Property damage can happen in many ways, from construction defects and natural disasters to accidental destruction by neighbours, tenants, or contractors. When the unexpected occurs, most homeowners struggle with the same question: What should I do now?

Fortunately, Malaysian law offers several remedies to help you assess the damage, file claims, and pursue compensation. This guide outlines the essential legal steps every homeowner should be aware of.

Fortunately, Malaysian law offers several remedies to help you assess the damage, file claims, and pursue compensation. This guide outlines the essential legal steps every homeowner should be aware of.

Stay Informed On Malaysian Property Laws

Get practical guidance and tips for homeowners.

Understanding Your Situation Immediately

Dealing with property damage can feel like your world has turned upside down. The first few hours are crucial.

Start by ensuring your personal safety: if there is a risk of collapse or fire, evacuate and alert the authorities. Once safe, begin to stabilise and secure the site. Lock doors, restrict access, and try to prevent further harm.

At the same time, mentally prepare for what comes next. You will need to deal not just with the emotional fallout but also with a legal and insurance process. Having a structured action plan early on can save you stress, money, and time in the long run.

Start by ensuring your personal safety: if there is a risk of collapse or fire, evacuate and alert the authorities. Once safe, begin to stabilise and secure the site. Lock doors, restrict access, and try to prevent further harm.

At the same time, mentally prepare for what comes next. You will need to deal not just with the emotional fallout but also with a legal and insurance process. Having a structured action plan early on can save you stress, money, and time in the long run.

Preserving Evidence After Property Damage

Strong documentation is vital. Without proof, your claim, whether to your insurer or a court, may be weak. Here is how to preserve crucial evidence for property damage:

1. Photograph and Video Record

Take wide-angle and detailed shots from different vantage points. Use your phone or a camera with timestamped metadata. Capture close-ups of cracks in walls, damaged fixtures, and debris.

2. File a Police Report

If the damage appears intentional (vandalism) or stems from negligent third-party conduct, file a police report without delay. A police report helps support your insurance claim and provides stronger proof if you need to take legal action.

3. Speak to Witnesses

Neighbours, passers-by, or security guards may have seen something. Secure written or recorded statements with names and contact information. Witness testimony can carry significant weight in court.

4. Expert Inspection

Hire a structural engineer, fire safety expert, or quantity surveyor to conduct a technical assessment. Their report becomes a critical piece of objective evidence in both your insurance claim and any civil lawsuit.

5. Repair Estimate

Obtain detailed, itemised repair quotations from reputable contractors. These estimates should break down labour, materials, and any additional costs.

By taking these preservation steps, you will build a solid foundation to justify your claim and back your demand for compensation.

Notifying Your Insurer and Initiating a Claim

Once you have evidence, you must act quickly to launch an insurance claim for property damage. Here’s how to navigate this process:

1. Locate Your Policy Documents

Review your homeowner’s or fire insurance policy. Identify which perils are covered (fire, flood, all-risk), the sum insured, and any exclusions.

2. Notify Your Insurer Promptly

Contact your insurer as soon as possible. Provide a written notice along with initial documentation: police report (if any), photos, and your repair estimate.

3. Submit Claim Forms

Use your insurer’s specified form or online portal. Fill it in carefully, and be clear and precise about the extent and cause of the property damage.

4. Know Your Rights Under Bank Negara Standards

As of 1 July 2024, general insurers in Malaysia must comply with the Policy Document on Claims Settlement Practices (PD CSP) issued by Bank Negara Malaysia. Insurers are required to process claims fairly, transparently, and in a timely manner.

5. Request a Detailed Loss Estimate

Under PD CSP rules, you are entitled to receive an itemised breakdown of how the insurer calculates repair costs, including labour, parts, betterment (if applied), and salvage deduction.

Taking these steps helps ensure that your insurer treats your claim seriously and that all aspects of the loss are properly evaluated.

Planning To Buy A Home Soon?

Explore a wide range of residential properties across Malaysia.

What If the Insurer Denies or Undervalues Your Claim?

