The Malaysian property market is in its cycle of market slowdown as of 2019, with an effect of stabilising the property prices.

In lieu of the property market slowdown, new developments are being sold with more attractive packaging, while the subsale market has become a viable option as the properties are being sold at their actual value instead of inflated rates.

Below then begins the first series of the complete set of guides on how to begin purchasing your new property, whether they are subsale, brand new or commercial developments.

Residential – New Development

New developments are among some of the easiest to procure financing for, in lieu of the very competitive market.

There are however a few preliminary steps that buyers have to take before making their purchase. Below begins the guide to purchasing new developments.

Plan Your Budget

The most important thing to first determine is the budget of the buyer. While purchasing a new property may be easier due to the possible discounts provided by the developer, there are other points of consideration before you make that purchase!

Firstly, no one knows your bank account, pockets and finances better than you do.

Even if you have high income, you may not be able to purchase a high end property if you have high commitments, and vice versa. Hence, you have to set a budget that is first within your reach.

- The first step to deciding your budget is to determine how much you can afford monthly. To know exactly how much you are earning, visit this website and key in your gross income with your bonus if it is applicable. The application will automatically calculate your nett income for you.

- The next step is to determine your monthly expenses. From your nett income, deduct all your monthly expenses. While this may be difficult for some who do not keep track of their daily usage, using a monthly calculator to gauge their expenses may be better. There are a lot of free mobile apps available that can help you track your expenses!

- The third step is to determine how much of your disposable income you can actually use to pay for your monthly instalments. Do note that the maximum loan that can be obtained from conventional loans is 90% of the property price tag. Hence if you aim to purchase a property priced at RM500,000, the maximum loan you can obtain for it is only RM450,000.

Once you have determined how much you can afford to pay for your property, the next thing that you will need to know are the fees that you will need to pay for the Legal Fees, Sale and Purchase Agreement, Stamp Duty, and Memorandum of Transfer (MOT)

1) Down payment

The down payment for a new residential property purchase usually varies depending on how much loan the purchaser is able to get from the bank.

So for example, if the bank is willing to loan the buyer 90% of the property price, then the buyer will only need to come out with 10% of the property purchase price.

For Residential titled developments, purchasers are allowed to withdraw money from their EPF Account II to partially pay for their property upfront payments such as the 10% down payment.

The purchaser will however need to pay for the property first before being able to withdraw from EPF, as the government body requires the SPA of the development before they can proceed with the withdrawal process.

2) Sale And Purchase Agreement Fees (a.k.a. SPA, SNP or S&P)

The Sale and Purchase Agreement is the most important document that buyers will have.

These are the proof that the buyers have purchased a property, whereby the contract will contain all the facts and blueprint of the property. The charges for these follow a price tier.

- For The First RM500,000 – 1.0% (Subject to a minimum fee of RM300.00)

- For The Next RM500,000 – 0.80%

- For The Next RM2,000,000 – 0.70%

- For The Next RM2,000,000 – 0.60%

- For The Next RM2,500,000 – 0.50%

3) Loan Agreement Legal Fees

These fees are otherwise known as Lawyer Fees. They are the fees that you pay a lawyer for their time in creating the legal documents.

The fees however follow a standard table, whereby the price of the property determines how much a property purchaser has to pay. Below is the table:

- For The First RM500,000 – 1.0% (Subject to a minimum fee of RM500.00)

- For The Next RM500,000 – 0.80%

- For The Next RM2,000,000 – 0.70%

- For The Next RM2,000,000 – 0.60%

- For The Next RM2,500,000 – 0.50%

The Stamp Duty for the legal fees are government charges when the lawyer submits your documents. They are usually only 0.5% of your loan amount.

Other charges to note are as below:

- Professional Legal Fees to be inclusive of 6% government tax

- Disbursement Fees to range between RM1,000 – RM1,500

4) Stamp Duty On Memorandum Of Transfer (MOT)

The MOT is only paid when the development is completed. These are the fees that the purchaser has to pay for transferring the property from the developer’s name into the owner’s name.

The charges for these fees also follow a table:

- For The First RM100,000 – 1%

- For The Next RM500,000 – 2%

- RM5,000,001 and above – 3%

Other charges to note are as below:

- Professional Legal Fees to be included 6% of government tax

- Disbursement Fees to range between RM1,000 – RM1,500

The advantages of purchasing a property from the developers themselves is that buyers may be able to get various types of freebies (depending on the developer) such as:

- Free Legal Fees

- Free Stamp Duty

- Rebate

- Free down payment

There are however other costs that property buyers will need to anticipate into when purchasing a new property, such as:

- Mortgage Reducing Term Assurance (MRTA) / Mortgage Level Term Assurance (MLTA)

- Fire insurance

- Loan Instalment

- Interest rates

- Utilities deposit (Electricity and water)

- Repair or renovation costs

- Maintenance fees

Residential – Subsale

Purchasing a subsale property is almost no different than purchasing a brand new development. You will also still need to know your affordability level, and understand how much you can afford.

