Owning a property is one of the more popular items on most people’s bucket lists but unfortunately, the chances of ACTUALLY buying one seems to be a faraway dream these days.

And the main cause of it all? The shocking number of home loans that were rejected last year: a whopping 60%! But, why is it so difficult to get a home loan approved?

This is when we decided to find out by getting in touch with a few Malaysians who’ve had their application rejected last year, so they can share their experiences with the rest of our readers. Without further ado, let’s get down to business!

Reason #1: Having an unstable income and non-existent credit score

- Faris, 24, Front of House Supervisor

It had always been his dream to own a property, and he knew how to be frugal with his expenditures.

He even stuck with his old motorbike to commute, even though he could afford a new car. At last, he found the perfect home under RM250,000 and quickly made an offer.

However, even though he’s more than capable of paying the 10% down payment, his home loan application was rejected, and he could only watch as the house was sold off.

The bank explained that his basic salary was too low even though his overall monthly income was sufficient for the loan.

“My salary is around RM3,700 per month. However, as with many in the hospitality industry, our basic salary is much lower than that as we implement the service point system.”

What this means is that:

- His monthly salary fluctuates according to his hotel’s revenue each month.

- The only constant is his basic salary which, at the time, was only RM1,000.

- Banks do not see the service point system as an additional fixed monthly allowance.

- Thus, he’s categorised as having an unstable income and needs to put a higher down payment for the application to go through.

Furthermore, the bank also clarified that he had no credit score history. Having no credit card, car loan or even a student loan in the past, the bank explained that there was no repayment trend that they could refer to in order to justify the loan.

“It’s really ironic that my overly cautious financial habits actually contributed to my home loan being rejected when I did it to save up for the house in the first place.”

Not deterred, Faris recently accepted a better offer at another hotel after making sure that they provided a higher basic pay.

He has found another house listing on PropertyGuru now. Hopefully, he won’t be disappointed a second time!

Reason #2: The seller or developer has been blacklisted

- Vanessa, 28, Video Producer

Renting a house with her husband for the past 2 years, she finally felt like last year was the right time to own a place of their own.

They found a 2-storey house near Kajang up for sale, and quickly got in touch with the owner. A price was fixed, and a pre-agreement was made.

With a combined monthly household income of RM15,000, their financial record is superb. However, their home loan still got rejected.

The reason? The owner of the house was bankrupt, and had recently been blacklisted by the Credit Tip-Off Service (CTOS).

“We were really lucky as we only entered into a pre-agreement and did not sign a Sale and Purchase Agreement (SPA)!”

As per Malaysian law, anyone who is declared bankrupt is barred from making any deals or transactions regarding their properties. Other points to note:

- It’s also illegal for them to enter into a Sale and Purchase Agreement (SPA) without prior consent from the Insolvency Department.

- However, this also depends on the number of assets he/she has in comparison to the current liabilities.

That’s why it’s very important to do a thorough background check on the seller and/or developers before entering into an agreement.

“Good thing we never gave any down payment or earnest deposit either to the property owner, or we might have lost a hefty sum of money!”

Reason #3: The bank values the property differently than the seller

- Divinish, 30, Human Resource Manager

He found the perfect home (or so he thought) in Shah Alam, that’s at a prime location and most importantly, near his office. Sadly, he too, faced a home loan rejection due to complications from the property seller’s side.

Although it was a bit pricey, he met the owner and agreed on a price. Well, a sub-sale house in a prime location should be worth it in the long term even if it’s a little overpriced, right? The bank didn’t share his opinion though.

“When I went to the bank to finance the purchase, they valued it much lower than I expected; RM50,000 lower to be exact!”

Each bank would have its own property valuation expert(s), and none of the banks he enquired with would justify the financing amount that he was asking for the house.

Divinish was left with the options of either forking out a substantially larger down payment or negotiate a lower price with the seller.

“The seller would not budge from her initial asking price and after much deliberation, I didn’t think that it was worth it to fork out such a large sum for just a down payment.”

Reason #4: A Debt Service Ratio (DSR) score that is too high

- Chloe, 32, Marketing Senior Executive

With a salary upwards of RM4,000, she was pretty confident in her chances of having her home loan approved.

After all, it was only a 3-bedroom apartment on the outskirts of Kuala Lumpur that was well within her budget.

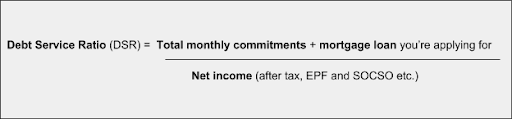

What she didn’t know was that she had a high Debt Service Ratio (DSR), which resulted in her home loan being straightaway dismissed by the bank.

“I was pretty shocked when the bank rejected my application as I always pay my bills and other financial commitments on time.”

However, Chloe later realized that one’s DSR score is unaffected by how prompt your repayments are (that is the credit score), but instead on the amount of monthly commitments you have.

Specifically, the DSR is a method used by the banks to calculate whether or not you can afford the loan you’re applying for, which is of the utmost importance. Here’s the formula used to calculate DSR:

Each bank has its very own DSR evaluation, but you should ideally keep it within the 60% range. Your monthly commitments include bank debts (car loan, credit card bills, and personal loans.) and non-bank debt (PTPTN loan etc).

As for Chloe, her DSR score hovered around the 80% range which is higher than what was allowed by the bank she applied for.

“I never knew my monthly commitments would add up to be that high!”

Well, with PropertyGuru’s Home Loan Calculator, you can actually find out the estimated monthly home loan repayment, based on the loan amount, interest rate and loan tenure you wish to obtain from banks.

Relevant Guides:

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.