The Real Property Gains Tax (RPGT) remains one of the most significant taxes for Malaysian property owners, investors, and those planning to sell a home. However, the system underwent considerable changes as of January 1, 2025, transitioning to a comprehensive self-assessment regime, introducing new filing requirements, and tightening compliance standards for both buyers and sellers.

Whether you are disposing of a residential unit in Kuala Lumpur, cashing out on a landed home in Johor, or navigating the disposal of a corporate property, understanding RPGT tax malaysia is crucial, especially if you want to avoid costly penalties or filing delays.

Search homes for rent nationwide

See units aligned with your budget and needs.

Why RPGT Exists?

When RPGT was first introduced in 1976, it was not merely a tax instrument but a policy designed to guide Malaysia’s property market towards long-term health and stability. At its core, RPGT exists to curb unhealthy speculation, the kind that artificially inflates prices and pushes genuine homebuyers out of the market.

By taxing gains made from short-term disposals, the Government discourages "flip for quick profit" behaviour and encourages more responsible, sustainable investment.

Beyond speculation control, RPGT also plays several vital roles:

- Stabilising property prices: It helps prevent sudden spikes caused by speculative buying, particularly in fast-growing markets.

- Ensuring fair taxation of capital gains: Individuals and companies that benefit from significant profits on disposal contribute a proportionate amount back to the economy.

- Supporting national revenue during economic cycles: RPGT serves as a counter-cyclical tool, providing fiscal support during periods of market volatility.

Today, in 2025, RPGT remains central to regulating a property landscape that continues to evolve.

With high-demand areas such as the Klang Valley, Penang, and Johor attracting intense transactional activity, RPGT helps maintain a degree of balance, protecting affordability, encouraging fair market behaviour, and ensuring that growth does not come at the expense of stability.

What Is RPGT Tax in Malaysia?

Real Property Gains Tax (RPGT) is a tax imposed on the profit you make when disposing of a property or shares in an honest property company (RPCS). At its core, it is a tax on gains, not on the selling price itself.

Put simply: RPGT = Tax on the net profit earned from selling a property.

For example, if you purchased a condominium for RM500,000 and later sold it for RM650,000, the RM150,000 gain may be subject to RPGT, depending on your holding period and taxpayer category.

RPGT covers a broad range of asset types, including:

- residential properties,

- commercial properties,

- vacant land,

- industrial buildings,

- shares in a Real Property Company (RPC), and

- Any rights connected to the disposal of real property.

The framework is governed by the Real Property Gains Tax Act 1976 and administered by Lembaga Hasil Dalam Negeri (LHDN), ensuring that property transactions are taxed fairly and transparently.

Key RPGT Exemptions Every Malaysian Property Owner Should Know

Malaysia offers several necessary exemptions that can significantly reduce, or even remove, your Real Property Gains Tax liability.

The key ones to understand are:

1. Once-in-a-Lifetime Residential Property Exemption

Malaysian citizens are entitled to a full exemption on the gain from the disposal of one residential property during their lifetime. Many homeowners reserve this for a significant upgrade or the sale of a long-held family home.

2. Exemptions for Transfers Within Immediate Family

Certain transfers that do not involve a genuine sale are fully exempt from RPGT. These include transfers between:

- Husband and wife,

- parents and children, and

- Grandparents and grandchildren.

Transfers between siblings, however, do not qualify for this exemption.

3. Automatic RM10,000 or 10% Exemption

Every disposal automatically receives the higher of:

- RM10,000, or

- 10% of the chargeable gain.

This deduction is applied upfront when calculating the amount subject to tax.

4. Exemption for Divorce-Related Transfers

Transfers arising from a court order or formal settlement agreement in a divorce are also exempt, ensuring that asset redistribution does not trigger an unintended tax burden.

Together, these exemptions provide meaningful relief and ensure that RPGT remains fair, practical, and sensitive to genuine life circumstances.

