If you plan to take a home loan this year, you may notice that interest rates change more often than before. In 2025, the Standardised Base Rate (SBR) for all major banks is 2.75 per cent per annum, and this figure plays a major role in how much you will pay each month. Many buyers still struggle to understand the SBR meaning, how the rate is set and why banks can offer different final rates even when the SBR is the same.

Floating-rate loans can feel confusing, especially when instalments rise after an OPR adjustment. Without knowing how the SBR works, it becomes harder to plan your budget or compare loan packages with confidence.

This article explains what the SBR is, how it works in 2025 and 2026, and what you should look out for when choosing a home loan.

Ready To Buy? Check Your Eligibility

Take the first step toward owning a home by knowing how much you can borrow.

SBR Meaning: Understanding the Standardised Base Rate

Before looking at how banks price home loans, it is important to understand what the Standardised Base Rate means. Knowing the SBR meaning helps you see why loan rates change and how banks decide what to charge.

The SBR is the reference rate used by all banks in Malaysia for floating-rate home loans. Bank Negara Malaysia introduced it in August 2022 to replace the old Base Rate system. Unlike before, the SBR is now the same across all banks, which makes comparisons easier for homebuyers.

The SBR is tied directly to the Overnight Policy Rate (OPR). When the OPR moves, the SBR will move in the same direction. This makes the SBR a clear reflection of current monetary policy and a key starting point for your final loan rate.

To better understand this, here are the main points that define the SBR.

- SBR is a standard reference rate used by all banks

- It follows the OPR set by Bank Negara Malaysia

- It moves in the same direction and amount as the OPR

- It is the base used to calculate your home loan interest rate

- It allows easier comparison of loan packages between banks

With these basics covered, it becomes easier to see how SBR fits into Malaysia’s home loan system and why the spread each bank adds matters. We will explore that next.

How SBR Works in Malaysia’s Home Loan System?

Now that the basics are clear, it’s helpful to understand how SBR fits into Malaysia’s home loan structure. This will give you a clearer picture of how banks calculate your rate and why your monthly instalment may change over time.

The SBR acts as the starting point for all floating-rate home loans in the country. Every bank begins with the same SBR, then adds its own margin based on risk, loan type and internal pricing policies. This is why your final interest rate can differ from one bank to another, even though the SBR remains standard.

Let’s break this down further through the key components.

The Calculation Formula and How It Works

Every floating-rate home loan in Malaysia follows one simple formula. Understanding this formula makes it easier to compare loan packages and estimate long-term affordability.

Here is a quick transition before the breakdown.

The formula looks simple, but each part carries important meaning.

- Effective Lending Rate (ELR) = SBR + Spread

- SBR: The standard reference rate used by all banks

- Spread: The bank’s margin based on borrower risk, loan features and internal costs

The SBR is fixed across banks. The spread is not. This is why two banks can show the same SBR but offer different final interest rates.

Buyers with a stable income, good repayment history and lower risk usually qualify for a lower spread. Meanwhile, buyers with higher risk may receive a wider margin. This difference can create a significant impact on monthly instalments and total interest paid.

Why do All Banks Use the Same SBR, But Your Loan Rate Still Varies?

Many homebuyers assume standardisation means identical loan rates everywhere. However, the SBR only standardises the base rate, not the final rate.

The part that creates variation is the spread, not the SBR. Banks calculate spreads based on several factors:

- Risk profile of the borrower

- Loan-to-value ratio

- Loan tenure

- Type of property

- Internal funding cost and product strategy

Because spreads differ, two borrowers applying for the same loan amount can end up with very different effective lending rates.

For example, Bank A and Bank B may both show an SBR of 3%. But if Bank A adds a spread of 1.2 per cent and Bank B adds a spread of 1.5 per cent, the final rates will differ. This is why comparing spreads is just as important as checking the base rate.

Recent OPR Changes, SBR Movements and What Borrowers Should Watch

To understand how the SBR behaves in 2025 and beyond, it helps to look at what has happened with the Overnight Policy Rate in the last few years. Since SBR moves exactly in line with the OPR, any shift in monetary policy will affect home loan rates almost immediately.

The OPR was adjusted several times after the pandemic period, moving from a historically low level back toward a more stable range. These increases pushed the SBR higher, thereby raising the effective lending rates banks offered. As a result, many borrowers noticed higher monthly instalments or tighter affordability assessments during loan applications.

Here is a clearer look at what these changes mean for borrowers today.

- The OPR is now closer to its pre-pandemic level, which means the SBR has also normalised

- Higher SBR levels make floating-rate loans more sensitive to future rate changes

- Even a small OPR adjustment can increase monthly instalments, especially for long tenures

- Buyers who borrow near their maximum eligibility may face stricter evaluations from banks

Because the SBR closely follows the OPR, any future rate hike or cut will affect the affordability of floating-rate loans. This makes it important for buyers to track monetary policy updates and understand how these decisions may influence their long-term repayment plans.

