Buying a home in Malaysia involves more than just agreeing on a price. One of the most important costs to prepare for is stamp duty, and understanding stamp duty calculation can make a huge difference to your overall budget.

Whether you are purchasing your first property, upgrading to a larger place, or buying an investment unit, knowing how this tax is calculated helps you plan with confidence.

Stamp duty applies to key documents in a property transaction, and the amount you pay depends on several factors. If this is your first time navigating the process, it can feel a little overwhelming.

To make things easier, this guide breaks everything down step by step so you know exactly what you are paying for and why it matters.

Know What You Can Afford Today

Calculate your mortgage in seconds and plan confidently for your new home.

Why Stamp Duty Matters When Buying Property In Malaysia?

For many Malaysian buyers, stamp duty often feels like an extra cost that becomes noticeable only at the end of the purchase process. However, understanding it early can help you plan your finances more accurately and avoid surprises when it is time to sign your documents.

Stamp duty plays a major role in a property transaction because:

- It affects your upfront cash outlay: Stamp duty is usually paid before the transfer of ownership can be completed, so buyers need to prepare this amount in advance.

- It is tied directly to property value: As property prices increase across Malaysia, the amount of duty payable also rises.

- It applies to multiple documents: Many first-time buyers are not aware that both the transfer document and the housing loan agreement need to be stamped.

- It determines your final purchase cost: Buyers often calculate the down payment but overlook stamp duty, which can add several thousand ringgit to the total.

- It can offer meaningful savings: First-time buyer exemptions and certain Government incentives can significantly reduce the amount payable if you know how to use them.

When you know how stamp duty calculation works, you can estimate your costs more confidently, compare property options more realistically, and understand exactly how much you will need from the start to the end of the purchase.

How Stamp Duty Calculation Works: Step-By-Step Examples

Stamp duty can feel complicated at first, but once you understand how the bands work, the calculation becomes much clearer. The duty for transferring property ownership is charged progressively, which means every portion of the property price is taxed at a different rate.

To help you see how it adds up, here are simple, real-life examples that Malaysian buyers commonly encounter.

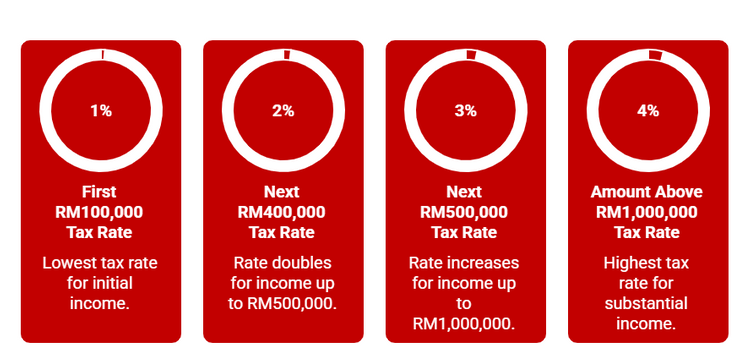

Step One: Understand the Rate Bands

Stamp duty for the Instrument of Transfer is calculated using these tiers:

These bands apply to the higher of the purchase price or market value.

Step Two: Apply the Bands to Your Property Price

Below are practical scenarios showing how the calculation works.

Example One: Property Price RM500,000

This is one of the most common price points for Malaysian homebuyers.

Breakdown:

- First RM100,000 at one per cent: RM1,000

- Next RM400,000 at two per cent: RM8,000

Total stamp duty: RM9,000

This amount is payable when the ownership transfer document is submitted for stamping.

Example Two: Property Price RM800,000

This example helps you understand how the higher bands come into play as property prices increase.

Breakdown:

- First RM100,000 at one per cent: RM1,000

- Next RM400,000 at two per cent: RM8,000

- Next RM300,000 at three per cent: RM9,000

Total stamp duty: RM18,000

This gives a clearer picture of how duty grows as you move into the higher bands.

Example Three: Loan Agreement Stamp Duty

If you are taking a home loan, the loan agreement has its own duty, calculated at 0.5 per cent of the total loan amount.

For example:

- Property price: RM600,000

- Loan amount (90 per cent financing): RM540,000

- Loan stamp duty: 0.5 per cent × RM540,000 = RM2,700

Many buyers overlook this portion, but it is an important part of your upfront costs.

Using these examples, you can now estimate your own stamp duty more accurately. In the next section, we will explore the official stamp duty rates and how they apply to different types of buyers.

First-Time Buyer Stamp Duty Exemptions

First-time homebuyers in Malaysia can benefit from stamp duty exemptions that significantly reduce the upfront cost of purchasing a residential property. These exemptions apply to both the Instrument of Transfer and the loan agreement, making them one of the most helpful incentives available to new buyers.

Full Exemption For Properties Up To RM500,000

Under the current Government initiative, Malaysian citizens buying their first residential property priced up to RM500,000 may receive a full stamp duty exemption. This means:

- No stamp duty on the Instrument of Transfer

- No stamp duty on the loan agreement

To qualify, buyers must meet the following conditions:

- The purchaser is a Malaysian citizen

- The property is a residential property

- It is the buyer’s first home purchase

- The Sales and Purchase Agreement is executed within the eligible period set by the Government.

This exemption can translate into substantial savings. For example, a first-time buyer purchasing a RM500,000 home could save RM9,000 in transfer duty, plus the loan agreement duty if financing is involved.

When The Exemption Does Not Apply

The exemption does not cover:

- Properties priced above RM500,000

- Buyers who have previously owned any residential property, even if sold

- Joint purchases where any party is not a first-time buyer

- Commercial or industrial properties

First-time buyers purchasing units above RM500,000 will pay stamp duty according to the standard tiers without exemption. For these buyers, knowing how the figures are calculated becomes even more important when planning their finances.

