Have you ever been handed a legal document called a Letter of Indemnity and felt unsure about what you were really agreeing to? Many of us face this situation when buying a home, signing a tenancy agreement, or dealing with renovation or handover issues. It is easy to feel pressured to sign quickly, especially when the transaction is time-sensitive.

Property paperwork today has become more detailed, with stricter compliance checks and more parties involved. Because of this, Letters of Indemnity are increasingly used to protect one party when there is risk, missing information, or uncertainty. But signing it without understanding the actual implications can lead to financial loss or disputes later.

This article explains the letter of indemnity meaning, why it matters, when it is used, and what you must check before signing. The goal is to help you make clear and confident decisions.

Plan Your Budget With Confidence

Check how much you can afford in seconds.

Letter Of Indemnity Meaning: What It Actually Is?

A Letter of Indemnity is a legal document in which one party agrees to assume responsibility and compensate another party if something goes wrong. In simple terms, it is a written assurance that protects someone from loss, damage, or legal consequences when a transaction involves uncertainty or a lack of confirmation.

Many property buyers and owners sign a Letter of Indemnity without realising the seriousness of the commitment. It is more than just a form. It is a binding agreement. If the risk materialises, the person who issued the indemnity must pay the losses. That is why understanding its meaning before signing is important.

Why Does A Letter Of Indemnity Exists?

To allow a property transaction to continue smoothly when there is an unresolved issue

- To give reassurance to the party taking on the risk

- To prevent delays while waiting for documents or approvals

- To reduce the chances of disputes or legal action later

Simple Example To Understand

Here are the main reasons it is issued:

Imagine you are buying a sub-sale property, but the original strata title has not yet been issued. The seller may issue a Letter of Indemnity promising to cover any financial loss if issues arise related to the pending title. You may proceed with the sale, but the seller will now be responsible if a problem arises.

A Letter of Indemnity can be useful, but it must be understood clearly. Once signed, both parties are legally bound by its terms. Never treat it as just another document.

When And Why It Is Used In Malaysian Property Deals?

A Letter of Indemnity is used in property transactions when there is a risk that needs protection or when something is not fully confirmed at the time of signing. It helps the transaction move forward without waiting for every document or condition to be completed.

In these situations, the LOI serves as a safeguard, allowing both parties to proceed with confidence.

Common Situations Where an LOI Is Used?

These are some of the most common scenarios in Malaysia where a Letter of Indemnity may be requested:

- Subsale property transactions: When the strata title is not yet available, and buyers need reassurance before signing the Sale and Purchase Agreement.

- New development handover: When there are minor outstanding defects or delays in final documentation.

- Tenancy agreements: When a tenant requests permission to renovate a unit and the landlord wants protection for potential damage or safety risks.

- Early termination of tenancy: When either party wants to exit before the contract ends, and the other party wants financial assurance.

- Banking and financing matters: When original loan or title documents are lost or misplaced, and must be replaced.

- Disputes on responsibility: When it is unclear who should bear certain charges, repair costs, or penalties.

These situations usually involve uncertainty, missing documents, or overlapping responsibilities. A Letter of Indemnity helps protect the affected party until all issues are resolved.

Why Is It Important In These Cases?

Here is why a Letter of Indemnity becomes necessary during these moments:

- It keeps the transaction moving without lengthy delays.

- It clarifies who will be responsible if something goes wrong.

- It reduces stress and avoids future arguments.

- It builds trust between the parties and helps complete the deal smoothly.

A Letter of Indemnity is most useful when there is uncertainty or risk. It allows transactions to proceed while protecting the party with more to lose. Understanding this helps you decide whether a request is reasonable or if the risk is too high.

Now that we know when it is used, it is important to understand what makes a solid and reliable Letter of Indemnity.