Insurance companies may reject or undervalue your claim. If that happens, you have rights and remedies:

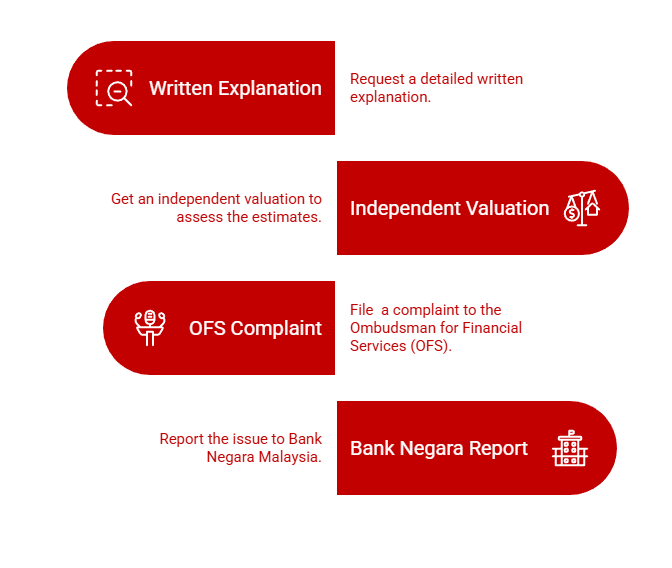

1. Seek a Written Explanation

Ask for a detailed repudiation letter stating why the claim was denied or discounted. Under PD CSP, insurers must clearly articulate their reasoning.

2. Obtain an Independent Valuation

Engage a third-party surveyor or quantity surveyor to provide an independent repair estimate. Use it to question the insurer’s figures if they are significantly lower.

3. File a Complaint with the Ombudsman

You can escalate unresolved disputes to the Ombudsman for Financial Services (OFS). Many insurers’ service charters specify this route.

4. Report to Bank Negara

If you suspect your insurer is not abiding by the PD CSP, you can lodge a complaint through Bank Negara Malaysia Link.

By asserting your rights, you put yourself in a better position to negotiate or escalate the matter formally.

Civil Legal Remedies: When You Can Sue

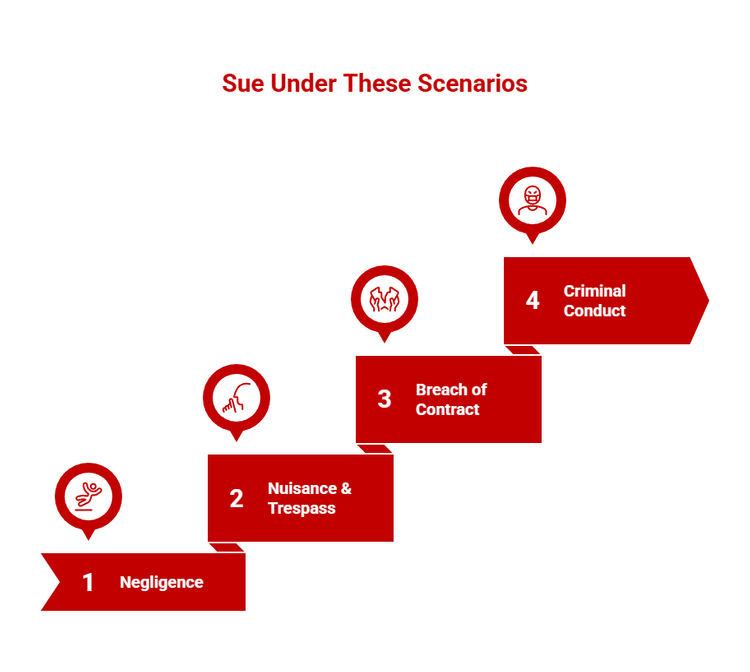

If your property damage was caused by someone else’s negligence, deliberate act, or breach of contract, you may consider a civil lawsuit. Here are some legal options:

- Negligence: If a developer, architect, or third party failed to take reasonable care, leading to your loss, you may hold them liable. The court will assess duty, breach, causation, and damage.

- Nuisance / Trespass: If someone has intruded on or trespassed on your property (for example, through unauthorised excavation), you may sue on these grounds.

- Breach of Contract: Where there is a Sale and Purchase Agreement (SPA) or formal contract (for renovation, construction, or maintenance), damage caused by breach can give rise to compensation claims.

