Buying a home is one of the most significant financial milestones many Malaysians will ever achieve, especially for first-time buyers. However, the excitement of owning a place can quickly be dampened by the upfront "entry" costs associated with taking out a mortgage, including legal fees, valuation, stamp duty, and more.

If not planned for, these costs can add up to a substantial sum at an inconvenient time. This is where the Zero Moving Cost (also known as Zero Entry Cost) home loan becomes a game-changer.

In 2026, as interest rates ease and banks compete for mortgage business, this type of financing deserves a fresh look. Below, we break down precisely what zero moving cost packages are, how they work, their benefits, potential downsides, and whether they make sense for you in today’s economic climate.

Discover rental opportunities near you.

Compare prices and shortlist what fits best.

What Is a Zero Moving Cost Home Loan?

A Zero Moving Cost (ZMC) home loan means the bank absorbs many of the upfront costs typically borne by the buyer. Instead of paying for legal fees, valuation costs, and stamp duties out of pocket, these expenses are covered by the bank as part of the loan package (subject to the terms).

To understand how these packages actually work in practice, here are the key components:

- Example provider: CIMB’s official Zero Moving Cost package covers legal fees, valuation, and stamp duties for property financing of completed homes.

- Eligibility: According to CIMB, the property must be fully completed, and the financing amount should be between RM200,000 and RM3,000,000 for residential properties.

- Financing margin: For example, CIMB’s HomeFlexi Smart plan under its ZMC package allows financing of up to 90% + 5% for costs such as MRTA. Effective up to 95%, including entry costs, which include legal and valuation fees.

- Islamic version: CIMB Islamic’s HomeFlexi Smart-i is typically structured with features similar to its conventional counterpart; however, detailed confirmation of Zero Moving Cost coverage for legal and valuation fees in 2025 is not explicitly stated in publicly available sources. (Buyers should verify the latest terms directly through CIMB Islamic brochures or official channels before proceeding.)

- Bank-lock or conditions: Some ZMC packages are structured as campaigns. For instance, HSBC’s 2025 "Bank Pay Costs" Zero Moving Cost campaign covers legal, stamp, and valuation fees, subject to certain limits.

Taken together, these features demonstrate why Zero Moving Cost financing has become one of the most attractive entry pathways for buyers seeking to reduce upfront expenses without delaying their transition into homeownership.

Why Zero Moving Cost Is More Attractive Now?

Zero-movement-cost packages have become increasingly appealing to Malaysian homebuyers in 2026, especially amid shifting interest rates, rising living expenses, and stronger competition among lenders.

Several key factors explain why these plans are gaining traction:

1. Lower Interest Rate Environment

The attractiveness of zero-moving-cost options is closely tied to the current lending climate. In July 2025, Bank Negara Malaysia (BNM) reduced the Overnight Policy Rate (OPR) from 3.00% to 2.75%, making borrowing cheaper across the board.

- Lower OPR translates to more affordable floating-rate and base-rate home loans.

- Because financing costs have decreased, rolling your upfront expenses, such as legal fees, stamp duty on loan agreements, and valuation charges, into your mortgage now carries a smaller long-term financing burden.

- In simple terms, the "price" of letting the bank absorb your entry costs has gone down, making these packages more cost-efficient than in previous years.

2. Improved Cash Flow at the Point of Purchase

Zero-movement cost packages are particularly beneficial for buyers who want to preserve cash during the costly transition to a new home.

By allowing the bank to fund your legal fees and valuation costs, you can retain more of your own money for:

- Renovations and interior upgrades

- Essential furniture and appliances

- Moving expenses

- Emergency liquidity and financial stability

In a period where household budgets are stretched, having additional cash on hand at completion provides both practical and psychological relief.

3. Growing Competition Among Banks

Another factor driving the popularity of zero moving cost packages is the increasing competition in the mortgage market. As homebuyers become more price-sensitive and cautious with financial commitments, banks are responding with more attractive, incentive-driven loan products.

- While CIMB is often highlighted for its strong zero moving cost offering, other banks, including HSBC, are actively promoting similar campaigns.

- This competitive environment provides borrowers with more opportunities to compare, negotiate, and secure better terms or flexible structures that align with their financial goals.

As these trends converge, zero moving cost options stand out as one of the most advantageous entry strategies for Malaysian buyers navigating today’s housing landscape.