One of the biggest differences will however be the freebies. When it comes to residential subsale properties, the only “freebie” you may expect to get are the built-in knick-knacks already in the property.

Below is a rough estimation of how much you will need to prepare when buying a subsale property.

1) Valuation Fees And Cost

The valuation fees of a property is one of the biggest differences that sellers can expect. Valuation fees are the fees paid to professionals for evaluating how much the property is worth at today’s market value.

This valuation price will give sellers an idea of how much to sell their property for, and how much mortgage loan the banks will be willing to loan to the buyer.

This cost is usually borne by the seller. The valuation fees and costs are charged based on tiers below as of 2017:

- For The First RM100,000 – 0.25%

- Next residue up to RM2,000,000 – 0.20%

- Next residue up to RM7,000,000 – 0.20%

- Next residue up to RM15,000,000 – 0.167%

- Next residue up to RM50,000,000 – 0.10%

- Next residue up to RM200,000,000 – 0.067%

- Next residue up to RM500,000,000 – 0.05%

- Next residue over RM500,000,000 – 0.05%

* For pre/new launch residential, buyers will not need to go through the valuation step or pay any valuation fees, as the value of the property would have been obtained by the developer

2) Real Estate Agent’s Fees

Another fee that is carried by subsale properties are the Real Estate Agent’s fees. These fees are usually borne by the seller – however, they may occasionally be transferred to the buyer instead.

The charges for the Real Estate Agent’s fees are usually 2% to 3% of the property purchase price. 2% is the norm, while 3% is considered to be high.

3) Down payment

Other than the above fees, almost all the other fees apply when purchasing a developer unit.

A down payment of at least 10% also still needs to be prepared, and the difference between buying a developer unit and a subsale unit is that there will be no discounts on the down payment.

The purchaser can however also withdraw money from their EPF Account II to partially pay for the 10% down payment and Legal fees, depending on how much money they have in their Account II.

As with purchasing a developer unit, the purchaser will however need their SPA before they will be able to perform their EPF Account II withdrawal.

4) Sale And Purchase Agreement Fees (a.k.a. SPA, SNP Or S&P)

The fees for the Sale and Purchase Agreement applies for subsale properties as well, as proof of purchase. The charges for the SPA agreement also follows the same price tier as for developer units.

- For The First RM500,000 – 1.0% (Subject to a minimum fee of RM300.00)

- For The Next RM500,000 – 0.80%

- For The Next RM2,000,000 – 0.70%

- For The Next RM2,000,000 – 0.60%

- For The Next RM2,500,000 – 0.50%

This time however, the Memorandum of Transfer fees (MOT) will have to be paid together as subsale units are existing units and can be transferred immediately.

The charges are the same as for purchasing a developer unit. The Stamp Duty charges for the MOT are as follows:

- For The First RM100,000 – 1%

- For The Next RM500,000 – 2%

- RM5,000,001 and above – 3%

Other charges to note are as below:

- Professional Legal Fees are to be inclusive of 6% government tax

- Disbursement Fees will range between RM1,000 – RM1,500

5) Loan Agreement Legal Fees

The same Lawyer Fees apply as for when purchasing a subsale property, following the same standard table, whereby the price of the property determines how much a property purchaser has to pay them.

- For The First RM500,000 – 1.0% (Subject to a minimum fee of RM500.00)

- For The Next RM500,000 – 0.80%

- For The Next RM2,000,000 – 0.70%

- For The Next RM2,000,000 – 0.60%

- For The Next RM2,500,000 – 0.50%

The Stamp Duty for the legal fees are government charges when the lawyer submits your documents. They are usually only 0.5% of your loan amount.

The other charges to note are as below:

- Professional Legal Fees are to be inclusive of 6% government tax

- Disbursement Fees will range between RM1,000 – RM1,500

The other costs that property buyers will need to anticipate when purchasing a subsale property does not differ much from when purchasing a brand new property.

