As the nation endures its third week under the extended Movement Control Order (MCO), the impact of the MCO amid the ongoing Covid-19 outbreak on the Malaysian economy has yet to be fully realised.

In line with its commitment to being the nation’s property advisor, PropertyGuru Malaysia anticipates corresponding effects on home seeker sentiment to be short-lived, with prospects for recovery in the near term.

Sheldon Fernandez, Country Manager, PropertyGuru Malaysia notes that income and employment have been adversely affected by the closure of non-essential businesses during the MCO, and many Malaysians are prioritising bread-and-butter issues.

“This dampened sentiment is likely to persist through to H2 2020, though measures such as the government’s Economic Stimulus Package (ESP) announcements and Bank Negara Malaysia’s (BNM’S) six-month moratorium on financing payments are laying the foundation for the market to bounce back.”

Sentiment among home seekers was already in decline at the start of the year, with the PropertyGuru Malaysia Consumer Sentiment Study H1 2020 reporting a drop in the Property Sentiment Index to 42 points, down from 44 points in the corresponding period last year.

Meanwhile, research by property data analytics and solutions provider MyProperty Data Sdn Bhd highlights the property market’s resilience in the face of prior economic downturns and viral outbreaks, notably the severe acute respiratory syndrome (SARS) epidemic of 2002.

The Resilience Of Property

In recent events, property transaction volumes and values have remained strong throughout periods of uncertainty (see Chart A).

Chart A: Property Transaction Volume vs Value Growth (Source: MyProperty Data, NAPIC data)

According to the National Property Information Centre (NAPIC), the national house price index has not exhibited an overall decline since 1999, though its growth moderated to a low of 1.1% in 2001.

Fernandez explained that during the 1998 recession, in conjunction with the outbreak of the Nipah virus, volumes and values declined by 32.3% and 47.6% respectively, showing the largest downturn in recent decades.

“However, the industry still moved forward, with 186,000 transactions worth RM27.9 bil. In addition, house prices as a whole have only continued to grow over the past few decades, highlighting the merits of property as an asset class.”

Similar recoveries are seen in national house price growth in the years following 2001, 2006 and 2009. “Price growth, as well as transaction volumes and values, have slowed down in recent years, with measures in place to address the residential overhang. This may cushion potential impacts on the market as it rolls with the blow,” says Fernandez.

“Moving forward, investors tend to restructure their portfolios in uncertain times to manage risk, with property as a potentially lucrative venture. This, along with natural corrective forces as the market regains equilibrium, may account for the sharp recoveries seen in domestic property following crisis years.”

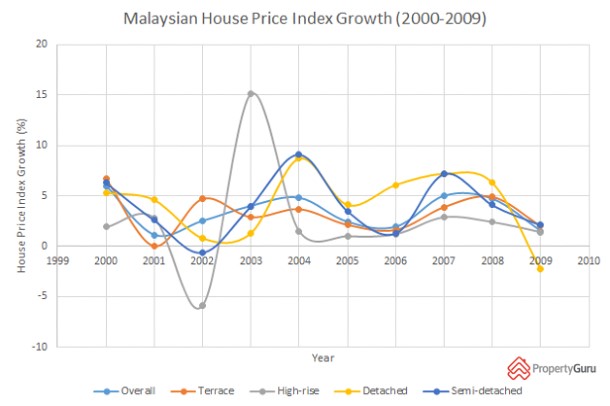

In terms of property types, high rises exhibited the most volatility in prices from 1999-2009, from a high of 15.1% growth in 2003 to a low of –5.9% the previous year (see Chart B).

Chart B: Malaysian House Price Index Growth (2000-2009) (Source: PropertyGuru Analytics, NAPIC data)

As such, terrace homes will likely be a key focus for property seekers moving forward. This is supported by the PropertyGuru Malaysia Consumer Sentiment Study H1 2020 report, which found that terrace homes are the residence of choice (39%) among Malaysians.

This is in line with MyProperty Data’s research which shows that terrace homes emerged as the clear favourite in Greater Klang Valley from 1999 to 2004, in terms of transaction volumes.

Joe Hock Thor, CEO, MyProperty Data, explained that median prices went from about RM220,000 in 1999 to up to RM400,000 by 2004. Around which time, demand similarly progressed to Setia Alam, Klang and other outlying areas towards 2012.

“Developers such as Sime Darby, SP Setia, Gamuda Land and IOI caught the wave perfectly, building larger homes within master planned townships at prices found closer to the city. High-rise popularity in Kuala Lumpur over this period picked up post-2003; this may have been due to cashed-up investors taking the opportunity to pick up glossy headline properties at discount prices.”

This resulted in substantial price appreciation, with median high-rise prices rising from RM350,000 in 4Q 2003 to RM765,000 in 4Q 2009.

Moving forward MCO and Covid-19

BNM’s reduction of the Statutory Reserve Requirement Ratio to 3.00%, moratorium on financing payments, OPR revision as well as revised voluntary EPF contribution guidelines in the government’s earlier ESP announcement are some initiatives contributing towards significant domestic liquidity moving forward.

“For those struggling to make ends meet, these measures help address costs of living while presenting an opportunity to rebuild savings. For those with leverage, it may be a good time to invest,” says Fernandez.

“There have already been calls from some quarters for revised loan-to-value ratio caps for third home purchases. This would accommodate demand from property seekers with leverage, driven by developer initiatives to add value for purchasers amid the changing property landscape.”

GuruCares Reaches Out To Property Agents

PropertyGuru acknowledges the potential impact of the MCO and other recent events on industry stakeholders, particularly property agents, who are often overlooked amid the larger national housing agenda.

Therefore, PropertyGuru has announced the launch of a suite of GuruCares initiatives, aimed at easing the burden on agent partners. Read more about GuruCares initiatives here!

Check out these latest project reviews today! Or explore these useful tips on how to stay sane during these trying times!