Effective from 2nd January 2015, the Base Lending Rate (BLR) system was replaced by Base Rate (BR) framework.

BR will be used as the main reference rate for new retail floating rate loan; such as mortgage, overdraft, unit trust loans, personal financing, share margin financing, which are applied for individual customers.

So what is BR? Why is there a need for change? How about the existing loans on BLR? What should we do as a borrower? All these questions will be answered as you read on.

What’s A Base Rate (BR)?

BR is a new interest framework where the interest rate charged by the bank on a loan comprised of BR and the desired spread.

The BR will be determined by the banks’ benchmark cost of funds (COF) and the statutory reserve requirement (SRR)1.

Other components such as borrow credit risk, liquidity risk premium, operating cost and profit margins will be reflected in a spread that charged on top of the BR.

This increases the visibility of the factors underlying changes to the Base Rate. The greater transparency in turn will enable more informed decision-making by consumers.

Under this cost-plus structure, spreads will always be positive as it would not be possible for financial institutions to offer lending rates below the reference rate.

Financial institutions will be given the flexibility to determine their respective benchmark rates.

The expected strong link between the Base Rate, market interest rates and the Overnight Policy Rate (OPR) will facilitate complete adjustments to retail loan repayments when market interest rates adjust to an increase or decrease in the OPR2.

Reason for the change?

“The BLR has become less meaningful as a basis for the pricing of loans, as the retail lending rates on new loans being offered by the industry are at a substantial discount to the BLR,” said Dr. Zeti3.

The BLR framework has been introduced since 1983, served as the main reference rate on consumer’s loans in Malaysia.

Since then, the determination and implementation of the BLR have evolved with the development of the financial sector.

In the recent period, however, the BLR has become less relevant as a reference rate for loan pricing, as lending rates on new retail loans are being offered at substantial discounts to the BLR3.

On top of that, BLR lack of transparency, which makes it difficult for consumers to make an informed decision.

The BR framework aims to give a better and more transparent reference rate to have a better decision by consumers in making choices among the many loans products that are offered by banks.

This BR system will be better in reflecting the changes in cost arising from monetary policy and market funding conditions while encouraging greater discipline and efficiency among financial institutions in the pricing of retail financing products.

How about the existing BLR-based loans?

The BR is used for new loans and refinancing of existing loans extended from 2 January 2015 onwards.

After the effective date, BLR-based loans prior to 2015 will continue to be referenced against the BLR.

All banks are still required to demonstrate the differences between BLR and BR for consumers.

* adapted from BNM Consumer Guide, 2nd January 2015

The diagram above illustrated how BLR and BR work. If the bank previously offered ELR of 4.85% on the loan amount, the same ELR should be offered under BR.

All banks are advised to offer the same effective lending rate with the implementation of BR in Q1 2015 by BNM.

What is an effective lending rate (ELR)?

ELR, in other words, means the interest rate that we will have to pay for the mortgage.

Each individual bank has its own way of deriving the BR and hence create a situation where the BR differs from bank to bank, unlike the old BLR where all banks applied the same rate.

However, all the rate changes can be compared with the ELR to know what is the ultimate rate adjusted by the banks. The formula is as below:

| BR + SPREAD = ELR |

For example: If BR=3.65%, Spread=0.8%

| 3.65% + 0.8% = 4.45% |

The major banks’ BR, and indicative ELR reported to BNM are as below:

Note:

* Indicative Effective Lending Rate refers to the indicative annual effective lending rate for a standard 30-year housing loan/home financing product with financing amount of RM350k and has no lock-in period. – As of 2nd January 2015 / Bank Negara Malaysia

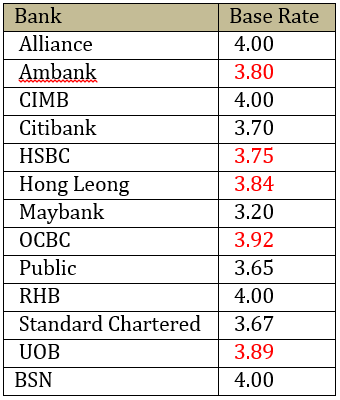

10 months have passed and the table below is the latest banks BR:

Source: based on our latest survey as of 30 October 2015

What should we do as a borrower?

- Compare the ELR quoted by different banks before taking out a new loan.

- Ask for a Product Disclosure Sheet (PDS) providing you with the ELR and total repayment amounts for the loan/financing facilities plan to take out.

- Ask the bank to explain the factors which may lead to a change in the BR.

- The monthly repayment amount will increase or decrease when there is a change in the BR.

- Assess whether you can continue to afford the loan repayments if the ELR increases in the future.

* adapted from BNM Consumer Guide, 2nd January 2015

10 interesting facts you need to know about BR!

- All revolving loans such as overdraft will need to be replaced to BR from BLR upon annual review or renewal of the loan.

- There should be no price hike with the implementation of BR at least in Q1 2015 as advised by BNM.

- If you refinance your existing loan which on BLR, your new loan will be priced on the new BR framework.

- However for any top-up loans offered under an existing housing loan reference against BLR, your existing bank may continue to use the BLR.

- The new BR framework is only applicable to loans applied by individual customers. For the pricing of other loans such as corporate or SME loans, banks have the flexibility to determine the choice of adopting the BR or continue to use the BLR.

- Banks are allowed to adjust the BR to reflect changes in market rates even though the OPR has not been advised, in the future on your loans that is referenced to BR. This is the same like BLR framework today.

- On the other hand, banks are not allowed to make changes on the spread during the financing tenure unless you do not service your monthly repayments promptly. This means the spread rate on your mortgage will remain constant throughout your mortgage tenure.

- When bank adjust the BR in the future, the same corresponding adjustment will need to be made on the BLR, by the same magnitude. Nevertheless, exception is given for the year of implementation.

- For any upwards or downwards adjustment to the BR and the BLR, banks will need to revise the monthly installment of your loans to reflects on the changes (not to revise the mortgage tenure) unless the differences in the installment amount is less than RM50 per month or by a small percentage as predetermined by the bank, whichever is lower.

- The mode of notification by the banks to you on the revised repayment amount could be in writing or via electronic means (including emails and SMS) but the banks are required to notify you at least 7 days ahead of the change in monthly installment.

References:

1 Reference rate framework, Bank Negara Malaysia, 12 December 2014

2 New Reference Rate Framework, 19 March 2014

3 BNM looks to review BLR framework, 19 December 2013

Want to learn more on how you can own a home? Our ‘Own Your Home’ programme aims to empower 100,000 Malaysian households to become homeowners by 2020. Take charge of your home ownership aspirations now!

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.