- Criminal Conduct: For wilful destruction (vandalism or malicious damage), report to the police first. While criminal prosecution won’t automatically give you compensation, the police report can support your civil claim.

Filing a civil action provides a structured way to recover loss, but it is usually more complex and time-consuming than an insurance claim.

Which Court Should You Go To?

When taking legal action for property damage in Malaysia, the court you choose matters. Different courts handle different claim values and levels of legal complexity. Filing in the right jurisdiction ensures your case proceeds smoothly and avoids unnecessary delays.

Deciding where to file your lawsuit depends on the scale of your property damage claim:

- Small Claims Court: In Malaysia, this court handles individual claims up to RM5,000. This streamlined process is designed for modest claims and excludes companies as plaintiffs. It aims to provide a quicker, cheaper resolution for small disputes.

- Magistrates’ Court: This court hears civil claims generally up to RM100,000. It covers a wider scope of claims beyond small claims and allows for regular civil procedures. This is the proper jurisdiction for mid-sized claims exceeding the small claims limit.

- Sessions & High Court: The Sessions Court takes civil claims generally between RM100,001 and RM1,000,000, while the High Court handles claims exceeding RM1,000,000 and cases involving complex legal issues or special remedies such as injunctions or specific performance

Choosing the correct jurisdiction is essential to ensure your claim is heard and enforced properly, helping you avoid wasted time, costs, and procedural setbacks.

Emergency Remedies: Injunctions and Caveats

In urgent property disputes, waiting for a full trial may not be practical. Malaysian law provides several fast legal measures to protect your rights before a case concludes.

These emergency remedies help prevent further damage, loss, or unfair transfers while the dispute is being resolved.

Sometimes you may require urgent legal intervention:

- Injunction: If there is a risk of further property damage, or a party intends to demolish, transfer, or dispose of property, you may apply to the court for an injunction to halt them.

- Caveat: If there is a dispute over title or ownership, you can lodge a private caveat at the Land Office to prevent registration or transfer until your claim is resolved.

- Preservation Orders: In rare but serious cases, the court may issue a Mareva injunction or similar order to freeze assets or prevent disposal pending litigation.

These remedies can function as a powerful tool to stabilise your situation while your claim proceeds. They help secure assets, maintain the status quo, and prevent the other party from taking actions that could weaken your position.

New Launches Across Malaysia

Explore upcoming residential developments and new projects.

Compiling Evidence for Court or Insurance

If you decide to go to court or challenge your insurer, strong documentation is non-negotiable. Make sure you have:

- Photos, videos, and timestamped date and time information showing the scope of property damage.

- Expert reports (structural engineers, surveyors, fire experts).

- Witness statements, with names and contact information.

- Repair and replacement cost estimates from contractors.

- Receipts, invoices, or proof of past maintenance (to show pre-damage condition).

- All correspondence with your insurer, including letters, emails, and claim forms.

- Your original insurance policy and any renewal documents.

Well-ordered, comprehensive evidence boosts your credibility and strengthens your case.

How to Quantify Your Losses

When claiming compensation, you must put a monetary figure on your loss. This helps the insurer, court, or opposing party understand the financial impact of the damage. A clearer, well-supported valuation strengthens your case and improves your chance of fair recovery.

Your claim can include:

- Special (Pecuniary) Damages: These are tangible costs: repair or reconstruction, replacement of damaged contents, clean-up, temporary accommodation, and professional fees.

- General (Non-Pecuniary) Damages: More subjective losses such as inconvenience, loss of use, and mental distress (though Malaysian courts may limit such awards).

To compute your claim:

- Use the expert report and contractor estimates to arrive at a detailed figure.

- Add incidental costs: relocation, storage, and disposal.

- Consider future loss: risk of latent defects or structural weakness.

- Prepare a well-documented schedule of loss to present either to the insurer or to the court.

A professional quantity surveyor can help organise these numbers and give credibility to your claim, making it easier for the court or insurer to assess your compensation fairly.

Limitation Periods: Key Deadlines

It is vital to act within the legal time limits set by Malaysian law, as missing these deadlines can result in losing the right to pursue compensation entirely.