They will still need to prepare a sum of money for the below:

- Mortgage Reducing Term Assurance (MRTA) / Mortgage Level Term Assurance (MLTA)

- Fire insurance

- Loan Instalment

- Interest

- Utilities deposit (Electricity and water)

- Repair or renovation costs

- Maintenance fees

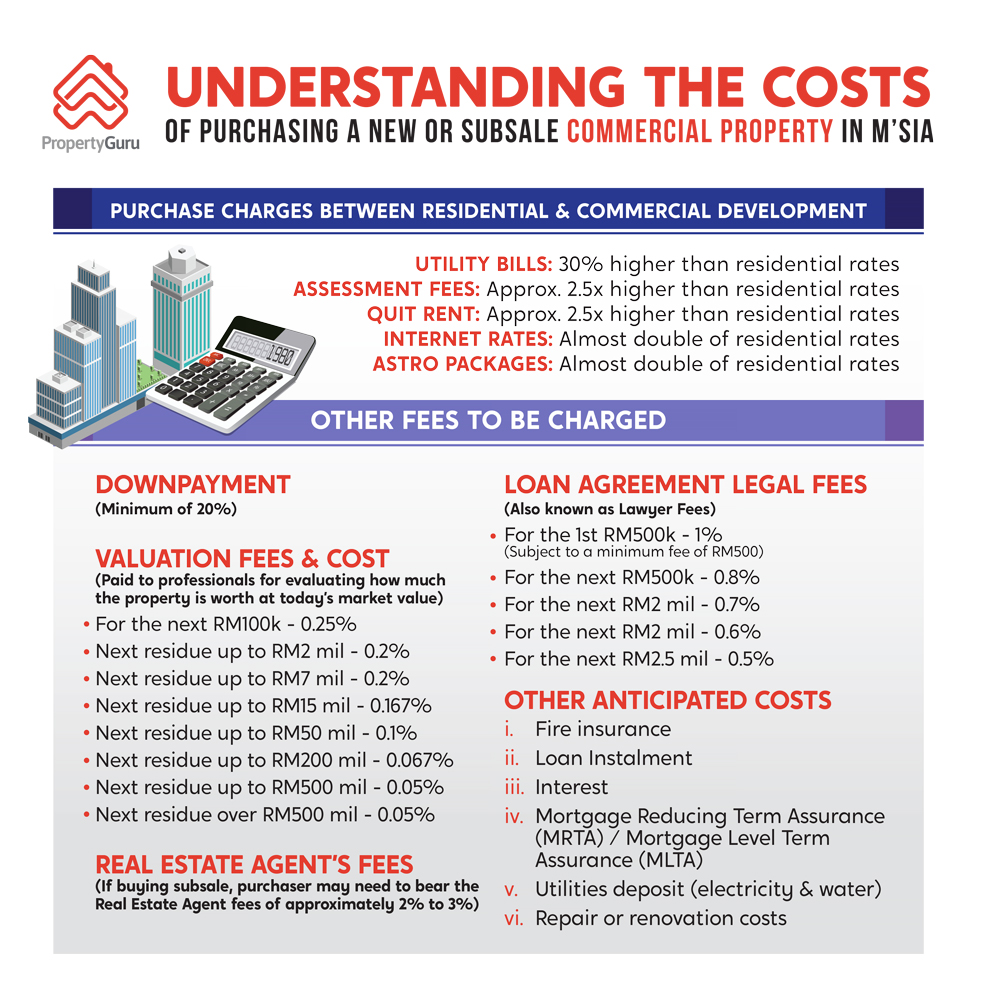

Commercial Properties

Many buyers usually find purchasing commercial properties to be intimidating because of the high cost of owning one.

True enough the budget for purchasing a commercial development has to be higher, but it is still affordable.

Below are some of the charges that differs from when purchasing a residential development and commercial development.

- Utility bills: The utility bills for commercial developments are usually approximately 30% higher than residential developments. The rates can be viewed on the Tenaga Nasional website.

- Assessment fees: The assessment fees for Commercial developments are approximately 2.5 times the rates of Residential developments. Assessment fees are charged twice a year.

- Quit Rent: The quit rent for commercial developments are also approximately 2.5 times the rates of Residential developments, but these are charged only once per year.

- Internet rates: Taking the rates from Malaysia’s leading internet provider TMNet, the price of Unifi for Commercial developments are almost double the rates for residential developments. The typical Residential rate is approximately RM168 per month, while the cheapest package for Commercial packages at TMNet is RM295 per month (inclusive of GST) as of June 2017.

- Astro packages: And if the business requires cable TV connection, applying for an Astro package will also cost almost double the Residential rate for Commercial developments.

Other than the higher assessment, quit rent and utility rates, purchasing a Commercial development is almost the same as purchasing a Residential development.

1) Down payment

The down payment for purchasing a Commercial development will be higher than purchasing a Residential development, as the maximum loan allowed for Commercial developments is only 80%.

Purchasers will hence need to pay a minimum of a 20% down

payment for their Commercial property.

