Many Malaysians worry if their retirement savings will be enough. The rising cost of living, longer life expectancy, and economic uncertainty make future planning stressful. This concern is especially real as we enter 2026, with new changes affecting how much we need to save for retirement.

The EPF Basic Saving benchmark has been revised to reflect today’s financial reality. The old RM 240,000 target at age 55 is no longer enough. The updated benchmark affects how we plan, how much we need, and when we can realistically retire.

Understanding these new requirements is crucial to avoiding a retirement shortfall and ensuring that we can continue to live comfortably after stopping work.

If you are reviewing your finances or planning for major goals such as buying a home, now is the right time to check where you stand.

Find Out Loan Eligibility Check

Curious about your budget? Use our Eligibility Calculator to see how much home you can comfortably buy.

What Is EPF Basic Saving In 2026?

The EPF Basic Saving is the minimum recommended amount that members should have in their EPF account when they retire. It is designed to provide a basic level of financial security after stopping work, covering essential monthly expenses throughout retirement. It is based on realistic living costs, not luxury spending.

The Employees Provident Fund (EPF), also known as Kumpulan Wang Simpanan Pekerja (KWSP), is Malaysia’s national retirement savings institution. It manages compulsory and voluntary contributions and helps members build long-term financial security through structured savings and annual dividends.

The benchmark was updated because the previous target of RM 240,000 at age 55 is no longer enough. Living costs have risen, people are living longer, and retirement now spans more years. Without an updated benchmark, many Malaysians risk running short of funds later in life.

In 2026, the EPF Basic Saving benchmark is aligned to retirement planning up to age 60. This reflects current retirement needs and the period during which savings must support daily living.

Quick points to understand:

- EPF Basic Saving = the minimum recommended balance for retirement security.

- Updated in line with the Retirement Income Adequacy (RIA) framework.

- The old benchmark RM 240,000 at 55 has been replaced with a higher target.

- Now, based on retirement planning until age 60, due to a longer lifespan and a higher cost of living.

- Helps members assess if they are on track or need stronger saving strategies.

Understanding this updated benchmark is important because it sets a clear guide for planning your future and deciding how much more you need to save.

Updated EPF Basic Saving Benchmark For 2026

The Basic Saving benchmark has been revised under the Retirement Income Adequacy (RIA) framework. This new benchmark reflects the amount needed to support essential living needs during retirement based on current economic conditions and the latest Belanjawanku cost-of-living data.

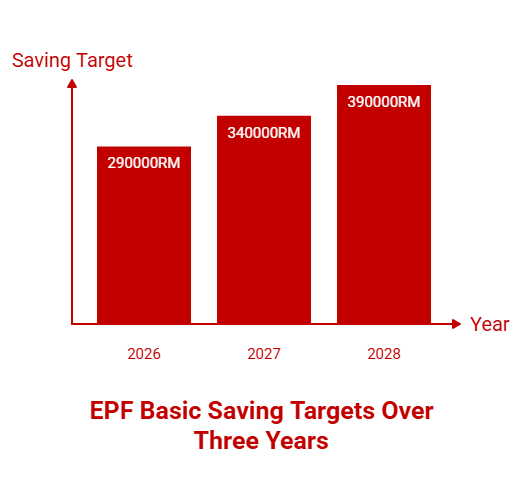

The benchmark will increase gradually over three years. This phased approach gives members time to adjust and plan.

Revised EPF Basic Saving targets:

- RM 290,000 by 1st January 2026

- RM 340,000 by 1st January 2027

- RM 390,000 by 1st January 2028

These figures represent the minimum savings recommended by EPF for retirement planning up to age 60. They are calculated to provide a basic monthly income for at least 20 years after retirement.

Why this matters?

- The previous target of RM 240,000 is not enough for today’s living costs.

- Monthly living expenses for retirees have increased significantly in recent years.

- The updated benchmark gives a more realistic picture of what is required to maintain basic needs in retirement.

What RM 290,000 means in practical terms?

- Designed to support modest monthly expenses after retirement.

- Helps members understand how much more they may need to save.

- Encourages early and consistent contributions rather than last-minute pressure.

The phased increase allows members to review their current EPF balance, plan savings strategies, and adjust contributions if necessary.