- Under the Limitation Act 1953, most claims involving negligence or breach of contract must be filed within six years from the date the property damage occurred.

- The Limitation (Amendment) Act 2018 introduced Section 6A, which provides a three-year discovery period specifically for latent property damage claims.

- There is also a 15-year long-stop rule, which prevents any claim from being filed more than 15 years after the negligent act, even if the damage is only discovered later.

For example, if a structural defect was built into your home in 2008 but only became clear in 2018, you may have until 2021 (three years from discovery) to sue, provided the 15-year ceiling has not passed.

Missing these deadlines could prevent you from making a claim, so it is advisable to consult a lawyer early to understand your options and protect your legal rights.

Planning Your Litigation Strategy

Pursuing a lawsuit for property damage requires careful planning. Careful preparation helps you manage risks, gather evidence effectively, and make informed decisions throughout the legal process.

Key factors to keep in mind when planning your litigation strategy:

- Estimate Legal Costs: Legal fees, court costs, expert report fees, and counsel (if required) can add up.

- Timeline: Understand the expected timeline for your case. Urgent remedies like injunctions may be quick; a full damages trial could take months or even more than a year, depending on the case’s complexity.

- Alternative Dispute Resolution (ADR): Consider mediation or arbitration to resolve the dispute more quickly and cost-effectively. Many developers or insurers may agree to ADR.

- Risk vs Reward Assessment: Assess the risks and rewards before going to court, including whether your evidence is strong, whether the other party can pay, and if the outcome is worth the legal cost.

- Leverage Negotiation: Use your evidence and expert valuations to try settling with the other party or insurer before you enter a full legal process and spend more money.

A carefully crafted litigation strategy helps you balance cost, time, and potential gain, making your pursuit of justice more focused and pragmatic.

New Rental Homes Waiting for You

Discover the latest rental properties, including condominiums, apartments, and landed homes across Malaysia.

Special Scenarios: Defects, Tenant Damage, Third-Party Harm

1. Latent Defects

If the damage is not immediately visible (for example, water seepage, hidden structural cracks), this is known as a latent defect. Thanks to the amended Limitation Act, you may use the three-year discovery period (Section 6A) to bring a claim when you first recognise the issue. Engaging an expert to date the defect to when it first appeared vs. when you discovered it is crucial.

2. Tenant-Caused Damage

If a tenant damages your property:

- Check your tenancy agreement. You may be able to claim repairs or costs from the tenant.

- Use your landlord insurance (if you have it) to cover the damage, depending on your policy.

- If necessary, issue a “letter of demand” and initiate a civil claim to recover losses.

3. Third-Party Destruction (Neighbour / Contractor)

For property damage caused by negligence, trespass, or intentional harm by a neighbour or contractor:

- Use your preserved evidence (photos, expert report, witness statements).

- Report the act to the police if it was intentional.

- Claim for damages via civil action (tort, nuisance, or contract), or via your insurer if covered.

Next Steps: What Every Homeowner Should Do

Here is a simple, practical action plan if your property has been damaged:

- Stabilise and Secure – Ensure safety, restrict access, and document everything.

- Report – File a police report if criminal conduct is suspected.

- Notify Insurer – Lodge your insurance claim promptly with full documentation.

- Get Expert Help – Hire engineers or surveyors to assess damage.

- Assess Remedies – Decide whether to resolve via insurer negotiation, ADR, or civil suit.

- Consult a Lawyer – Especially if you anticipate litigation or need injunctions/caveats.

- Monitor Deadlines – Be aware of limitation periods under Malaysian law.

- Review Settlement Offers – Do not accept undervalued offers without expert valuation.

- Take Legal Action If Needed – File civil action in the appropriate court, with the help of your legal counsel.

When property damage happens, you do not have to face it alone. You still have options. Record everything, reach out to the right parties, and take the necessary steps to protect your rights and move forward with confidence.

Ready To Check Your Home Loan Eligibility?

Ready To Check Your Home Loan Eligibility?

Calculate your borrowing capacity, compare loan options, and plan your home purchase with confidence. Use the Home Loan Eligibility Calculator on PropertyGuru Malaysia.

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.