Life’s getting more expensive in Malaysia, from daily groceries to fuel, everything seems to be rising in cost. Perhaps the most daunting challenge many face today is owning a home. Property prices in major cities, particularly the Klang Valley, remain high, and with interest rates, construction costs, and inflation all playing a role, owning a home seems like a distant dream to many.

But not all hope is lost. Thanks to a variety of affordable housing malaysia schemes introduced and supported by both the public and private sectors, home ownership is more achievable than it might seem. These schemes aim to bridge the gap, especially for the B40 and M40 income groups, by lowering the entry barrier to property ownership.

In this guide, we’ll break down the current landscape of affordable housing malaysia as of 2026. You’ll learn where the schemes stand now, the pros and cons, what to watch out for, and how to decide if applying for one is right for you.

What Is "Affordable Housing" in Malaysia?

Affordable housing typically refers to housing units that are priced, financed, or subsidised so that lower or middle-income households can realistically afford them without compromising basic living standards.

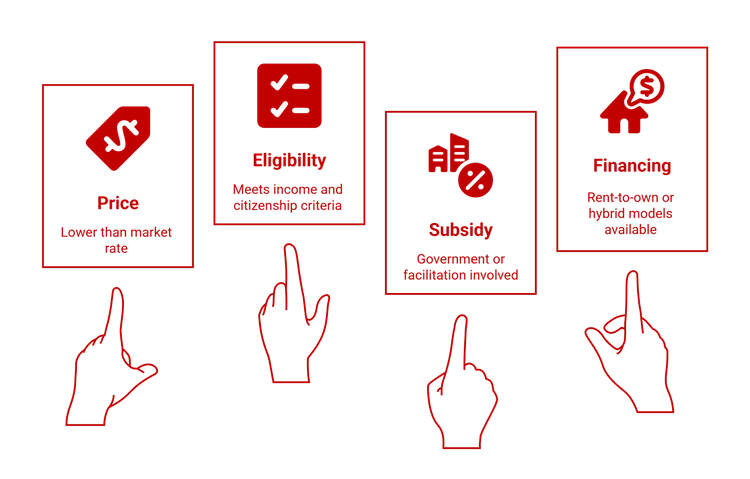

In Malaysia, affordable housing often means:

- A sale price that’s substantially lower than the typical market-rate new developments

- Eligibility criteria based on household income, citizenship, and other requirements

- Some form of subsidy, government involvement, or facilitation to make units more accessible

- Possibility for rent-to-own, or other hybrid financing models

Over the years, several government and developer-led affordable housing programmes have been rolled out to meet growing demand.

In 2026, these schemes remain highly relevant and, in some cases, are evolving.

Key Affordable Housing Schemes in Malaysia

Here are the most commonly used and widely recognised schemes available today (or very recently) to support affordable home ownership:

PR1MA (1MalaysiaPeople’ss Housing)

Household incomes approx RM2,500 – RM15,000 (varies by location)

RM150,000 – RM500,000+ (depending on location and project)

Large-scale development, mixed urban locations, some resale, low down payment options

Residensi Wilayah (RUMAWIP)

Urban households (e.g., Kuala Lumpur) often capped Rat M10,000 – RM15,000

RM200,000 – RM400,000+

City-centric, designed for working professionals in KL/Putrajaya/Federal territories

Rumah Selangorku

Selangor residents, income cap varies (e.g., < RM10,000)

RM240,000 – RM350,000+

State-level affordable housing with a variety of unit types

New Budget 2025

Low- to middle-income Malaysians

Varies by project

Public-private partnerships, community-centric developments, mixed residential types

PR1MA Rent-to-Own

Those who can’t immediately afford a down payment

Availability varies by project; not offered for every PR1MA development each year

A rent-to-own structure where part of the monthly rent contributes towards eventual ownership

Note: Price ranges are based on recent PropertyGuru, developer, and government scheme data as of mid-2025. Always check current project listings before applying.

Taken together, these schemes form the core pathways for Malaysians seeking attainable homeownership, offering structure and realistic entry points for buyers who want stability without overstretching their finances.

Pros of Affordable Housing Schemes

Before weighing affordability against compromises, it helps to understand the genuine advantages these schemes offer to first-time buyers and long-term planners.

Pros:

- Lower Entry Price

- Compared to typical market-rate new launches, especially in the Klang Valley, affordable housing units can be priced significantly lower. For many schemes, you’re not paying the speculative premium.

- This makes it financially feasible for B40/M40 buyers to own property rather than rent indefinitely.