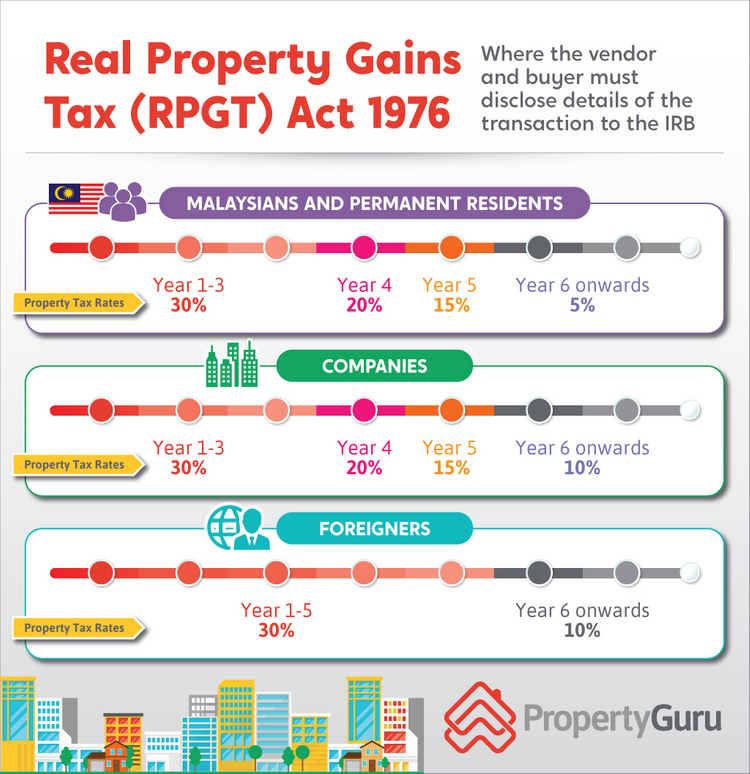

RPGT Rates in Malaysia

RPGT rates depend on two factors:

- Who you are (Malaysian citizen, PR, foreigner, or company)

- How long do you hold the property before it is disposed of?

Below is the latest RPGT rate table, applicable to disposals from 1 January 2025 onwards:

RPGT Rates in 2025:

Year 1-3

30%

30%

30%

30%

Year 4

20%

30%

20%

30%

Year 5

15%

30%

15%

30%

After Year 5

0%*

10%

10%

10%

*Residential exemptions still apply and must be formally claimed (details below).

Important

For Malaysian citizens and permanent residents, disposals made after Year 5 are typically charged at 0%, especially for residential properties where exemptions may be available.

Local companies, however, move to a 10% RPGT rate after Year 5, while foreign companies face a 30% rate up to Year 5, before dropping to 10% from Year 6 onwards.

Regardless of category, all exemptions and reliefs must be claimed using the correct CKHT forms to ensure compliance with LHDN’s requirements.

Plan your financing smarter

Check your repayment range before you proceed.

How is RPGT calculated in Malaysia?

RPGT is not simply charged on your selling price. Instead, it is calculated based on your chargeable gain, which is the actual profit you make after deducting all allowable costs associated with buying, holding, and selling the property.

Understanding this structure ensures you neither overpay nor overlook legitimate deductions that could significantly reduce your tax bill.

The Core Formula: Chargeable Gain = Disposal Price – Acquisition Price – Allowable Expenses – Exemptions

Each part of the formula plays a specific role:

1. Disposal Price

This is the actual amount you receive from the sale of the property.

In certain situations, the Inland Revenue Board (LHDN) may adjust the figure if part of the transaction is deemed non-arm’s-length, artificially inflated, or does not reflect genuine market value. The goal is to ensure the disposal price used in RPGT calculations represents a fair and legitimate transaction.

In certain situations, the Inland Revenue Board (LHDN) may adjust the figure if part of the transaction is deemed non-arm’s-length, artificially inflated, or does not reflect genuine market value. The goal is to ensure the disposal price used in RPGT calculations represents a fair and legitimate transaction.

2. Acquisition Price

The acquisition price goes beyond the amount you originally paid for the property.

It also includes incidental costs tied to the purchase, such as:

It also includes incidental costs tied to the purchase, such as:

- legal fees;

- stamp duty;

- Valuation or surveyor fees, where relevant.

These costs are recognised because they form part of the total investment in acquiring the asset.

3. Allowable Expenses

Allowable expenses refer to costs directly linked to enhancing or enabling the disposal of the property. Common examples include:

- Value-adding renovation works;

- advertising expenses;

- legal fees incurred for the sale;

- Estate agent commissions.

However, under Paragraph 3, Schedule 2, not everything qualifies.

Routine repairs, cosmetic upgrades, or general maintenance cannot be claimed, as these are considered part of regular property upkeep rather than capital enhancement.

Example:

Property Details

- Bought: RM600,000

- Sold: RM750,000

- Holding period: 4 years

- Allowable expenses: RM15,000

- Exemption: RM10,000 or 10% of gain (whichever is higher)

Step 1: Compute initial gain

RM750,000 – RM600,000 = RM150,000

Step 2: Deduct expenses

RM150,000 – RM15,000 = RM135,000

Step 3: Apply exemption

RM135,000 – RM13,500 (10%) = RM121,500

Step 4: Apply RPGT rate (Year 4 = 20%)

RM121,500 × 20% = RM24,300 RPGT payable

Ultimately, understanding how RPGT is computed provides the clarity needed to plan your disposal strategically and maximise the value of your hard-earned gains.