New Three-Tier Retirement Savings Framework Under RIA

The Retirement Income Adequacy (RIA) framework introduces a clearer structure for retirement planning. Instead of relying on a single savings benchmark, members now have three different targets based on retirement lifestyle needs. This helps Malaysians understand the level of retirement income they may require and plan more accurately.

The three tiers are:

- Basic

- Adequate

- Enhanced

Each tier reflects a different level of financial security during retirement, aligned with the latest Belanjawanku 2024/2025 living cost estimates.

Let’s Understand the three tiers:

1. Basic Savings

- Designed to cover essential monthly expenses.

- Benchmark target: RM 390,000 by age 60 (fully implemented by 2028).

- Intended to support basic living needs.

2. Adequate Savings

- For a more comfortable lifestyle with broader financial flexibility.

- Benchmark target: RM 650,000 by age 60.

3. Enhanced Savings

- Provides higher financial security and lifestyle options in retirement.

- Benchmark target: RM 1.3 million by age 60.

These tiers were developed using the latest Belanjawanku expenditure guidelines to ensure the targets match real living expenses. They offer Malaysians a structured guide to planning retirement rather than guessing or relying on outdated estimates.

Why this three-tier model matters?

- Creates clearer retirement planning goals for different lifestyles.

- Shows a realistic picture of what retirement may cost today.

- Helps members evaluate whether they need to increase contributions or explore supplementary savings options.

Understanding which tier you aim for can help shape long-term financial decisions, including voluntary EPF contributions, investment choices, and retirement income planning beyond EPF.

Where Do Malaysians Stand Today Against These New Targets?

Many Malaysians are still far from reaching the revised EPF Basic Saving benchmark. Recent figures show that a large portion of contributors may struggle to meet the new savings target when the phased increases take effect.

Current EPF savings reality

- Nearly 48% of EPF members below age 55 have less than RM 10,000 in their accounts.

- As of 2025, only 23.9% of all EPF members aged 18–55 have reached the basic savings level recommended for their age.

- Only around 42% of members aged 51–55 have met the benchmark that applied before the 2026 revision.

These numbers show that a significant retirement savings gap still exists, especially among those approaching retirement age. Many members may struggle to reach the new Basic Saving target of RM 390,000 by age 60 without additional action or stronger savings discipline.

Why do many fall short?

Common challenges include:

- Low or irregular income affecting contribution levels

- Early withdrawals reduce long-term compounding

- A higher cost of living is limiting disposable savings

These trends suggest that relying only on mandatory contributions may not be enough for many Malaysians. More proactive planning is needed to catch up and move closer to the revised benchmark.

Figure Out Your Home Budget Easily

Get fast estimates on how much you can borrow and repay.

How Can You Grow Your EPF Basic Savings in Malaysia in 2026?