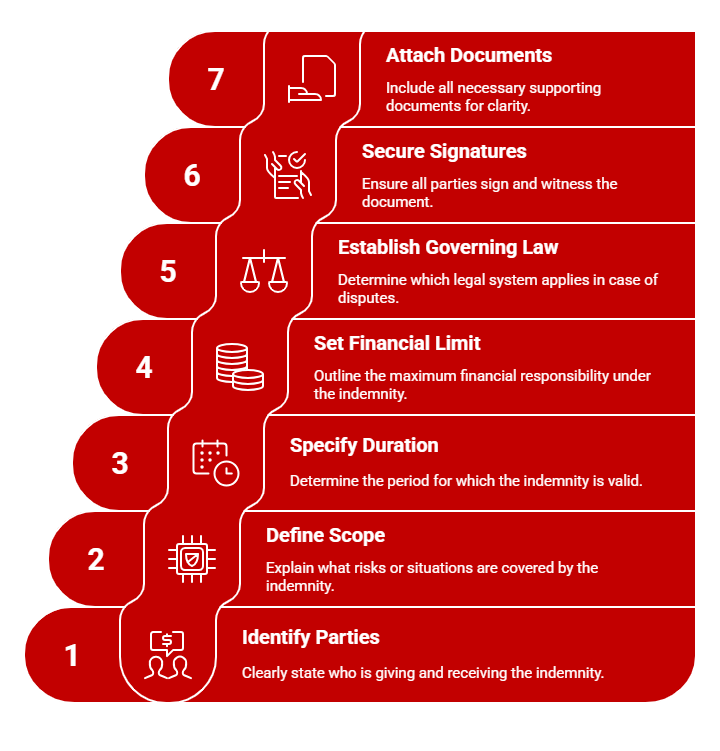

Key Elements You Must Check In A Letter Of Indemnity

Not all Letters of Indemnity offer the same level of protection. Some are clear and enforceable. Others are vague, risky, and may not hold up if something goes wrong. Before signing, it is important to review the details carefully. Understanding what should be included helps you decide whether the document is strong enough to protect your interests.

Before we look at the list, remember one thing: do not rely on assumptions. Every clause matters.

1. Parties Involved

The Letter of Indemnity must clearly state who is giving the indemnity and who is receiving it.

- Full legal names and identification must be listed

- Ensure company or developer names match official registration records

- Confirm contact details are valid and up to date

If the document does not properly identify the parties, enforcement later could be difficult.

2. Scope Of Indemnity

The document must explain what risks or situations are covered.

- What is the indemnifier responsible for?

- What type of loss or damage is included?

- What specific event or scenario triggers the indemnity?

If this scope is too vague, the protection may not be valid.

3. Duration And Validity

Every LOI must specify the duration of the indemnity.

- Does it cover until a specific date or event?

- Does it end once a problem is resolved or a document is issued?

Without a clear timeline, disputes can arise about the expiry.

4. Financial Limit And Liability

This section outlines the maximum financial responsibility.

- Is there a compensation limit?

- Does it cover legal fees and penalties?

- Are there exclusions?

A low limit may not cover actual losses.

5. Governing Law And Jurisdiction

This determines which legal system applies in the event of a dispute.

- Normally governed by Malaysian law for property matters

- Ensure it does not refer to foreign jurisdictions

This clause affects the enforceability of the indemnity.

6. Signatures And Witnessing

The LOI must be appropriately signed to be valid.

- Signatures of all parties

- Signature date clearly shown

- Official witnessing or stamping if required

Unsigned documents may not be enforceable.

7. Attachments, Supporting Documents, Or References

Some LOIs refer to other documents.

- SPA, tenancy agreement, or renovation approval forms

- Official correspondence or evidence

Always check the attached documents before signing anything.

A strong Letter of Indemnity is clear, specific, and supported with proper documentation. If anything is unclear, incomplete, or feels rushed, ask questions before agreeing. Signing without clarity may lead to financial exposure later.

Understanding the key elements helps you review an LOI confidently. Next, it is useful to know how the process works in a real property transaction.

Get Pre-Check On Your Buying Power

Know where you stand and explore homes that match your budget smoothly.

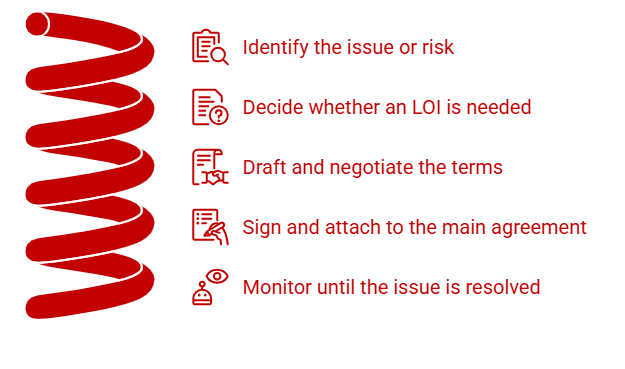

How It Works In A Property Transaction

A Letter of Indemnity follows a simple sequence in most Malaysian property transactions. Understanding the process helps you know what to expect and when to ask questions. It also shows where careful review is important before committing.

