing the benefits and trade-offs more clearly:

- Check whether your loan has a lock-in period and whether early settlement charges apply; many banks have reduced or ceased these fees since 2025.

- Ensure you still have an emergency fund and are not tying up all your cash in paying off the home, especially when other financial needs arise.

- Consider whether paying extra (but not fully settling) strikes a good balance between savings and flexibility.

- Factor in your age, career prospects, other debts, and investment goals. If retirement is near, being debt-free may be valuable.

- Use the calculator frequently as you approach milestone years (for example, annually or when the rate resets).

- Revisit your property goals: if you plan to sell or refinance, consider whether settling early could limit your future gains. Review current market listings to gauge potential sale prices and the transaction timeline.

- Regularly review the interest rate and profit rate environment. In a rising rate scenario, you may benefit more from reducing principal early.

- Discuss with your bank how they handle pre-payments, early settlements, and whether any rebates are applicable (for example, some banks may offer rebates on "unearned profit" for Islamic financing).

Ultimately, the decision comes down to striking the right balance between peace of mind and financial efficiency.

Should You Use an Early Settlement Housing Loan Calculator in 2026?

Using an early settlement housing loan calculator in Malaysia for 2026 is a smart way to understand your options. Whether you settle your loan early, make extra payments, or simply stay the course.

By modelling the numbers, you can clearly see the savings, costs, and trade-offs. With many banks reducing early settlement fees since 2025, the decision becomes even more timely.

On PropertyGuru Malaysia, we offer not only the calculator but also up-to-date guides, listings tools, and expert perspectives to help you plan your loan, your property strategy, and your financial future. Explore the latest listings, current home-loan offers, and tap into our insights to decide whether early settlement is proper for you.

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.