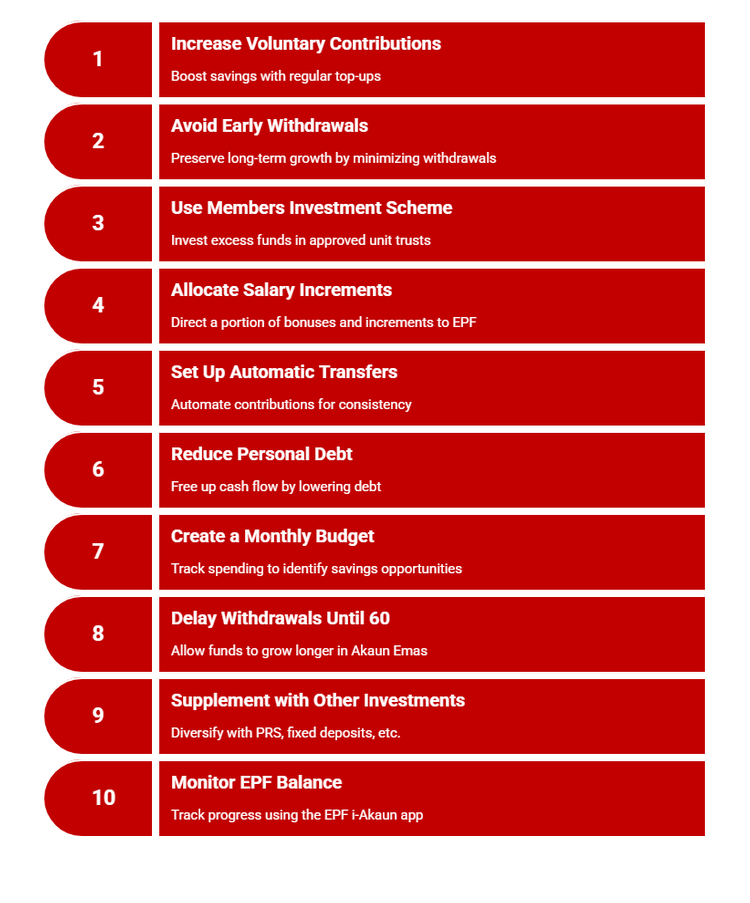

With the revised EPF Basic Saving benchmark being phased in, taking proactive steps now can make a significant difference. Here are ten practical ways Malaysians can strengthen their retirement savings in 2026.

1. Increase Voluntary Contributions

Voluntary top-ups can help close savings gaps faster. Even a small fixed monthly amount can accumulate significantly through compounding. Members with irregular income can contribute at any time via self-contribution or i-Saraan.

2. Avoid Unnecessary Early Withdrawals

Every withdrawal reduces the long-term growth of your savings. If possible, reserve EPF withdrawals for essential needs only. Leaving funds untouched helps maximise compounding returns over the years.

3. Use the Members Investment Scheme (MIS)

If your EPF balance exceeds the Basic Savings threshold, you may invest part of the excess in approved unit trusts through MIS. This can potentially generate higher returns, depending on risk tolerance and market conditions.

4. Allocate Part of Salary Increments or Bonuses

Directing even 10% to 20% of bonuses or annual salary increments into EPF can accelerate progress without significantly affecting monthly expenses.

5. Set Up Automatic Savings Transfers

Automating voluntary contributions helps create consistency. It removes the need for manual decisions and ensures saving becomes a habit rather than an occasional action.

6. Reduce Personal Debt to Free Up Cash Flow

Lowering loan commitments, especially high-interest debt, frees more money for savings. Managing debt well supports stronger financial planning and long-term security.

7. Create a Realistic Monthly Budget

Tracking spending helps identify areas where expenses can be reduced. Reducing non-essential expenditure and redirecting savings to EPF can create meaningful long-term gains.

8. Delay Withdrawals Until Age 60

Members who continue working beyond age 55 can let funds grow in Akaun Emas, delaying withdrawal until age 60. This allows an additional five years of compounding.

9. Supplement EPF With Other Investment Channels

Consider adding private retirement schemes (PRS), fixed deposits, or diversified investment options. Relying only on EPF may not provide enough for those aiming for the Adequate or Enhanced tiers.

10. Monitor Your EPF Balance Regularly

Use the EPF i-Akaun app to track your progress against the new benchmark. Reviewing savings frequently helps you adjust contribution strategies and keep goals realistic.

Taking these steps early can help Malaysians move closer to the new EPF Basic Saving benchmark and reduce financial stress as retirement approaches.

What Does the New EPF Basic Saving Benchmark Mean for Different Age Groups?

Different age groups face different challenges when working towards the updated Basic Saving benchmark. Here is a simple view of what each group should consider.

20s

Longest time to grow savings through compounding.

Start early, avoid withdrawals, set small monthly top-ups, build consistent habits.

30s

Balancing career growth and family commitments.

Allocate part of bonuses or increments to EPF, track progress, create a solid budget.

40s

Higher pressure due to shorter compounding window.

Increase contributions, automate savings and explore supplementary investments.

50s

Critical stage to close gaps before retirement.

Review savings vs benchmark, reduce debt and delay withdrawals if possible.

Near 60

Time to plan how savings will sustain living expenses.

Plan withdrawal timeline, estimate monthly needs and seek financial guidance if needed.

This breakdown helps members see where they stand today and decide what actions suit their life stage.

Are You Prepared to Reach the New EPF Basic Saving Target by 2026?

The new EPF Basic Saving benchmark may feel overwhelming, especially with rising living costs and increasing financial commitments. Many Malaysians are still catching up, and it is normal to feel unsure about whether your current savings will be enough. But small, consistent action can make a big difference.

Start by understanding where you stand today. Compare your EPF balance against the new benchmark, set realistic targets, and take advantage of the many tools and strategies available to grow your savings.

Planning your next financial step? Explore helpful tools, retirement planning insights, and property-related resources tailored for Malaysians. Visit PropertyGuru Guides Now!

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.