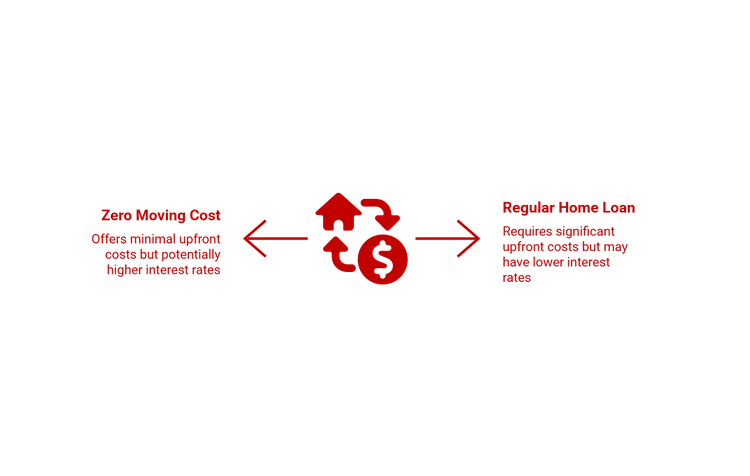

Zero Moving Cost Home Loan vs Regular Home Loan

To help you gauge whether a Zero Moving Cost home loan genuinely aligns with your financial priorities, the comparison below breaks down how it stacks up against a regular mortgage across all major cost components in 2025:

Upfront Legal Fees

Paid by bank (subject to caps and eligible documents).

Paid by buyer (RM4,000 – RM10,000 depending on loan size).

Stamp Duty on Loan Agreement

Often covered by the bank in ZMC packages (varies by bank).

Paid by buyer (0.5% of loan amount).

Valuation Fee

Paid by the bank under ZMC packages.

Paid by buyer (RM600 – RM2,000 depending on property value).

Entry Cost (Total Cash Needed Upfront)

Very low (the bank subsidises the majority of entry costs).

High (typically RM7,000-RM20,000 upfront).

Interest Rate/Effective Cost

Usually slightly higher BR + margin because the bank subsidises costs.

Usually lower because the buyer absorbs all entry costs.

Lock-In Period

More likely (e.g., 3-5 years, varies by bank).

Sometimes, none or shorter; it depends on the package.

Eligibility

Often limited to completed homes; minimum financing, e.g., RM200k – RM3m (CIMB).

Wider eligibility across properties and loan sizes.

Financing Margin

Often up to 90% + 5% for costs like MRTA

Typically, 90% for first home buyers.

Ideal For

Buyers with limited cash upfront/first-time buyers prioritising liquidity.

Buyers want the lowest long-term interest cost.

Long-Term Cost

Higher due to interest charged on a larger financed amount.

Lower over the entire loan tenure due to a smaller financing base.

Short-Term Cash Flow

Substantial, minimal upfront burden.

Weaker, heavy upfront cost.

Example (2025)

CIMB Zero Moving Cost (legal + valuation + stamp duty covered) • HSBC Zero Moving Cost Campaign (subject to caps).

Standard mortgage packages from all major banks.

Viewed side by side, the differences are apparent: Zero Moving Cost packages ease the immediate financial pressure, while regular home loans reward buyers who can afford higher upfront payments with better long-term savings.

Work out your loan instalments quickly.

Stay within a budget that fits your lifestyle.

Pros of Zero Moving Cost Loans

Here are the key advantages of going for a ZMC home loan:

- Reduced Burden at Signing: No need to pay hefty upfront legal or valuation fees. This is particularly helpful for first-time buyers who might not have significant savings.

- Better Liquidity for Move-In Needs: The cash you save can be used for renovations, furniture, or simply kept as a buffer.

- Higher Financing Margin: Many ZMC loans allow for very high financing, sometimes up to 95%, which reduces the cash you need to bring in.

- Flexibility in Repayment: In plans like HomeFlexi Smart, you may be able to make extra repayments or redraw, giving you more control over your cash flow.

- Access to Beneficial Campaigns: With bank promotions, you might score very favourable terms (including legal and valuation borne by the bank), especially if you time your application right.

Taken as a whole, these benefits position ZMC financing as a smart entry point for buyers who value liquidity and prefer to keep their upfront commitments lean.

Cons to Consider

However, ZMC loans aren’t risk-free or perfect for everyone. Here are key disadvantages to watch out for:

- Higher Cost via Interest

Since the bank is covering the entry costs, the "cost" is simply rolled into your monthly repayments, often as a slightly higher margin or rate. - Lock-in Period

Some packages may have a lock-in period or stricter terms around refinancing or early repayment. Please read your Letter of Offer carefully. - Not Universally Available

Not all banks offer ZMC loans so product choices may be more limited. - Coverage Limits

Even under "zero" schemes, there may be caps: for example, HSBC’s ZMC campaign covers legal and valuation, but only up to a point. - Long-Term Interest Burden

Although your cash flow is better at the start, over a long financing tenure (e.g., 30-35 years), the extra interest could be significant.