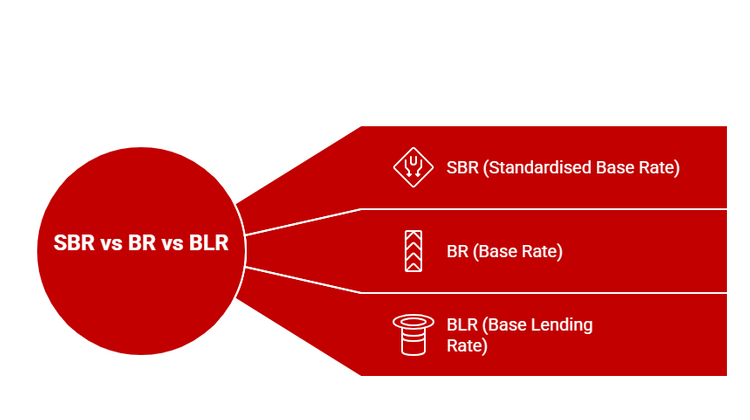

SBR vs BR vs BLR: What Has Changed for Borrowers?

Before we look at how the current system affects homebuyers, it’s important to understand how Malaysia transitioned from BLR to BR and finally to SBR.

Each reference rate was introduced to improve transparency, and knowing these differences makes it easier to see why comparisons are more simple today.

Malaysia used the Base Lending Rate (BLR) for many years. In 2015, it was replaced by the Base Rate (BR). Then, in August 2022, Bank Negara Malaysia introduced the Standardised Base Rate (SBR) to create a fully consistent reference rate across all banks. This change has made loan pricing clearer and easier to compare, especially for floating-rate home loans.

To see how these systems differ, here is a simple comparison.

Key Differences Between SBR, BR and BLR

This table provides a quick overview of how each reference rate operated and why SBR offers a more transparent structure today.

BLR

Set internally by each bank

Not transparent, varied widely

Harder to compare loan packages

BR

Based on each bank’s benchmark cost of funds

More structured but still different for each bank

Comparisons improved but still inconsistent

SBR

Directly linked to the OPR

Fully standardised across all banks

Easier comparisons and clearer pricing

This shift matters because it standardises the starting point for all floating-rate home loans. Under the BLR and BR systems, banks used different reference rates, which made comparisons difficult. With the SBR, every bank begins with the same base rate, and the only variation now comes from the spread added on top of it.

Borrowers with older BLR or BR loans will continue using their original structure. These loans still move in line with OPR changes, so monthly instalments may increase or decrease when the OPR is adjusted.

How SBR Affects Your Home Loan Repayments in 2026

Before looking at loan comparisons, it helps to understand how the SBR affects your monthly instalments. This will give you a clearer idea of what may change if interest rates move in the future.

The SBR is the base rate for floating-rate home loans. When the SBR increases, your loan’s effective lending rate increases as well. This causes your monthly instalments to rise. The opposite happens when the SBR decreases. Because the SBR follows the OPR, every change in the OPR will affect your repayment amount.

How Changes in SBR Affect Monthly Instalments

Here is a simple breakdown to show how sensitive floating-rate loans are to SBR changes.

- A higher SBR means a higher effective lending rate

- Monthly instalments will rise when the SBR increases

- Instalments will fall when the SBR is reduced

- Longer loan tenures feel the impact more

- Borrowers with tight budgets may experience strain when rates rise

This is why many buyers choose to calculate their loan based on slightly higher rates, just to prepare for future OPR adjustments.

Simple Examples Based on Common Loan Amounts

A short example makes this easier to understand. The figures below assume a 30-year tenure and a small increase in the effective lending rate.

These examples show how a small rate change affects monthly instalments.

RM300,000

~RM1,432

~RM1,476

+RM44

RM500,000

~RM2,387

~RM2,459

+RM72

RM800,000

~RM3,819

~RM3,934

+RM115

Even a small 0.25 per cent increase can affect your budget over time. This is why it is important to leave some room in your affordability.

What Borrowers Should Watch in 2025 and 2026?

Here is a short transition before highlighting the key points.

These are the main things to monitor if you are taking a floating-rate loan.

- OPR announcements from Bank Negara Malaysia

- Your current debt-to-income ratio

- Whether the bank’s spread will change based on your profile

- Loan features such as flexi or semi-flexi options

- Your overall repayment buffer in case rates rise

Understanding how the SBR affects your loan makes it easier to plan ahead and choose a package that suits your financial goals.

How To Compare Home Loans Using SBR?

Before choosing a home loan, it is important to know what to compare. Since the SBR is the same across all major banks, the difference in loan pricing comes from other factors. Understanding these elements will help you compare packages more accurately and avoid surprises later.