Before we look at the steps, remember that an LOI is not automatically required. It is usually requested only when risk or uncertainty exists.

Here is how a Letter of Indemnity is typically used in a property deal:

Step 1: Identify the issue or risk: For example, missing documents, unclear responsibilities, or pending approvals.

Step 2: Decide whether an LOI is needed: Both parties agree that the transaction should continue despite the risk.

Step 3: Draft and negotiate the terms: Lawyers or property professionals review the wording to ensure fairness.

Step 4: Sign and attach to the main agreement: The LOI is linked to the Sale and Purchase Agreement, tenancy contract, or bank document.

Step 5: Monitor until the issue is resolved: When the document or action is completed, the LOI expires or becomes invalid.

This process ensures that both parties understand their commitments and responsibilities from the start.

Why This Process Matters

Understanding how the LOI process works helps you:

- Know when requests are reasonable or excessive

- Decide whether signing is safe or too risky

- Avoid rushed decisions without proper checks

A Letter of Indemnity is a practical tool to keep property transactions moving when the situation is uncertain. However, it must be reviewed carefully at every step. Treat it as a legal commitment, not a routine document.

Now that you understand the process, it is important to know the real benefits of using an LOI in property deals.

What Are The Practical Benefits You Should Know?

Here are the key benefits of using a Letter of Indemnity:

- Keeps the transaction moving: It prevents unnecessary delays caused by waiting for approvals or documents.

- Provides security and peace of mind: You know who is responsible if something goes wrong.

- Reduces disputes and confusion: Responsibilities are clearly written, so misunderstandings are less likely.

- Strengthens trust between parties: Both sides show commitment to completing the deal fairly.

- Supports negotiation: An LOI can help both sides reach a compromise when expectations differ.

- Helps avoid losing a purchase opportunity: You do not risk missing a property due to timing or paperwork issues.

These advantages are the reason more people are using Letters of Indemnity in Malaysian property transactions.

Risks And Limitations You Should Be Aware Of

A Letter of Indemnity can be helpful, but it is not perfect. Many people sign quickly without asking enough questions, and that can create serious problems later. It is important to understand the risks so you can protect yourself and avoid painful surprises.

Before assessing an LOI properly, let us first look at what could go wrong.

Here are some risks you need to keep in mind:

- The terms may be unclear: If the wording is vague, it may be hard to enforce or interpret in the event of a dispute.

- The indemnifier may not be able to pay: Even if the LOI promises compensation, it will not help if the issuing party has no financial strength.

- It could conflict with another agreement: For example, the LOI may contradict terms in the Sale and Purchase Agreement or tenancy contract.

- It might not cover everything you assume: Some LOIs only cover specific losses, and you may find out too late that the coverage is limited.

- It may not be legally enforceable: Poorly drafted documents or missing signatures reduce legal strength.

A Letter of Indemnity is a strong tool when written clearly and backed by a reliable party. But when it is vague or rushed, the risk shifts onto you. Never assume the document protects you just because it feels official.

Letter Of Indemnity Vs Bank Guarantee Vs Insurance Indemnity

A Letter of Indemnity is often confused with other financial protection tools. Before we explore the details, it helps to compare them side by side in a simple way:

Who provides it

Individual, seller, landlord, tenant, or developer

Bank or financial institution

Insurance company

Main purpose

Protects against a specific risk or missing document

Ensures payment if someone fails to perform

Compensates for loss or damage based on policy

When used

To continue the transaction despite uncertainty

For high-value agreements or construction projects

For damage, accidents, or long-term risk management

Cost

Usually low or free

Bank fee applies

Insurance premium required

Strength

Depends on the financial ability of the indemnifier

Very strong and reliable

Strong if covered under policy terms

Legal enforceability

Can be weak if poorly drafted

Very secure

Depends on insurance terms and conditions

Understanding these differences prepares you to ask the right questions before signing anything. Now, let us look at how to check if a Letter of Indemnity is valid and safe to rely on.

Thinking About Signing A Letter Of Indemnity Soon?

A Letter of Indemnity is not just a formality. It has real financial and legal consequences. Take time to read it properly before signing. A quick decision can lead to problems and unexpected costs.

Take your time to read the document carefully. Ask questions. Check every clause. Make sure the terms truly protect you. If something feels unclear or unfair, stop and clarify before signing.

Having the right information helps you make confident decisions and avoid costly mistakes.

Planning to buy or sell a property soon? Make sure you understand your rights before committing to any legal documents. Explore Properties for Sale

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.