RPGT Self-Assessment in 2026: What Property Sellers Must Now Do?

Beginning January 1, 2025, the Real Property Gains Tax officially adopts a self-assessment system (SAS). This marks a significant shift in responsibility: sellers must now accurately compute their own RPGT, prepare all supporting documents, and submit the required CKHT forms without relying on LHDN to perform the calculations.

The move mirrors Malaysia’s existing self-assessment income tax model, aiming to streamline processes, improve compliance, and expand the use of digital submissions.

To help you navigate the new framework, here’s what has now changed under RPGT self-assessment:

1. You Must Calculate Your Own Chargeable Gain

LHDN will no longer determine your RPGT on your behalf. Sellers must compute their own profit, apply the appropriate exemptions, and calculate the final tax payable.

2. The Buyer Still Withholds the Retention Sum

Despite the shift to SAS, buyers must continue to retain and remit the RPGT retention sum, generally 3% of the disposal price, within the stipulated timeframe.

3. CKHT Forms Must Be Filed Within 60 Days

All CKHT-1, CKHT-2, or CKHT-3 forms must be completed and submitted within 60 days of the disposal date. Late submissions attract penalties, even if the tax payable is eventually corrected.

4. Full Documentation Is Required

You must maintain and submit complete supporting documents, including:

- SPA for acquisition

- SPA for disposal

- Proof of allowable expenses

- Loan statements

- Receipts and invoices

- Valuation reports, where relevant

Proper documentation ensures that your self-calculation withstands potential LHDN audits or verification.

5. Digital Filing Is Strongly Encouraged

LHDN is expanding its digital platforms, notably:

- e-CKHT

- MyTax portal

- Online payment channels

This shift aims to reduce manual paperwork and make compliance easier for both buyers and sellers.

Handled with care and proper documentation, the new self-assessment approach can be both manageable and efficient for property sellers in 2025.

CKHT Forms and Filing Requirements

RPGT compliance in 2026 centres on submitting the correct CKHT forms within the mandatory timelines. Both sellers and buyers have distinct responsibilities, and failing to complete any form can delay processing or result in penalties.

Forms Required from Sellers

Sellers must file the following documents when disposing of a property:

- CKHT 1A (Disposal Form)

The primary declaration form is where you report the disposal, compute your chargeable gain, and determine the RPGT payable. - CKHT 3 (Exemption Form)

Used to claim available exemptions, including once-in-a-lifetime exemptions for individuals and qualifying transfers between family members. - CKHT 2A (Amendment Form)

Submitted only if corrections or adjustments are needed after the initial filing.

Forms Required from Buyers

Buyers also have statutory obligations under RPGT:

- CKHT 4A (Acquisition Form)

A formal declaration of the property purchase. - Retention Payment Slip

Proof that the mandatory retention sum (typically 3% of the disposal price) has been remitted to LHDN.

Filing Timeline for 2026

The filing deadline remains unchanged: All CKHT forms must be submitted within 60 days from the date of disposal, which is generally the date the SPA is signed.

Late submissions may attract penalties, additional tax assessments, and processing delays.

By staying disciplined with the required forms and timelines, both buyers and sellers can ensure a smooth, compliant RPGT process, avoiding unnecessary penalties and keeping the transaction firmly on track.

All CKHT forms can also be conveniently downloaded directly from the IRB’s (LHDN) official website, ensuring easy access to the most current versions and filing instructions.

Common Mistakes Malaysian Sellers Make

Before you file your RPGT, it’s worth understanding the slip-ups that frequently catch sellers off guard, many of which are entirely avoidable with a bit of preparation:

1. Assuming RPGT is zero after five years without filing

Even if RPGT is 0%, you must still file CKHT forms.

Failure = penalty.

Failure = penalty.

2. Using renovation expenses that are not legally claimable

Only specific categories count.

3. Not documenting allowable expenses

Without receipts, deductions are often rejected.

4. Incorrectly calculating acquisition price

Especially for inherited or transferred properties.

5. Missing the 60-day deadline

This creates unnecessary penalty exposure.

By avoiding these common errors, you not only protect yourself from penalties but also ensure your disposal is handled cleanly, accurately, and in full compliance with 2025 requirements.

Thinking of Selling or Buying Property in 2026?

Whether you are disposing of an existing home or preparing to purchase your next one, understanding how RPGT works gives you a clearer sense of your actual financial position.

From knowing which exemptions apply to calculating your chargeable gain accurately to navigating the new self-assessment rules, being well-informed helps you plan, avoid unnecessary penalties, and preserve more of the profit you’ve worked hard to earn.

If you are exploring your next move, PropertyGuru Malaysia offers an extensive range of verified listings, neighbourhood insights, and market data to guide your decision.

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.