Focus on the Effective Lending Rate (ELR)

The ELR is the final rate you will pay after the bank adds its spread to the SBR. Since the SBR is fixed at 2.75 per cent per annum in 2025, the spread becomes the key part that varies between banks.

Here is a short transition before the main points.

These are the reasons the ELR should be your main comparison point.

- It reflects the total interest you will pay

- It includes both the SBR and the bank’s spread

- It gives a clearer picture of the long-term cost

- It is easier to compare across banks than the raw SBR

When comparing loan packages, always place the ELR at the top of your checklist.

Why the Spread Makes the Biggest Difference

The spread is the bank’s margin added to the SBR. It varies based on your income stability, loan amount, property type and overall risk profile.

Here is a simple transition before the list.

These factors often influence the spread offered by banks.

- Your credit score and repayment history

- Debt-to-income ratio

- Loan amount and tenure

- Type of property (residential or investment)

- Bank’s current lending strategy

- Your employment stability

Two borrowers can receive very different spreads even at the same bank. This is why understanding your financial profile can help you negotiate or choose a more suitable loan.

Use the Product Disclosure Sheet (PDS)

Every bank publishes a Product Disclosure Sheet that explains the ELR, fees and repayment details. This is one of the most reliable tools for loan comparison.

Here is a short transition before the key points.

The PDS helps you compare:

- Indicative ELR

- Total repayment amount

- Possible fees or charges

- Lock-in period

- Instalment calculations

Always review the latest PDS before making a decision, as these figures change when the OPR or bank pricing is revised.

Example: How Two Banks Can Offer Different Final Rates

A short illustration helps make this clearer. The numbers below are simplified to show how spreads affect the final rate.

Bank A

2.75%

1.25%

4.00%

Bank B

2.75%

1.50%

4.25%

The SBR is the same.

The difference comes from the spread.

This affects how much interest you pay over the life of the loan.

What To Look Out For When Comparing Loans?

Here is a clear transition before the checklist.

These are the key things to review before choosing a package.

- Final ELR after the spread

- Monthly instalment at current rates

- Impact of a 0.25 per cent rate increase

- Loan tenure and total interest payable

- Lock-in period and early settlement fees

- Whether the loan is flexi or semi-flexi

- Any promotional conditions attached

A clear comparison helps you choose a loan that matches both your current budget and your long-term financial plans.

Plan Your Home Purchase Smarter

Get instant repayment estimates and see how much you could borrow.

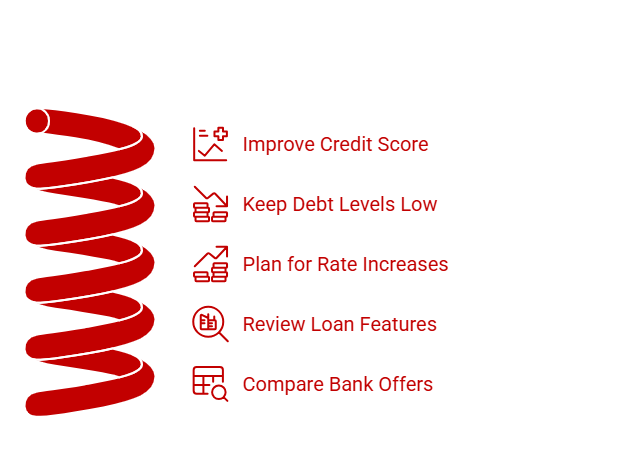

Tips To Prepare for SBR-Linked Home Loans in 2026

Here are a few simple steps that can help you prepare before taking a floating-rate home loan this year:

- Improve your credit score: A stronger score can help you qualify for a lower spread and better overall rates.

- Keep your debt levels low: Banks prefer borrowers with manageable commitments and steady repayment capacity.

- Plan for possible rate increases: Check whether you can still afford the instalment if rates rise by 0.25 to 0.50 per cent.

- Review loan features carefully: Flexi options, extra payment facilities and any lock-in periods can affect long-term cost.

- Compare offers from several banks: Since the SBR is standard, focus on the final effective lending rate and total repayment.

A bit of preparation can make a big difference when choosing a floating-rate loan. By keeping your finances healthy and carefully comparing offers, you can select a package that remains manageable even if rates change in the future.

Ready To Apply for a Home Loan in 2026?

Understanding how the Standardised Base Rate works can help you make clearer decisions when planning your home loan. If you are getting ready to buy a property, it’s a good idea to review your credit score early and check how much you can comfortably afford, even if rates change. This will help you avoid last-minute surprises and choose a loan that suits your long-term plans.

For more property tips, guides and market updates, visit the PropertyGuru Guides section.

Still searching for the right home? Explore the latest launches and resale properties on PropertyGuru Malaysia.

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.

Disclaimer: The information is provided for general information only. PropertyGuru International (Malaysia) Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.