And unlike purchasing a Residential property where the purchasers are allowed to withdraw money from their EPF Account II to pay for their property, Commercial property buyers are not allowed to.

2) Valuation Fees And Cost

If purchasing a subsale Commercial development, the seller will need to bear the cost of evaluating the price of the property as well.

As with Residential properties, the valuation price will give sellers an idea of how much to sell their property for, and how much mortgage loan the banks will be willing to loan to the buyer.

The valuation fees and cost are charged based on the tiers below as of 2017:

- For The First RM100,000 – 0.25%

- Next residue up to RM2,000,000 – 0.20%

- Next residue up to RM7,000,000 – 0.20%

- Next residue up to RM15,000,000 – 0.167%

- Next residue up to RM50,000,000 – 0.10%

- Next residue up to RM200,000,000 – 0.067%

- Next residue up to RM500,000,000 – 0.05%

- Next residue over RM500,000,000 – 0.05%

* For pre/new launch residential property, buyers will not need to go through the valuation step or pay any valuation fees, as the value of property would have been obtained by the developer

3) Real Estate Agent’s Fees

If purchasing a subsale Commercial property, another fee that the purchaser may need to bear is the Real Estate Agent fees of approximately 2% to 3% – where 2% is the norm and 3% is considered to be high.

And also as is with Residential developments, this cost may be transferred to the buyer instead.

4) Sale And Purchase Agreement Fees (a.k.a. SPA, SNP or S&P)

As is standard for purchasing a property, there is also the SPA fees for the documents as proof of purchase.

The charges for the SPA agreement is the same as it is for Residential developments, following the same price tier.

- For The First RM500,000 – 1.0% (Subject to a minimum fee of RM300.00)

- For The Next RM500,000 – 0.80%

- For The Next RM2,000,000 – 0.70%

- For The Next RM2,000,000 – 0.60%

- For The Next RM2,500,000 – 0.50%

For subsale Commercial developments, the Memorandum of Transfer fees (MOT) will also have to be paid together as subsale units are existing units and can be transferred immediately.

The charges are the same as for purchasing a developer unit:

- For The First RM100,000 – 1%

- For The Next RM500,000 – 2%

- RM5,000,001 and above – 3%

Other charges to note are as below:

- Professional Legal Fees to be inclusive of 6% government tax

- Disbursement Fees to range between RM1,000 – RM1,500

5) Loan Agreement Legal Fees

And also as with purchasing a Residential development, the same Lawyer Fees also apply, with the same table, whereby the price of the property determines how much a property purchaser has to pay the lawyer.

- For The First RM500,000 – 1.0% (Subject to a minimum fee of RM500.00)

- For The Next RM500,000 – 0.80%

- For The Next RM2,000,000 – 0.70%

- For The Next RM2,000,000 – 0.60%

- For The Next RM2,500,000 – 0.50%

Stamp Duty for the legal fees are the government’s charges when the lawyer submits your documents. They are usually only 0.5% of your loan amount.

Other charges to note are as below:

- Professional Legal Fees to be inclusive of 6% government tax

- Disbursement Fees to range between RM1,000 – RM1,500

The other costs that property buyers will need to anticipate when purchasing a Commercial development is almost the same, and purchasers will need to prepare a sum of money for the below:

- Mortgage Reducing Term Assurance (MRTA) / Mortgage Level Term Assurance (MLTA)

- Fire insurance

- Loan Instalment

- Interest

- Utilities deposit (electricity and water)

- Repair or renovation costs

Buying a property, whether a Commercial or Residential development can be a lucrative venture for those who are interested in long term returns and gains.

Moving on, learn how to find the best property for investment whether it is brand new, subsale or commercial.

For more guides on property buying, you can visit the following pages:

- Learn how to prepare mortgage loan documents

- Understanding commercial property loans and how to get the loan

- Signing the Letter of Offer, Sale and Purchase (SPA) and Loan Agreement

- The property buying process for subsale, commercial and new developments

To learn about property titles, payment schedules and loan documents, visit our other guides:

- Understanding the differences of freehold, leasehold and bumi lot land titles

- Payment schedule of new and under construction property project

- Loan documents for buying a property

Source: https://loanstreet.com.my/learning-centre/entry-costs-buying-property

Relevant Guides:

-

Overnight Policy Rate (OPR) In Malaysia: Why It’s So Important

-

Base Rate (BR), Base Lending Rate (BLR), Standardised Base Rate (SBR): All You Need To Know

-

3 Infrastructure Developments That Can Transform Property Prices In Malaysia

Keep Track of New Launches

Visit our new launches page to find the new launch project of your dreams and submit an enquiry today.

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.