Understanding your eligibility early helps determine your true entry cost. Once buyers are clear on exemptions, the next important topic is penalties, especially those related to late or incorrect stamping.

How Stamp Duty Penalties Are Calculated?

Stamping your documents on time is an important part of the property purchase process. If the stamping is delayed, the Inland Revenue Board of Malaysia will impose penalties based on how late the submission is. These charges are calculated on the deficient duty, which is the amount of stamp duty that should have been paid.

Stamping Deadline

All instruments must be stamped within thirty days from the date they are executed in Malaysia. If the document is signed overseas, the timeline begins when the document arrives in Malaysia.

Submitting the documents late will trigger penalty charges, so buyers should work closely with their solicitor to avoid delays.

Penalty Rates For Late Stamping

The penalty structure is clearly defined and increases based on how long the delay is:

- Up to three months late: five per cent of the deficient duty

- More than three months and up to six months late: 10 per cent of the deficient duty

- More than six months late: 20 per cent of the deficient duty

These penalties apply to both the Instrument of Transfer and the loan agreement. Even a minor delay can result in additional costs, so it is always best to submit your documents promptly.

Common Reasons Buyers Face Penalties

Buyers may encounter penalties for several reasons, including:

- Late signing or submission of documents

- Incomplete or incorrect information provided for stamping

- Under-declaring the property value, leading to a recalculated duty

- Delays in coordinating documents between the buyer, seller, and solicitor

Understanding these penalty rates ensures buyers can avoid unnecessary costs and keep the transaction timeline on track. With penalties covered, the next part of the process is understanding how the Sales and Purchase Agreement and legal fees fit into the overall transaction.

How the SPA and Legal Fees Fit Into Your Stamp Duty Costs?

When planning your property purchase, it is helpful to understand how the Sales and Purchase Agreement (SPA) and legal fees relate to the overall costs you will incur. They are not part of the stamp duty bands, but they influence the final figure you need to prepare before the transfer can be completed.

Why the SPA Matters?

The SPA is the main contract between you and the seller. It sets out:

- The agreed purchase price

- Payment schedule

- Vacant possession details

- Defect liability terms

Even though the SPA carries a small fixed duty of RM10, it must be stamped so the agreement is legally recognised. This step sits alongside the stamping of your transfer and loan agreement.

How Legal Fees Relate to Stamping?

Legal fees cover the work your solicitor performs to prepare and process all required documents. This usually includes:

- Reviewing and finalising the SPA

- Preparing the Instrument of Transfer

- Handling the loan agreement (if you are financing)

- Submitting documents for stamping with the Inland Revenue Board

Because the solicitor handles the paperwork connected to stamp duty, these fees naturally sit within the same budgeting process.

Why Buyers Should Plan These Costs Together?

To estimate your upfront amount accurately, it helps to look at all related charges in one place:

- Stamp duty for the Instrument of Transfer

- Stamp duty for the loan agreement

- Legal fees for the SPA and loan

- Disbursements, searches, and registration fees

Considering these costs together gives you a clearer picture of the full amount needed before you receive the keys. It also helps you avoid late submission issues, which can lead to penalties of five to twenty percent of the deficient duty.

Know Your Buying Power Instantly

Wondering how much home fits your budget? Check your eligibility and plan confidently.

Common Mistakes Buyers Make With Stamp Duty

Many buyers overlook certain details when estimating their stamp duty, which can lead to unexpected costs later in the process. Being aware of these common mistakes helps you plan more accurately and avoid delays during your property purchase.

1. Relying Only on the Purchase Price

Stamp duty is calculated based on the higher of the purchase price or the adjudicated market value. Some buyers assume the price stated in the SPA is the only figure used, but if the property’s market value is higher, duty will be calculated on that amount.

2. Forgetting About the Loan Agreement Duty

Most buyers focus on the transfer duty and forget that the loan agreement also carries a 0.5 per cent duty. This can add a few thousand ringgit to your upfront cost, depending on the loan amount.

3. Not Checking Eligibility for First-Time Buyer Exemptions

First-time buyer exemptions can offer significant savings, especially for properties up to RM500,000. Buyers sometimes overlook these incentives or assume they apply automatically without checking the requirements.

4. Delaying the Stamping Process

Stamping must be completed within thirty days of signing. Delays can result in penalties of five to twenty per cent of the deficient duty, depending on how late the submission is. This is one of the most avoidable extra costs in a transaction.

5. Using Outdated Rates or Online Information

Stamp duty rates and exemptions can change. Some buyers rely on old calculators or outdated articles, which can lead to incorrect budgeting. It is always best to confirm the latest rates with your solicitor or official sources.

6. Assuming All Documents Have the Same Duty

Each document has its own duty:

- Transfer duty uses the tiered band system

- Loan duty is fixed at 0.5 per cent.

- SPA and duplicate copies carry RM10 nominal duties

Knowing which document attracts which fee helps you plan your finances more accurately.

By avoiding these mistakes, buyers can ensure their stamp duty calculation is correct and prevent any issues during the ownership transfer process.

What Buyers Should Remember in 2026?

When you know how the bands work, what documents require stamping, and how exemptions or penalties apply, it becomes easier to estimate your true upfront costs and avoid surprises during the buying process.

Taking time to check your eligibility, confirm figures with your solicitor, and keep track of deadlines can make your purchase much smoother.

If you are preparing to buy a home this year, explore more tips and detailed guides in the PropertyGuru Malaysia Guides section to help you make informed decisions throughout your property journey.

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.