- Compared to typical market-rate new launches, especially in the Klang Valley, affordable housing units can be priced significantly lower. For many schemes, you’re not paying the speculative premium.

- Reduced Down Payment & Easier Financing

- Many schemes are supported by government or quasi-government bodies, which may facilitate lower down-payment requirements or offer favourable financing.

- Rent-to-own models (e.g., rent-to-own) allow renters to pay toward equity before full ownership.

- Many schemes are supported by government or quasi-government bodies, which may facilitate lower down-payment requirements or offer favourable financing.

- Purpose-Built for First-Time Homebuyers

- These programmes often target first-time homeowners, young couples, and young adults. Rather than paying high rent, these buyers can invest in a property that they can grow into and own.

- The design of many affordable housing projects balances size, functionality, and cost; they may not be luxury flats, but they are practical and decent-sized.

- These programmes often target first-time homeowners, young couples, and young adults. Rather than paying high rent, these buyers can invest in a property that they can grow into and own.

- Community and Social Planning

- Many affordable homes are located in mixed-use or well-planned townships, where schools, public transportation, shops, and other amenities are integrated or nearby.

- This planning supports strong community ties, walkability, and better liveability for low- to middle-income buyers.

- Many affordable homes are located in mixed-use or well-planned townships, where schools, public transportation, shops, and other amenities are integrated or nearby.

- Long-Term Asset Building

- Even if the home isn’t premium, owning a property is a long-term investment. For many, affordable housing is a way to build equity, leverage future loans, or even upgrade later.

- In some schemes, there is a provision for resale (with conditions), which means you could potentially benefit from capital appreciation.

- Even if the home isn’t premium, owning a property is a long-term investment. For many, affordable housing is a way to build equity, leverage future loans, or even upgrade later.

Taken together, these benefits demonstrate why affordable housing schemes continue to play a crucial role in helping Malaysians transition from renting to owning a home, without overstretching their finances.

Cons & Risks of Affordable Housing Schemes

While the appeal of affordable housing is clear, it’s equally essential to understand the limitations and trade-offs that come with these schemes.

Cons:

- Smaller or Less Strategic Locations

- Affordable housing developments are sometimes located further from city centres or major economic hubs. While that helps affordability, it may mean longer commuting times.

- In some cases, projects close to transport hubs still command higher prices due to convenience, meaning" affordable"e" is relative.

- Affordable housing developments are sometimes located further from city centres or major economic hubs. While that helps affordability, it may mean longer commuting times.

- Quality Trade-Offs

- Because costs are kept low, the quality of materials, finishing, and artistry may not match that of high-end private developments.

- Facilities may be more limited (e.g., fewer swimming pools, gyms, or communal green areas).

- Overcrowding risk: With many targeting low- to mid-income buyers, maintenance and standard facilities can come under pressure if not well managed.

- Because costs are kept low, the quality of materials, finishing, and artistry may not match that of high-end private developments.

- Application Complexity

- Balloting processes are standard; simply applying doesn’t guarantee you’ll secure a unit.

- Waiting lists can be long. Being selected in a ballot does not always translate into an immediate purchase; some people wait for months or even years.

- There may be strict eligibility criteria, including income checks, citizenship status, and prior property ownership.

- Balloting processes are standard; simply applying doesn’t guarantee you’ll secure a unit.

- Resale Restrictions

- Some schemes have lock-in periods: you may be prohibited from selling or transferring the property for a specified period without approval.

- There may be resale controls in place to prevent the property from being sold to investors at premium rates, which can limit your flexibility.

- Some schemes have lock-in periods: you may be prohibited from selling or transferring the property for a specified period without approval.

- Long-Term Value Uncertainty

- If the project is in a less developed or suburban location, capital growth may be slower than in prime or highly gentrifying areas.

- While affordability is the immediate benefit, long-term market risk must be balanced: a lower price does not guarantee rapid appreciation.

- If the project is in a less developed or suburban location, capital growth may be slower than in prime or highly gentrifying areas.

Being aware of these challenges allows you to approach affordable housing with realistic expectations, ensuring your decision is guided by both opportunity and caution.

How to Evaluate Whether an Affordable Housing Scheme Is Right for You?

To determine whether an affordable housing scheme genuinely suits your situation, it helps to break down the decision into the essentials that matter most for long-term ownership.

Here are key factors to assess:

- Eligibility

- Confirm your household income qualifies under the housing scheme you are considering (B40/M40 cutoffs may vary).

- Check citizenship, permanent resident status, and other scheme-specific requirements (e.g., first-time buyer conditions).