When weighed carefully, these drawbacks serve as a helpful reminder that ZMC loans work best for buyers who prioritise liquidity over the lowest possible lifetime cost.

Is a Zero Moving Cost Home Loan Right for You?

Before you commit, it’s worth taking a step back to consider how a ZMC package aligns with your financial habits, long-term plans, and the level of flexibility you expect from your mortgage.

Here are scenarios where a ZMC loan makes absolute sense, and some where you should be more cautious.

Good Fit When:

- You’re a first-time homeowner and want to minimise your upfront cash outlay.

- You don’t have a large savings buffer, but plan to invest in the property (furniture/renovation) once you move in.

- You’re comfortable paying a slightly higher interest rate today in exchange for convenience.

- You want flexible repayment options and may be able to make extra repayments in the future.

Be Careful When:

- You plan to sell or refinance very soon, and you don’t want to pay the "carried cost" of higher interest.

- You prefer a fixed-rate loan and want to lock in the lowest possible interest.

- If you’re unsure about long-term cash flow, the "monthly convenience" might actually cost you more in interest.

Ultimately, the best choice is the one that strikes a balance between today’s convenience and tomorrow’s cost. When you understand how a ZMC loan shapes both your cash flow and future options, the decision becomes far more straightforward and far more strategic.

How to Apply for a ZMC Home Loan?

Applying for a Zero Moving Cost loan is straightforward, but it pays to approach the process methodically. Hence, you understand precisely what the bank is covering and what you’re ultimately signing up for.

- Check Bank Offers and Campaigns

- Visit bank websites to compare their ZMC packages (e.g., CIMB’s Zero Moving Cost page).

- Ask specifically about their "zero-entry-cost zero entry-cost / zero moving-cost" loans, as not all mortgage advisers mention this by default.

- Visit bank websites to compare their ZMC packages (e.g., CIMB’s Zero Moving Cost page).

- Calculate Total Cost

- Use a home loan calculator to model your monthly repayments with the ZMC package and compare them to those of a regular home loan.

- Factor in the value of what the bank is paying (legal, valuation, stamp duty) vs how much more you’ll pay in interest over the life of the loan.

- Use a home loan calculator to model your monthly repayments with the ZMC package and compare them to those of a regular home loan.

- Confirm Eligibility

- Confirm minimum loan amounts: for example, CIMB requires a minimum of RM200,000 for its ZMC package.

- Ensure your property qualifies (must be completed in accordance with CIMB’s terms).

- Confirm minimum loan amounts: for example, CIMB requires a minimum of RM200,000 for its ZMC package.

- Read the Terms & Conditions

- Look out for lock-in clauses, prepayment rules, interest rate adjustments, and whether the "free cost" covers everything (some packages exclude specific legal work).

- For HSBC’s ZMC campaign, read the full terms and conditions (T&C), which detail precisely what is borne by the bank and where the limit applies.

- Look out for lock-in clauses, prepayment rules, interest rate adjustments, and whether the "free cost" covers everything (some packages exclude specific legal work).

- Apply & Negotiate

- When you’re ready, apply for the ZMC package through the bank branch.

- Negotiate, some costs might not be fully covered if they exceed bank caps, so you may need to contribute in some cases.

- Make sure the bank issues your Offer Letter clearly stating the ZMC package details (costs, caps, lock-in, etc.).

- When you’re ready, apply for the ZMC package through the bank branch.

Handled carefully, the application process becomes more than a simple checklist; it’s your chance to secure clarity, certainty, and the most favourable terms for your long-term financial comfort.

Is "Zero Moving Cost" Worth It in 2026?

In today’s market, with a lower OPR and intense competition among banks, Zero Moving Cost home loans are more attractive than ever.

If your main pain point is the large lump-sum payment at the start of your home purchase, a ZMC package can significantly ease your burden and help you preserve cash for more critical expenses, such as renovations or furniture.

That said, it’s not a "free lunch." While you avoid paying legal, valuation, and stamp duties upfront, you should be comfortable paying a bit more in monthly repayments over time.

If your priority is short-term cash flow and you plan to stay in the home for the long haul, ZMC could be a smart move.

Explore Malaysia’s latest property listings on PropertyGuru and take the next step towards securing a stronger, safer rental portfolio.

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.