- Confirm your household income qualifies under the housing scheme you are considering (B40/M40 cutoffs may vary).

- Project Credibility

- Research the developer: track record, on-time delivery, and build quality.

- Verify whether the project has an approved Sales & Purchase Agreement (SPA) and whether a TOP (Temporary Occupation Permit) has been or will be granted.

- Research the developer: track record, on-time delivery, and build quality.

- Location & Connectivity

- Consider proximity to public transport (MRT/LRT), major roads, employment hubs, and amenities.

- A home far away, although cheap, may cost more in terms of travel, time, and lost opportunities.

- Consider proximity to public transport (MRT/LRT), major roads, employment hubs, and amenities.

- Financing Options

- Speak to banks or financial advisors to explore whether the developer or scheme offers special financing, or whether general property loans apply.

- Clarify what down payment is required and whether there are grants or subsidies available to help you access them.

- Speak to banks or financial advisors to explore whether the developer or scheme offers special financing, or whether general property loans apply.

- Resale Terms

- Read the fine print: Is there a minimum holding period before you can sell? Are there "affordable housing resale restrictions"s"?

- Understand whether capital gains from these homes are capped, or whether you must sell at controlled prices.

- Read the fine print: Is there a minimum holding period before you can sell? Are there "affordable housing resale restrictions"s"?

- Maintenance & Management Costs

- Affordablhomes’s maintenance fees (sinking fund, management fees) can vary widely.

- Confirm the charged per square foot or per unit, and whether there are plans to increase service levels or amenities in the future.

- Affordablhomes’s maintenance fees (sinking fund, management fees) can vary widely.

- Economic Growth & Demand

- Consider long-term demographic and infrastructure trends: Is the township growing? Are there nearby MRT lines planned?

- For investment purposes, check demand from rental market segments such as young professionals and students in the area.

- Consider long-term demographic and infrastructure trends: Is the township growing? Are there nearby MRT lines planned?

Once you’ve evaluated these core factors, you’ll have a far clearer sense of whether the scheme aligns with your budget and homeowner plans.

Estimate your monthly repayments with ease

Understand your financing range before you commit.

Real-Life Examples of Affordable Housing Projects

Here are three scheme-based affordable housing projects to watch or consider in 2026:

- PR1MA Projects: For example, in Johor or Perak, PR1MA developments remain among the most affordable in terms of price and financing.

- Residensi Wilayah (RUMAWIP): In Kuala Lumpur and Putrajaya, this supports working citizens with moderate incomes who want city living.

- Rumah Selangorku: For Selangor residents, this scheme has been very popular in mature townships, with good transport and amenities.

Together, these examples demonstrate how Malaysia’s affordable housing ecosystem continues to provide diverse and accessible pathways to homeownership for eligible buyers in 2025.

Is Affordable Housing Still Worth It in 2026?

Before deciding whether affordable housing is the right path for you in 2025, it helps to be clear about the type of buyer who genuinely benefits from these schemes.

- You want homeownership, not just renting, but you’re not ready or able to stretch into premium condos.

- You plan to live in the property long-term (five years or more), so capital appreciation and stability are important considerations.

- You are okay with more modest finishes and slightly limited facilities, in exchange for a much lower entry cost.

- You are eligible for the scheme and understand its conditions (resale restrictions, waiting list risk, etc.).

- You want to minimise risk, you’re comfortable doing due diligence on the developer, location, and financial structure.

If these points reflect your situation and long-term priorities, affordable housing remains one of the most practical and financially grounded routes into Malaysian homeownership in 2026.

Next Steps

Affordable housing in Malaysia remains a powerful enabler of property ownership. With the right approach, applying for one of these schemes can put you on the path to owning a home without overextending your financial resources.

Recommended Next Actions:

- Browse PropertyGuru’s affordable housing listings, use filters like" 40/PR1MA/RUMAWIP/affordable" to find real, active projects.

- Use a loan calculator to calculate your home loan and monthly obligations, and determine whether the monthly cost is sustainable in the long term.

- Reach out to developers or scheme offices to request the latest eligibility criteria, SPA samples, and resale rules.

- Visit shortlisted developments in person to walk through the units, assess the build quality, and speak with existing or prospective residents.

Owning a home is more than just a financial step; it is a long-term commitment, and for many Malaysians in 2026, affordable housing schemes are available.

Check PropertyGuru’s housing guides to find a realistic, structured approach to making that commitment wisely.

Keep Track of New Launches

Visit our new launches page to find the new launch project of your dreams and submit an enquiry today.

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.